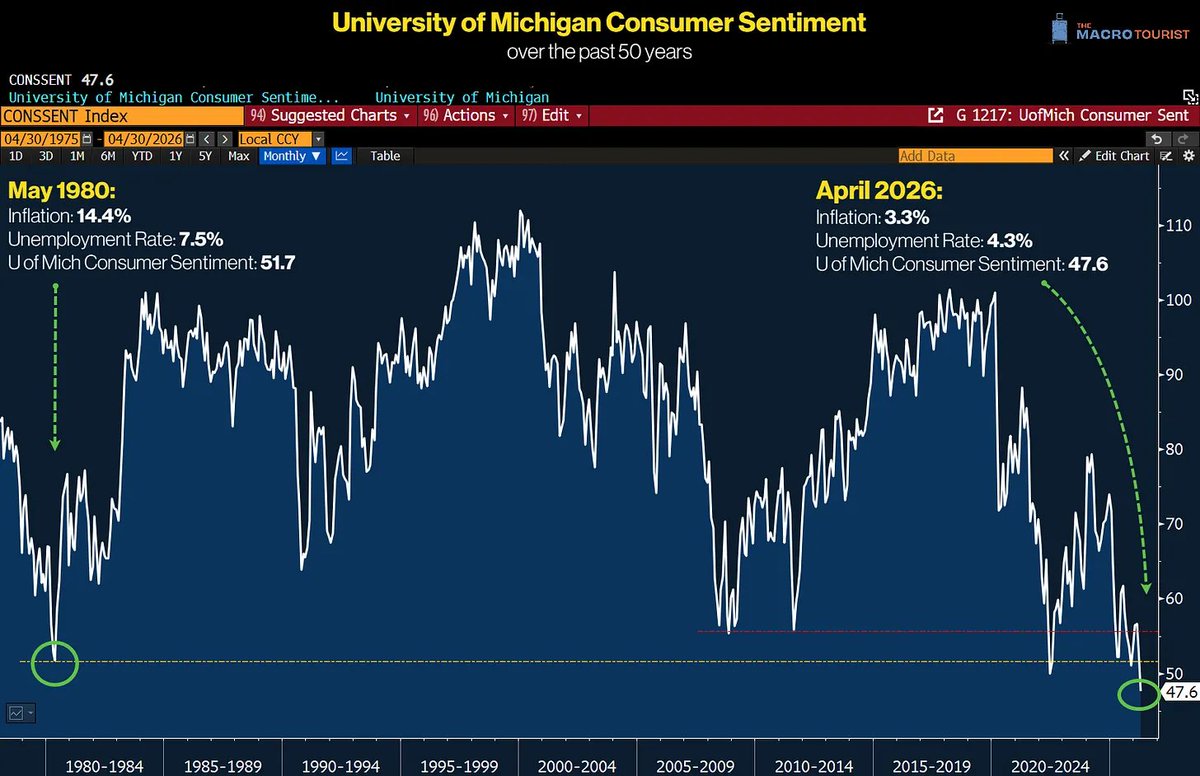

"U of Mich Consumer Sentiment hit an ALL-TIME LOW! It’s kind of shocking that today, with Inflation at 3.3% and Unemployment at 4.3% consumers feel worse off than in 1980 when Inflation was 14.4% and Unemployment 7.5%."

ht @kevinmuir

Stellar 1 yr performance across the memory & storage semiconductor industry

AI infrastructure buildout created insatiable demand for NAND flash & DRAM

One important caveat : this industry is deeply cyclical

Prices can collapse 60-70% in a downcycle as manufacturers overbuild capacity, this has happened across many past cycles (pic attached⏬)

The current upcycle is real, but it will not last forever.

So when does it top?

That's the trillion dollar question. The cycle likely stays strong through 2026 & 2027 as AI capex from hyperscalers (Microsoft, Google, Amazon, Meta) remains elevated & new fab capacity takes 2-3 years to come online.

The risk signals to watch: if AI spending growth decelerates, if Chinese manufacturers flood the market with cheap NAND, or if a technology like Google's TurboQuant which reportedly cuts AI memory requirements significantly

Most analysts expect the cycle to remain in the industry's favour through at least mid to late 2026, with 2027 being the year to watch for signs of a turn.

What do you think?

P.s. Not undermining the reforms and policies made/done/brought by the government and Indian companies but I'm trying to focus on stupid mistakes they have done which will cost us more & are creating a drag for all the work we are doing in positive directions.

As said by investors & RBI executives we are in a "goldilocks phase". I believe if this phase persists without growth rate of 7-8%+ what @Nithin0dha is saying will be seen as self fulfilling prophecy & the low hanging fruit will fix today but not tomorrow's growth.

Asked someone from the industry whether foreign investors are still interested in allocating to India. The TLDR:

Interest has pretty much died out. India is seen as geopolitically exposed, especially to an oil shock. There are no real AI plays. Valuations are rich. And the rupee situation doesn't help.

On top of that, investors who were sitting on gains have taken money off the table and are now looking at markets like Japan, Taiwan, Korea, Europe etc instead.

He also pointed out that our LTCG/STCG structure and the increase in STT have made India less attractive compared to other markets that are seeing inflows.

If we need to attract FPIs back, and we do, fixing this feels like pretty low-hanging fruit.

For Kaveri engine Govt spent is 1B$ in 20 yrs now we r importing 25B+$ worth engines bcuz it didn't do what we intended it to do. We want 70K inr earning engineer to give a product worth Billion $ & Im not ranting just a stupid investor like U, who is still ready to invests in 🇮🇳

$NVDA down 20% from highs. $MU down 20% after blowout earnings. Both stories are intact -- but oversized holders aren't sleeping.

Jim Roppel learned this with 3X leverage on 3 stocks: "Price will hurt you, but size will kill you." His max today is 18% in one name.

The stock can be right and the position can still destroy you.

Every correction is different, but investor behavior doesn’t change.

Bad investors panic and sell.

Good investors get nervous but hold.

The Best investors get excited about potential opportunities.

Capital is important. But capacity to wait is extremely important. Market provides you wealth when it wants and not when you need. Capacity to wait differentiates between whether you create wealth or forced to leave the journey.

Safe money, not invested in markets would only provide you capacity to wait. So safe money is as important or more important than invested capital.

The most humbling chart in investing.

The world's top 10 companies — by decade:

1980: IBM, AT&T, Exxon, Shell. Energy dominates.

1990: 6 of 10 are Japanese banks. Japan = 40%+ of MSCI World.

2000: Microsoft, GE, Cisco, Walmart. TMT bubble.

2010: Exxon, Apple, PetroChina, BHP. China + Energy.

2022: Apple, Microsoft, Nvidia, Tesla. Only Tech delivers growth.

Japan went from 40%+ of the global index in 1990

to 6% today.

Every decade has a new narrative.

Every decade has a new set of "obvious" winners.

And only 1 of 10 market leaders survives into the next cycle.

Diversify.

Stay humble.

The obvious trade is usually the dangerous one.

UBS: Current macro environment favors commodities

- Commodities hedge inflation risk

- Gold hedges geopolitical uncertainty and rising government debt

We live in volatile times, so expect elevated volatility. The recent gold/commodity selloff doesn’t negate the long-term thesis... it’s just part of the game.

- Central banks, the major gold driver, are still buying

- Supply shortages are bullish for commodities

- Copper deficit is widening

- So are uranium and silver

While predicting short-term price movements is hard, over the long term commodities have to rise.

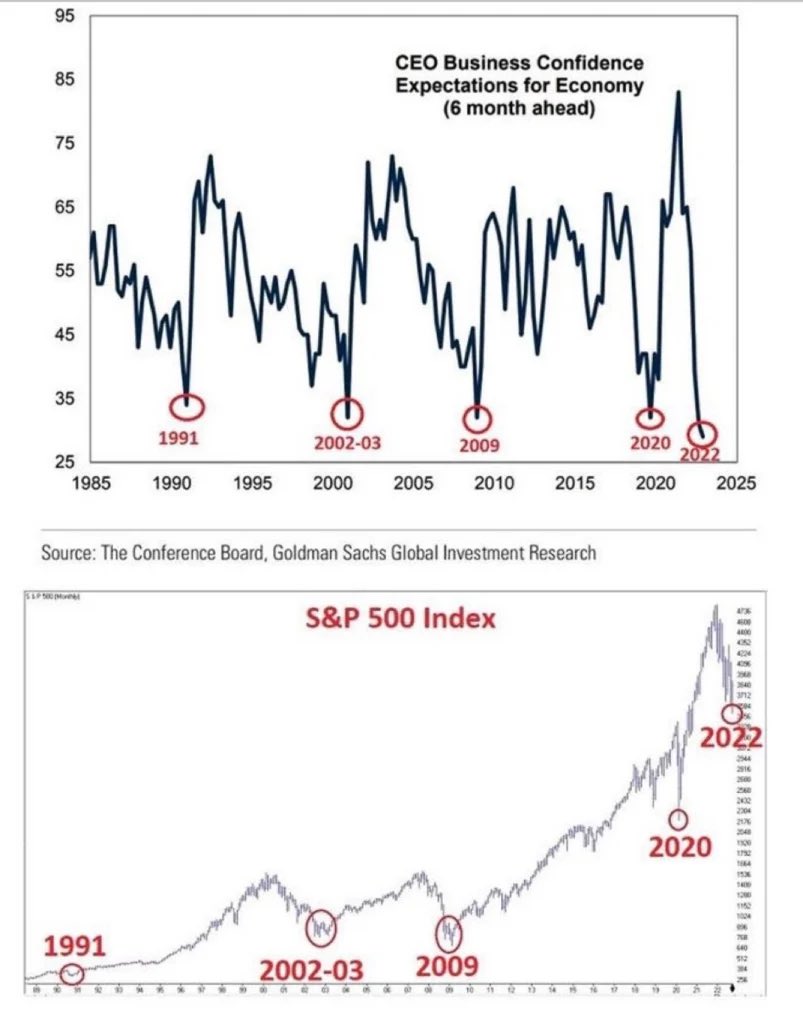

The best buy signal in markets isn't a chart pattern.

It's CEO confidence hitting rock bottom.

1991: CEOs most pessimistic → S&P 500 bottomed → massive rally

2002-03: CEOs most pessimistic → S&P 500 bottomed → massive rally

2009: CEOs most pessimistic → S&P 500 bottomed → massive rally

2020: CEOs most pessimistic → S&P 500 bottomed → massive rally

2022: CEOs most pessimistic → S&P 500 bottomed → massive rally

Every. Single. Time.

When the people running the world's biggest companies are most scared about the economy — the market is loading up for the next bull run.

Extreme pessimism is the contrarian investor's best friend.

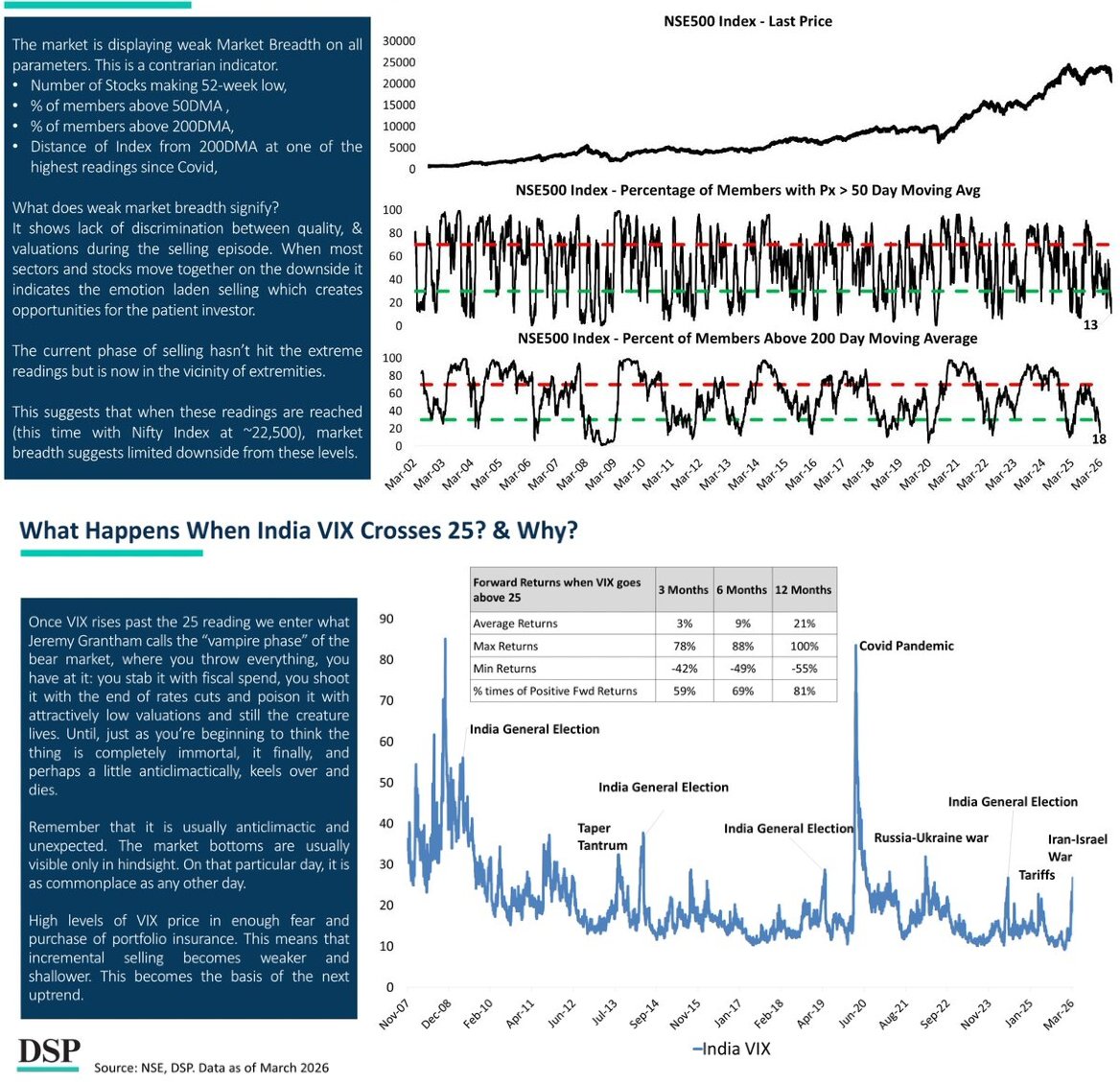

Very Interesting Data from DSP⏬

Nifty (USD terms) has given up nearly 4.5 years of gains & is back to Sep’21 levels

4 consecutive months of decline on Nifty is rare - only 7 such instances since the 1990s

India VIX crossing 25 & touching ~29 typically reflects panic - these zones historically are the best times

Market breadth is extremely weak:

- Many stocks at 52-week lows

- Stocks above 200 DMA within Nifty 500 are near extreme lows

Some index heavyweights are approaching towards very attractive valuation zones (Private banks, IT)

Historically when India VIX crosses 25:

Probability of positive 12 month returns ~81%

Weak market breadth + elevated VIX + valuation normalisation together form a classic contrarian setup

This does not indicate exact market bottom timing

but it significantly improves risk-reward for staggered investing

@SahilKapoor