$AMZN Q1 2026 earnings:

• Revenue $181.5B vs Est. $177.2B

• EPS $2.78 vs Est. $1.64

• AWS Sales $37.6B vs Est. $36.7B

Q2 Guidance

• Revenue $196B vs Est. $189B

FY26 Guidance

• CapEx $200B vs Est. $200B

Thoughts on SaaS

-No, SaaS is not dead.

-“Vibe coding” replacing enterprise SaaS is not a serious argument. Building a competing SaaS product still requires making something meaningfully better, and in that delta, human ingenuity remains the bottleneck.

-AI tools are not the sole province of new entrants. The same advantage applies to incumbents.

-It is now easier to build a SaaS tool, but harder to build a SaaS company.

-The real threat is agents, but SaaS will adapt.

-The market is overlooking SaaS companies’ ability to make advances in the agentic layer.

-SaaS companies are not dinosaurs and, by and large, will respond well to the existential agentic threat.

-One of the reasons this shift is different for incumbents (SaaS) is that the adaptation response (implementing agents) doesn't have to cannibalize their economics and could even improve them.

-Most SaaS companies will retain important touchpoints with customers even in an agentic world.

-GUIs will still be a destination. This is a form factor optimized for our visual cortex. Even if part of the interaction layer is absorbed by agents, there will still be a need to go into applications. Just as fears that Alexa voice would replace online search proved wrong, there is a visual, low-friction nature to GUIs that give them staying power.

-From an investing standpoint, more value exists in smaller-cap SaaS names, but selectivity is important.

-While the future is uncertain, it is clear that some of the selling pressure is being fueled by narratives designed to provoke fear.

$KKR - Bloomberg reports a $1.5B investment in Vertical Bridge (towers).

Note: source not verified by Reuters.

Risk management is fundamental with this early options flow.

Due diligence is mandatory.

Ready for Action in the United States

Today, Action, core holding of 3i Group $III.L, shared its plans for the upcoming years. On the horizon lies an expansion into the United States of America. Hajir Hajji, CEO Action:

“As part of our regular new markets research, we have conducted an in-depth market study of the United States and see a lot of promise for a formula like ours in non-food retail. Based on this favourable conclusion, we have decided to commence preparations for opening a first Action store in the United States at the end of 2027 or early 2028, provided the market context will not change.

As we are launching from scratch on a new continent, we will take the time needed to build up successful operations: one store at a time, patiently learning what works and adjusting when necessary.”

Moreover, the board increased Action’s white space potential in the European market by c.200 stores compared to last year. The total white space in Europe now stands at c.4,650 stores, in addition to the 384 newly opened stores in 2025. At the end of 2025, Action had an existing base of 3,302 stores in 14 European countries.

Insider buys usually feel like PR fluff. But $45M into $KKR at these levels is clearly an investment, not signaling. Especially meaningful coming from guys whose entire schtick is figuring out what things are worth...

Constellation Software has no moat.

Its founder said so himself.

Mark Leonard, 2014 shareholder letter:

"The barrier to starting a 'conglomerate of vertical market software businesses' is pretty much a cheque book and a telephone."

He's right. There is nothing stopping anyone from buying a small software company that manages cemeteries or water utility billing. By 2016, Vista and Thoma Bravo had each raised multi-billion dollar funds in a single year. Leonard noted this $CSU was deploying $1.4B. Today, Vista alone manages $100B. The gap only widened. And CSU kept winning.

So what does a $40B company have that $100B in PE capital doesn't?

Same letter. Next paragraph.

"CSI does have a compelling asset that is difficult to both replicate and maintain: We have 199 separately tracked business units and an open, collegial, and analytical culture."

That was 2014. 199 business units. Today it's 1,000+.

Every business CSU acquires doesn't just add revenue. It adds a data point to the largest private dataset in the world on how to operate vertical market software. Pricing experiments. Churn playbooks. Upsell sequencing. Tested across 100+ countries, 50+ verticals, simultaneously.

Leonard built this deliberately. In his 2016 letter, he studied a group he called High Performance Conglomerates: Danaher, Berkshire, Illinois Tool Works, Roper, TransDigm. He tracked their EBITA returns over decades. Found a pattern: returns started at ~21%, peaked at ~46%, then decayed as the conglomerates grew too large, paid higher multiples, and centralized.

Only one other tried CSU's model, buying hundreds of small businesses and managing them autonomously. Leonard's verdict: "They eventually caved in to increased centralization."

He studied why. His answer:

"When a VMS business is small, its manager usually has five or six functional managers to work with. All the employees know each other, and if a team member isn't trusted and pulling his weight, he tends to get weeded-out. Priorities are clear, systems haven't had time to metastasize, rules are few, trust and communication are high."

"The quirky but talented rarely survive in this environment."

That last line explains the entire architecture. CSU doesn't keep businesses small because it can't integrate. It keeps them small because Leonard studied what integration does to talent, innovation, and returns and concluded the data is unambiguous.

Small wins. Then he proved it with his own company.

Head office expense: 1.9% of net revenue in 2005. By 2014, it was 0.9%. By 2016, 0.5%. Over that same period, return on invested capital went from 17% to 37%.

"Clearly trust trumped central bureaucracy in our case."

PE firms don't build this. They can't. Their model is buy, optimize, exit in 3-7 years.

Leonard said the difference plainly in 2021: "Most of our competitors maximize financial leverage and flip their acquisitions within 3-7 years. CSI appreciates the nuances of the VMS sector. We are permanent and supportive stakeholders in the businesses that we control."

You can't build institutional knowledge across 1,000 businesses when you sell every 5 years. You never accumulate the dataset. You never build the trust. You never learn which operating experiments work across verticals and which don't.

Vista has more capital. They don't have 30 years of compounded operational intelligence across 1,000+ autonomous businesses with base rates for every key metric that make acquisition discussions "rational, not emotional."

The barrier to entry is a cheque book and a telephone.

The barrier to replication is three decades.

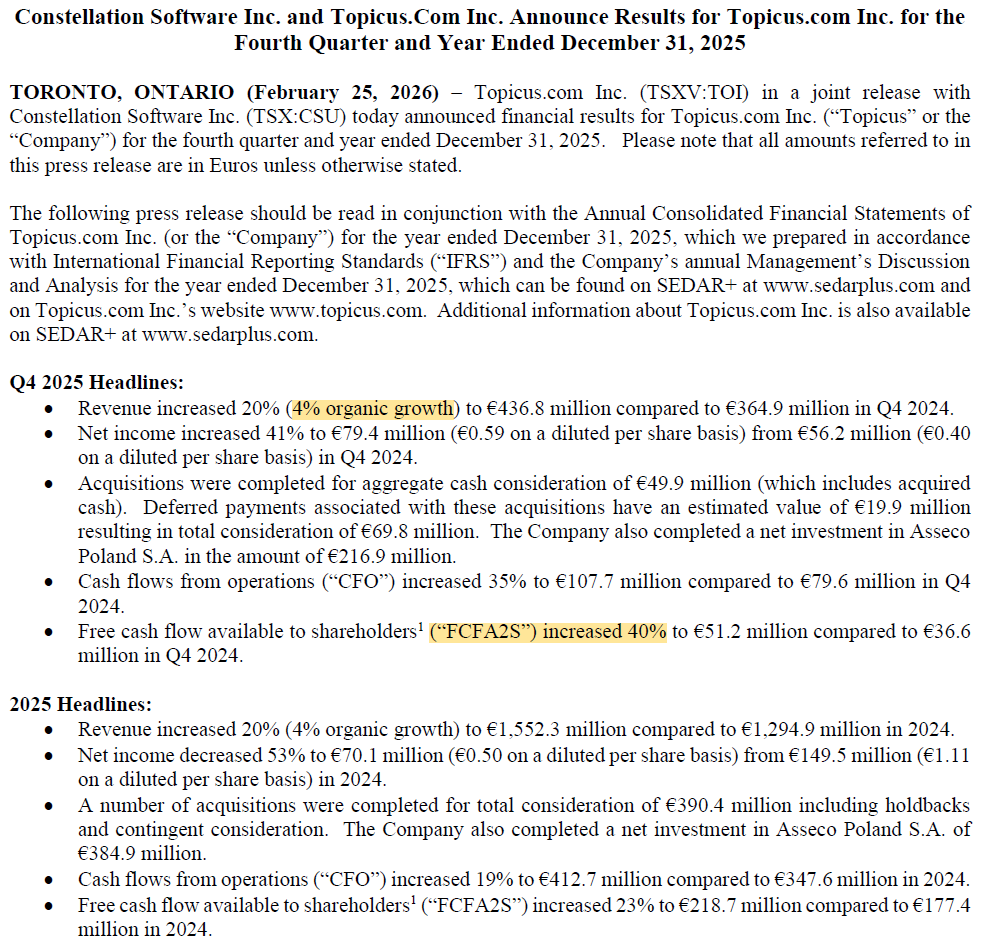

$TOI.V Q4 2025 results are out and they look pretty good:

✅ Organic growth 6% (4% in CC)

✅ FCFA2S +40%

✅ Margins up

✅ €70 million in acquisitions (+ €20M for acquisitions pending completion) => Solid quarter for acquisitions!

cc $CSU.TO

I keep getting asked about $CSU.

50 things every Constellation Software investor should know to get up to speed.

The basics. The numbers. The structure. The model. The compensation. Mark Leonard. Mark Miller. The moat. The hidden assets. The risks.

All of it. Bookmark this.

THE BASICS

1. Founded in 1995 by Mark Leonard in Toronto. He spent 11 years as a venture capitalist before starting CSU.

2. Listed on the TSX. Ticker: https://t.co/6YiDsxMYKc. One of the 60 largest companies in Canada.

3. CSU acquires, manages, and permanently holds vertical market software businesses. Software built for one specific industry. Courts. Cemeteries. Utilities. Transit.

4. Why VMS? Individual market niches are tiny. Often under $5M. Venture capital and big tech ignore them. But the software is mission critical, has high switching costs, and generates recurring revenue. Nobody else wants it. Incredible economics once you own it. That's the arbitrage.

5. 125,000+ customers. 100+ countries. 1,000+ acquired businesses. 64,000+ employees.

THE NUMBERS

6. Revenue: ~$11B USD (TTM). Up from $3.5B in 2019. More than tripled in five years. No down years. Ever.

7. ~75% of revenue is recurring. Subscriptions and maintenance contracts. The foundation of everything.

8. Customer retention: 96-98% annually. Without long-term contracts.

9. IPO in 2006 at ~$18 CAD/share. Now ~$2,377 at today's beaten-down price. A 130x return. $10K at IPO = $1.3M today. At the 52-week high of $5,300 it was nearly 300x.

10. Free cash flow to shareholders (FCFA2S): $1.47B in 2024, growing 27% year over year. This is Leonard's custom metric. Brutally honest. Deducts the IRGA liability on purpose, making numbers look worse than reality.

THE STRUCTURE

11. Six operating groups, each large enough to be its own public company.

12. Volaris. Largest group. 240+ businesses across 40+ verticals. Transportation, financial services, communications. Miller's home base before becoming President.

13. Harris. Oldest group. Public sector roots. Utilities, healthcare, government, schools. 100+ businesses.

14. Jonas. Started in club management software. Now fitness, hospitality, construction, foodservice. 140+ businesses.

15. Perseus. Healthcare, government, homebuilding. Smaller, closer to HQ.

16. Vela. Industrial. Oil and gas, manufacturing. 8 divisions.

17. TSS / Topicus. European operations. Spun out in 2021. Lumine Group spun out from Volaris. Both separate public companies where CSU retains significant interest.

18. Each business operates autonomously. HQ provides capital allocation and benchmarking, not operating directives. The culture is often described as "delegation to the point of abdication."

19. CSU is structured like Berkshire Hathaway but owns vertical market software instead of railroads and insurance. Decentralized. Permanent ownership. Zero stock-based compensation. Founder-led for 30 years.

THE MODEL

20. Buy and hold forever. Unlike private equity, CSU never sells an acquisition. This attracts better sellers. Founders who care about their employees and customers choose CSU over PE because the business stays intact.

21. The capital allocation cycle: buy sticky businesses, collect recurring cash flow, deploy into more acquisitions, compound. Repeat for 30 years.

22. CSU has identified tens of thousands of VMS businesses globally. They've acquired roughly 1,000 so far. The runway is measured in decades.

23. Typical deal: under $5M. Largest ever: Allscripts hospital business for ~$700M. Volume of small deals is the strategy.

24. $1.8B deployed into acquisitions in 2024 alone.

THE COMPENSATION

25. Zero stock-based compensation. $0. Ever. In 30 years. Executives buy shares at market price with their own cash. Same price as you and me.

26. Executives must invest up to 75% of their after-tax bonus in CSU shares with a 4-year lockup. Skin in the game is not optional. It is policy.

27. Leonard waived all salary and bonus in 2014. "I'm your partner in CSI, not your employee." His compensation from that point forward was stock appreciation only.

28. Many CSU employees are now millionaires through their shareholdings. No options. No RSUs. Open market purchases with their own money.

MARK LEONARD

29. Published annual shareholder letters that developed a cult following. Disclosed ROIC, organic growth breakdown, capital allocation philosophy in detail. If you own this stock and haven't read them, start there.

30. In 2018, wrote his last annual letter. Drew an analogy between VMS and the newspaper industry lifecycle: growth, consolidation, eventual decline. "I anticipate that the VMS industry will evolve similarly."

31. Same letter: "I am already casting about for such opportunities" outside VMS. He was looking beyond VMS seven years before stepping down.

32. Broke his silence in 2021 with one letter. The only topic important enough to make him write again: lowering hurdle rates and redirecting ALL free cash flow into bigger acquisitions and new asset classes. "I have converted, and with the fervour of the newly converted, I am busy demonstrating my new-found faith."

33. Named Mark Miller in that 2018 letter with "10,000 hours of relevant experience." Seven years before he needed a successor.

34. Resigned as President in September 2025 for health reasons. Stock crashed 17% that week.

35. Almost no photos of him exist online. No earnings calls since 2018. Cancelled them to protect acquisition intelligence from competitors.

MARK MILLER

36. Joined CSU in 2001 through Trapeze, CSU's very first acquisition from 1995. A CSU lifer.

37. Led Volaris, the largest operating group. The board called him "the most experienced, knowledgeable, and capable person" to lead.

38. The majority of acquisitions in the last decade were made by people who are not Mark Leonard. The machine was built to outlast any one person. Whether it does is the open question.

THE MOAT

39. Switching cost layer 1. Cost irrelevance. Software costs less than 1% of a customer's revenue. Even if a competitor offered it free, the migration risk wouldn't justify switching.

40. Switching cost layer 2. Decision maker incentives. The buyer is often a government employee who faces career risk if a switch fails and zero upside if it succeeds. Rational choice: don't touch it.

41. Switching cost layer 3. Regulated data. Court records have chain of custody. Utility billing has compliance audit trails. Government permits have public records obligations. Legal barrier, not technical.

42. The majority of CSU's revenue comes from government and regulated customers. Government headcount has grown almost every decade for 70+ years. The IRS still runs COBOL from the 1960s. These customers don't switch.

HIDDEN ASSETS

43. The IRGA: CSU's interest in Topicus shows as a ~$1B liability on the balance sheet. It's arguably worth ~$3B+. One of the most misunderstood line items in CSU's financials.

44. Topicus and Lumine spinouts decentralize capital allocation further and create more acquisition capacity across the system.

45. VMS Ventures: $200M fund launched in 2021 to acquire distressed startups that can't turn profitable after raising venture dollars. Buying distressed SaaS at a discount.

THE RISKS (HONEST)

46. Leonard's health and reduced involvement. Miller is unproven at enterprise-scale capital allocation outside VMS. This is the biggest open question.

47. Competition for acquisitions increasing. PE and other serial acquirers bidding up VMS valuations. Leonard acknowledged this himself.

48. AI risk: not that someone builds better VMS. The real risk is the intelligence layer moving above it. If AI agents become the customer interface, whoever builds them captures the relationship.

49. ISS gives CSU a 9/10 governance risk score. Same structural penalties as Berkshire. Concentrated ownership, limited board independence. Understand what you own.

THE BOTTOM LINE

50. Three fear events priced in simultaneously: AI disruption + Leonard resignation + SaaSpocalypse. Down 55% from the 52-week high.

The moat isn't the software. It's the capital allocation machine and the people who run it. A thousand autonomous businesses compounding capital into a thousand more.

Every other serial acquirer copies the model. None of them copy the discipline.

I'm long $CSU. What did I miss?

Bonus: Mark Leonard once built a flamethrower.

$CSU has a secret $200M venture fund incubating AI companies inside its own empire.

VMS Ventures.

It only backs startups sponsored by Constellation's 1,000+ business units.

(1) raia - AI Agent Platform Deploying Across CSU

- Built inside CSU.

- Started in real estate (10x ROI, 80% cheaper):

- 48,000 finance conversations handled globally, 70% resolved without a human

- 50% of support tickets solved by AI at IDEAL (equipment dealer ERP)

- AI agents managing 60,000+ college athletes at Postgame

(2) AssetCore - AI-Native Utility Asset Management

- Natural language AI agent for managing infrastructure. - Maps to Harris Computer, CSU's utility billing group.

(3) Rentr - AI Renting Platform

- Founded by former Volaris CTO.

- AI handles tenant screening, referencing, and lease signing.

(4) Fero - Rental Equipment Delivery

- Former Wynne Systems VP who ran a United Rentals branch.

- Building delivery software for an industry where CSU already owns the dominant ERP.

Nearly every founder came from inside the Constellation machine.

The company the market thinks AI will kill is building AI companies within its own walls.

Read that again.

But yeah the bears are right.

This thing is going to zero.

I'm feeling like an absolute clown for not knowing that AI leaders at Raia AI ( $CSU owned ) have a podcast and have talked a lot about how Constellation is already using AI:

- Lee Dickson (Director at Raia AI): https://t.co/W7ImHyK9kS

- Rich Swier (Founder of Raia AI): https://t.co/qYl0SIBV72

They have interviewing $CSU employees regarding how they're using AI and talking about how Business Units are using AI!!!

Some quotes:

- "We're working with one CSI company right now and they're really forward thinking and they've basically created a mandate that by the end of the year each employee will have 3 agents working for them." Link:https://t.co/yXmkSt7hyg

- Rich Swier, Raia founder

- "Constellation proposed an AI contest... sent 3 reminder emails... I didn't want to be the one CFO that doesn't have a submission..."

- Shikha Gandhi, CFO at Carina Software

Link: https://t.co/yvAwFpPHKB

Jason Jackson, Group AI Enablement Lead at Vesta Software Group, discussed AI adoption hurdles specific to the CSI business model.

Link: https://t.co/HmkDddSwkT

They also literally talked about some challenges that every $CSU shareholder has been thinking of here: https://t.co/kRKoJMTtuB

This makes a me a lot more comfortable owning $CSU!! They're on it, y'all!