@lgbalcag@GreenPlusAnE The 1977 amendments indexed initial benefits to growth in average wages, and benefits after claiming to price growth. The change was partially a correction for 1972 amendments, which created the COLA and essentially double indexed benefits for inflation.

There’s two ways we could sever the link between taxes and benefits.

One involves a 12.4pp tax hike to continue paying generous benefits to rich retirees.

The other is lowering the maximum benefit those retirees can receive. A $100K limit is a reasonable places to start.

There’s a SS payroll cap because there’s also a benefit cap. Any debate about eliminating the payroll cap must admit the program isn’t an “earned benefit.”

If Congress wants more of our money for SS the least it can do is stop patronizing us.

If Social Security became a flat benefit at or even a bit above the poverty line, progressives would find themselves enjoying much more fiscal space for their other priorities. It would also happen to be a progressive reform that ends elderly poverty!

Exactly this. I’d be all for using some of the savings from cutting benefits of wealthy retirees to bring the last 6% of seniors out of poverty! Not so much for eliminating the payroll tax cap just to pay the wealthy retirees even more.

It’s worse than that. It’s fetishization of a program that was arguably built in 1977. Social Security as it was created in 1935/1939 was not programmed to grow on autopilot in the same way it is now.

@Izengabe_ Sure. Part of this is my befuddlement at people on the left's reactionary fetishization of a program created 90 years ago for a different workforce operating in a different economy, to the point that they feel the need to defend $100k checks to millionaire retirees.

For what it’s worth, other countries with flat benefits appear to have robust public support their system. Some, like the United Kingdom, are even having trouble keeping them from growing too quickly!

💯 I refuse to accept that the only way to maintain political support for giving $20k Social Security benefits to poor widows is by also spending trillions of dollars giving up to $100k benefits to rich couples.

If we're raising taxes by trillions, that's not where to spend it.

1) today’s US seniors have the lowest poverty rate & most wealth of any cohort in the history of the universe.

2) the full retirement age is 67, when benefits are 15% higher.

3) These are not really replacement rates, theyre effectively current retiree Social Security benefits as a share of current workers wages - which makes them seem low b/c wages keep rising.

4) They also don’t count for the fact that wages are taxed much more heavily than Social Security benefits.

@dylanmatt Sorry, the shortfall is actually 16% larger today than it was when that plan was released. But the Actuaries current estimates are likely overly rosy based on their fertility assumptions

@dylanmatt The problem with this bipartisan rescue plan (which is still very good) is that it was a designed to close a 75-year gap that was three quarters of the size that it is today. More drastic changes are needed than was projected just a couple of years.

I simply don't think we should waste a 12.4 percent point tax increase on the rich, the biggest hike since WWII, on benefits for the elderly

Raise the cap to cover 90% of income, raise the rate mildly, and save top income hikes for boosting benefits for kids

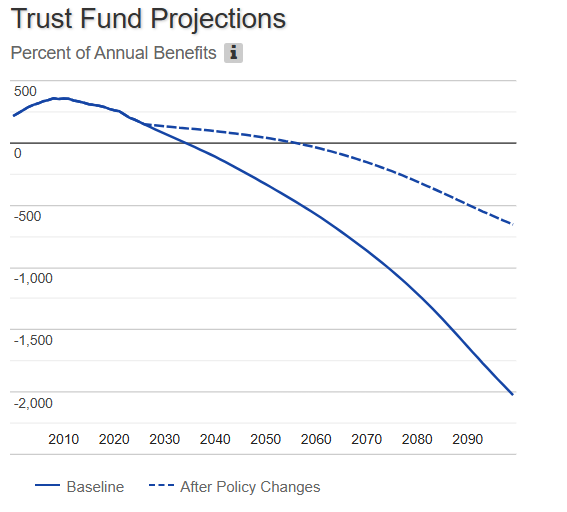

This is not true. Eliminating Social Security's tax cap - and not crediting additional benefits to newly taxed earnings - only keeps the program's trust funds solvent for 20 more years, and merely shrinks the growing gap between SS' costs and revenues

Today, Elon Musk, a trillionaire, pays the same amount into Social Security as someone making $184,500.

If we end that absurdity and lift the cap on taxable income, we can make Social Security solvent for 75 years and expand benefits by $2,400. My Social Security bill does that.

The first function seems more justified to me than the second. It's not obvious to me that we should be shifting consumption away from ages when people may want to buy a home or start a family and toward ages when they'll likely be wealthier and have fewer expenses.

Social Security does 2 things, not one:

1. It socially insures, by preventing old people from being impoverished.

2. It forces younger people who might undervalue their future need for money, to save.

Both are actually important governmental functions.

🗓️TODAY @ 2PM ET: Join us for a virtual event featuring a roundup of #SocialSecurity's and #Medicare’s finances + an expert discussion on the implications of insolvency and options for reform.

Featuring remarks by @SocialSecurity's Chief Actuary Karen Glenn + CRFB's Anna Bonelli, @MarcGoldwein, and Mark Sarney.

➡️Register here: https://t.co/trkge6tY5X.

An under-appreciated point. Social Security's financial problems are not just demographics.

Rather, by formula, benefits become *much* more generous each generation (yes, even after inflation). Today's retirees are coming out further ahead than previous ones - at great cost.

There's a third factor: Rising benefits, even after adjusting for inflation. In 1990, a 2-earner middle-income couple received about $44,000 in annual benefits. In 2026, a middle-income couple gets $60,000. By 2050, $86,000. /2

I looked up this story from Zach Carter's Keynes biography.

Did Milton Friedman really oppose black suffrage in South Africa? Not at all—he met and strategized with ANC leaders, was appalled by the apartheid system.

The source of this narrative: Quinn Slobodian

🗺️ What states are facing the largest average monthly benefit cut for retirees upon Social Security insolvency?

After applying the projected 24% benefit cut to current state data, we estimate an across-the-board monthly cut would range from $459 to $556 across the 50 states and the District of Columbia, with the benefit cut exceeding $500 per month in 29 states.

The top ten states facing the largest monthly reductions for retirees include:

1️⃣ Connecticut

2️⃣ New Jersey

3️⃣ New Hampshire

4️⃣ Delaware

5️⃣ Maryland

6️⃣ Washington

7️⃣ Minnesota

8️⃣ Massachusetts

9️⃣ Michigan

🔟 Utah

Find how your state compares to others here ⚖️ https://t.co/ia2rY2HgBL.