Great contribution to the Odd Lots newsletter from @IrvingSwisher and @_vikasbp that we published last week.

Regardless of where Kevin Warsh stands, the FOMC has already taken a more hawkish turn.

Read the entire thing thing here: https://t.co/67mkZMGoLE

Today's jobs report shaves off the case the labor market is reaccelerating. Lowers the prospect of a July hike, but also signals tougher Fed tradeoffs.

Inflation well above target, labor mkt momentum looks less impressive now

Payroll softness compounded by big negative revisions.

Household survey was weak beyond the "falling unemployment rate." Prime age 25-54 employment rate fell 0.6%, a weirdly large drop. Driven by 25-34yr olds' employment and participation cratering.

Strip out imputed px, like portfolio mgmt, & also remove the impact of strong software px, & you still end up with the mkt-based core PCE less info processing equip at 3.34%, nearly identical to core at 3.4%. 3m SAAR of mkt-based core serv was 4% in May vs 2.7% last May.

Forecasters who can transpose the PPI and CPI into the May PCE are expecting a firm core print (and wide wedge with the CPI) on Thursday morning, yielding a 3.4% increase from a year earlier.

For context, four FOMC participants expect core PCE to end the year at 3.2% or lower. Another four expect it to end the year at 3.5% of higher. The remaining 10 have it at 3.3%-3.4% on a Q4-Q4 basis.

Micron, the largest US maker of computer memory chips, delivered a sales forecast that topped Wall Street estimates after AI-fueled shortages of the components sent prices soaring. https://t.co/fv4gPPxPzm

Great summary

The statement and the press conference were distractions. The Projections were the main show.

The Fed has a tightening bias in all but name. Ironic if "no forward guidance" actually pulls forward the timing of the first potential hike...

Very hawkish dot plot.

Nine out of 18 officials have at least one hike this year (and six of those 9 have *multiple hikes*).

Only one person has a cut this year, and one participant (presumably Warsh) didn't submit an SEP

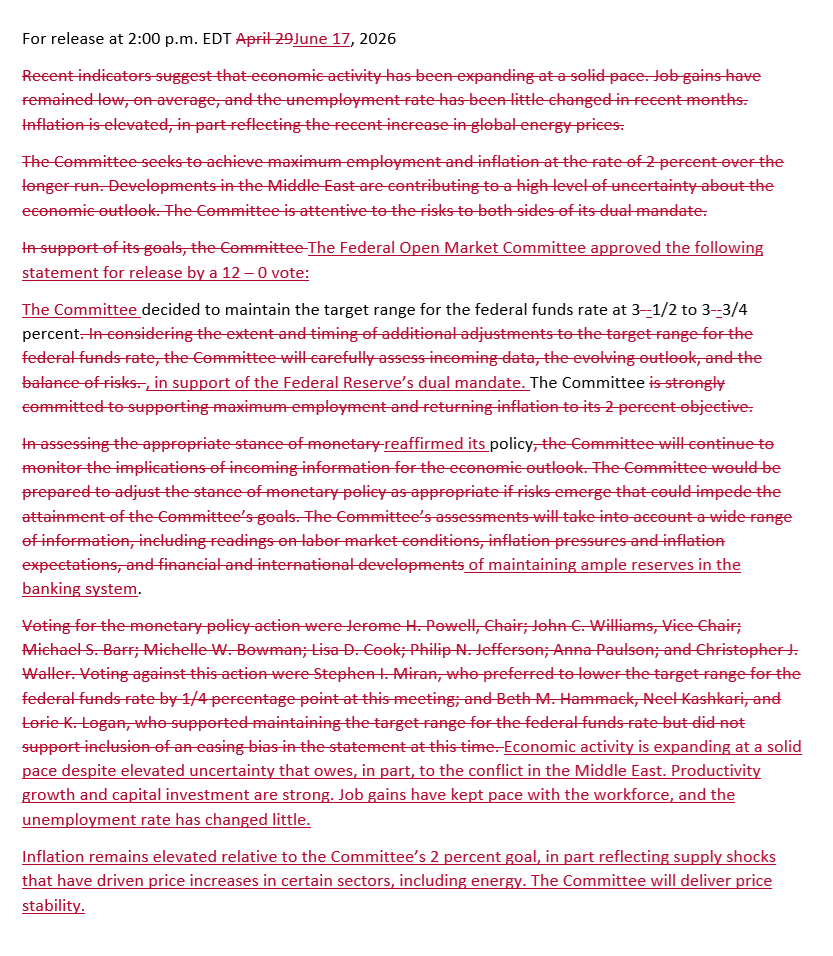

The statement gets a complete writethru from top to bottom, much shorter

With the May PPI and CPI in hand, forecasters expect core PCE to print around 0.35% in May.

This would raise the y/y rate to 3.4%. The six-month annualized rate would climb to 4.1%, the highest since June 2023.

Both measures were below 3% in the year-earlier period.

Early estimates of the May PCE number (following the Thurs release of May PPI and the CPI on Wed) point to a firm core m/m reading that rounds up to 0.4%. Market-based core was milder.

Portfolio management and airfares (which come from the PPI) have widened the CPI-PCE wedge in May. I will post the cheat-sheet table later.

A 2nd FOMC voter—Dallas's Lorie Logan—indicates rate hikes "this year" may be warranted

"I am increasingly concerned that higher interest rates could be necessary later this year to fully restore price stability...."

Cleveland Fed President Beth Hammack says if recent trends continue, rate hikes may "soon" be appropriate

“If we wait for definitive evidence that high inflation has become embedded in the economy, it may require larger policy adjustments, at greater cost.”

https://t.co/tzAqcHTtFT

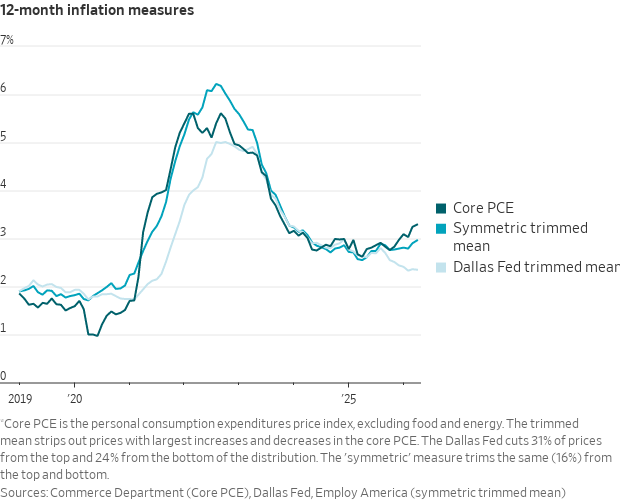

The Dallas Fed trims more from the top of the price distribution than the bottom. That asymmetry made it late to identify the 2021 surge.

Other versions that trim symmetrically, like one from @employamerica, are running closer to 3%.

The question, as @RiccardoTrezzi put it: is "looking through" inflation a principled framework or a way to down-weight inconvenient prints?

https://t.co/MqgnKqvAFd

Fed Chairman Kevin Warsh wants to pay more attention to measures of inflation that strip out the most extreme price moves each month.

Several versions exist, all running below core. The most widely cited is the Dallas Fed's, at 2.3% in April (vs. 3.3% for core PCE).