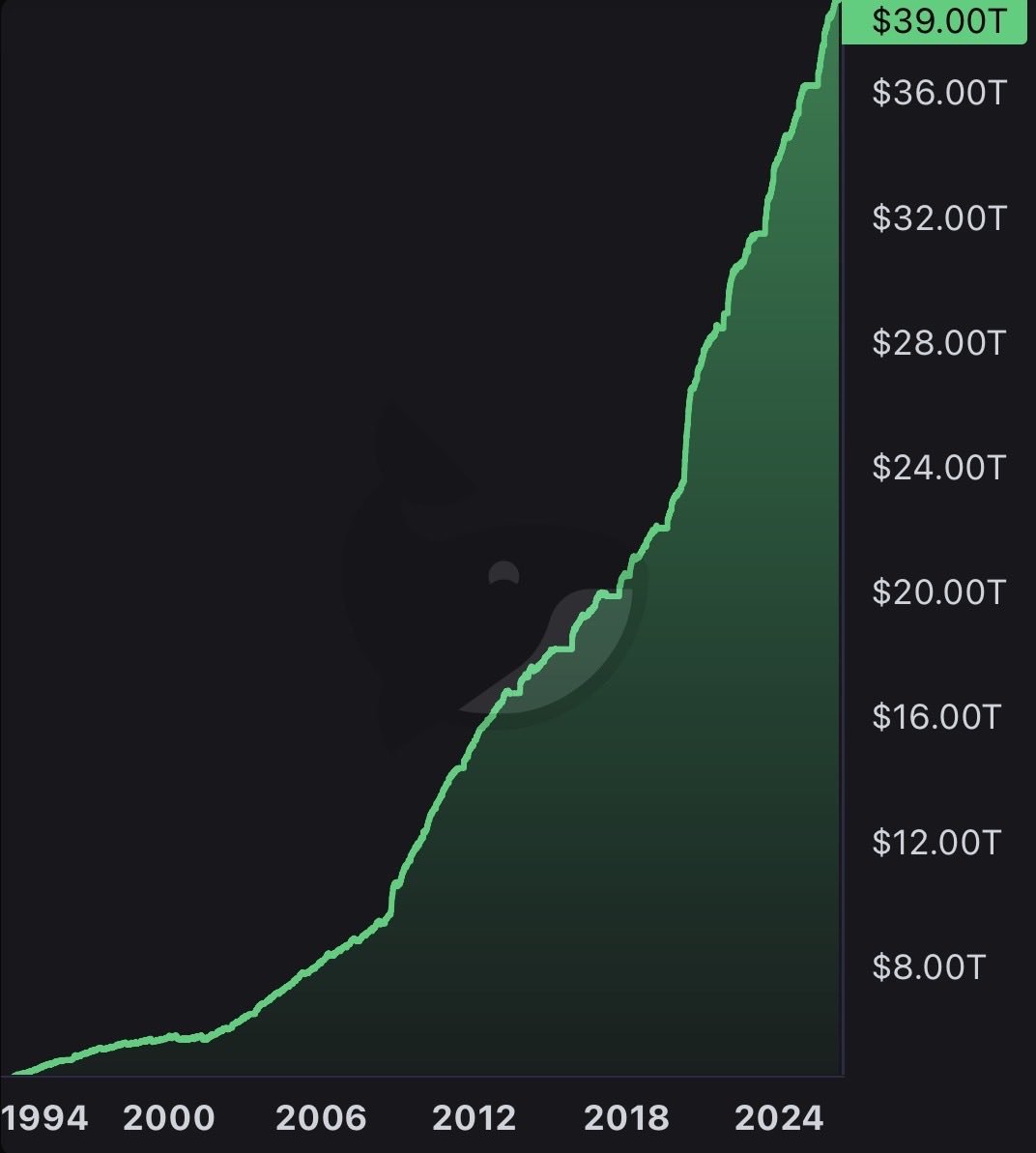

🇺🇸 Here's what $39 trillion in debt really means:

If we confiscated every dollar of U.S. corporate profit ($3.8T/year), it would take over 10 years to pay off.

Sell every ounce of gold ever mined: $32 trillion. Still $7 trillion short.

Liquidate every Bitcoin in existence on top of that: $33.5 trillion. Still $5.5 trillion short.

If we confiscated every dollar of federal tax revenue ($5.3T/year), it would take over 7 years to pay off, assuming zero spending.

The debt is 71% of every home in America, or 30% of every publicly traded company on Earth.

The debt grows by $7.2 billion a day, or $84,000 a second.

This is a problem.

You cannot buy a new gas turbine until 2030. Order books at GE, Siemens, and Mitsubishi stretch to 2029. Turbine prices have nearly tripled since 2019. Every AI data center needs power and every gas plant needs a turbine. And every turbine has one part that bottlenecks the entire industry: The blade. It has to survive in gas 500°C above the melting point of the metal it's made from and spin at up to 20,000 RPM under 10,000 g of centrifugal force. Each blade is grown as a single crystal of nickel superalloy, pulled through a vacuum furnace at 3 mm per minute. A set of blades costs $600,000 and takes 90 weeks to grow. The same metallurgy powers modern jet engines. Only 3 companies on Earth can build one. China spent $42 billion trying to catch up. They bought a Russian fighter engine, took it apart, and copied every part. Their copy ran 30 hours between overhauls versus 400 for the original. Modern Western engines run 4,000. You can reverse engineer the shape of a turbine blade. You cannot reverse engineer 60 years of metallurgy.

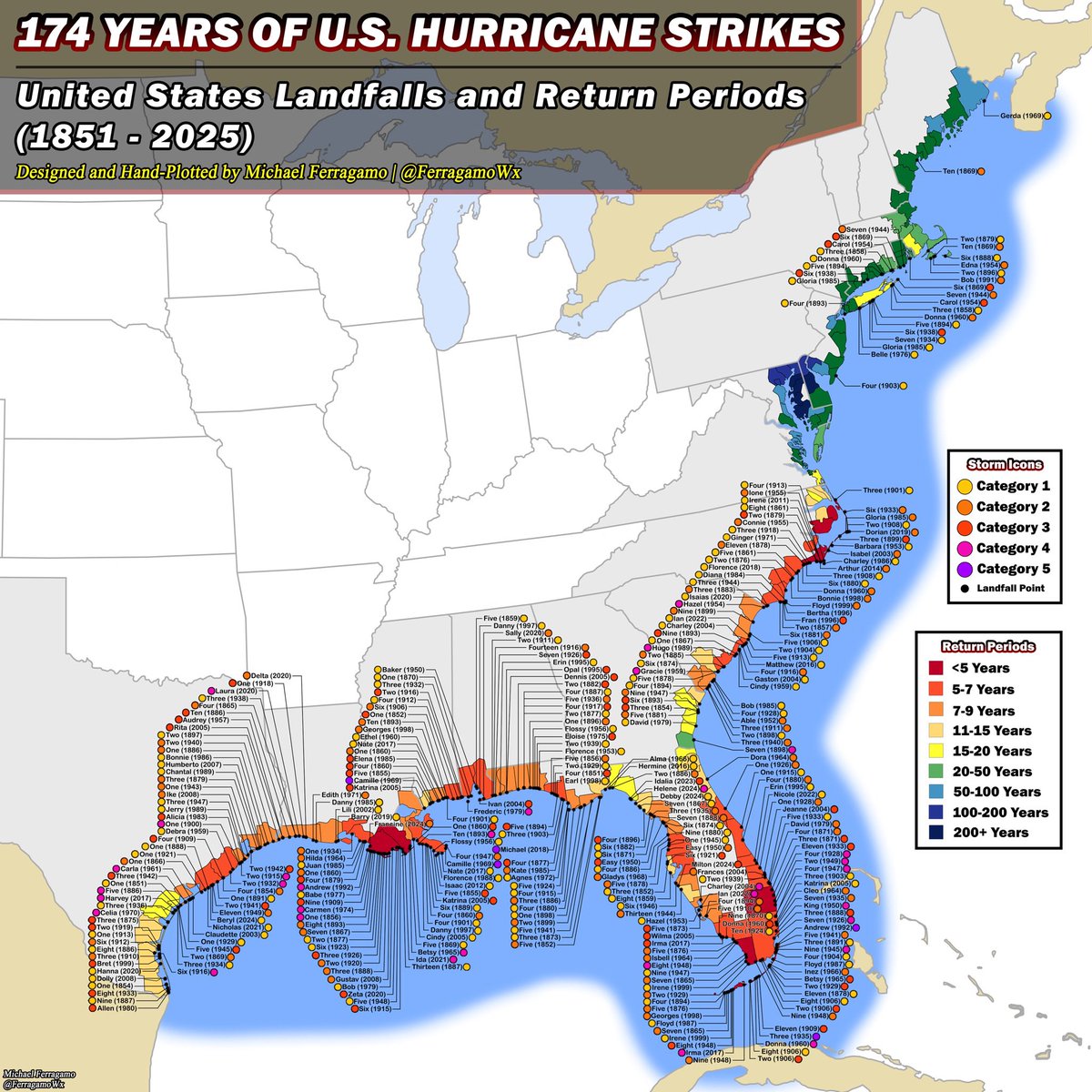

After months, I was finally able to combine both my hurricane landfall and return period datasets for the U.S. into one massive infographic.

I absolutely love this. What an insane map to look at!

OPEC+ eight members agree to raise production quotas by 206,000 bpd for May.

The market will likely go from discounting scarcity to expecting a balanced supply quite fast.

via Bloomberg, Reuters.

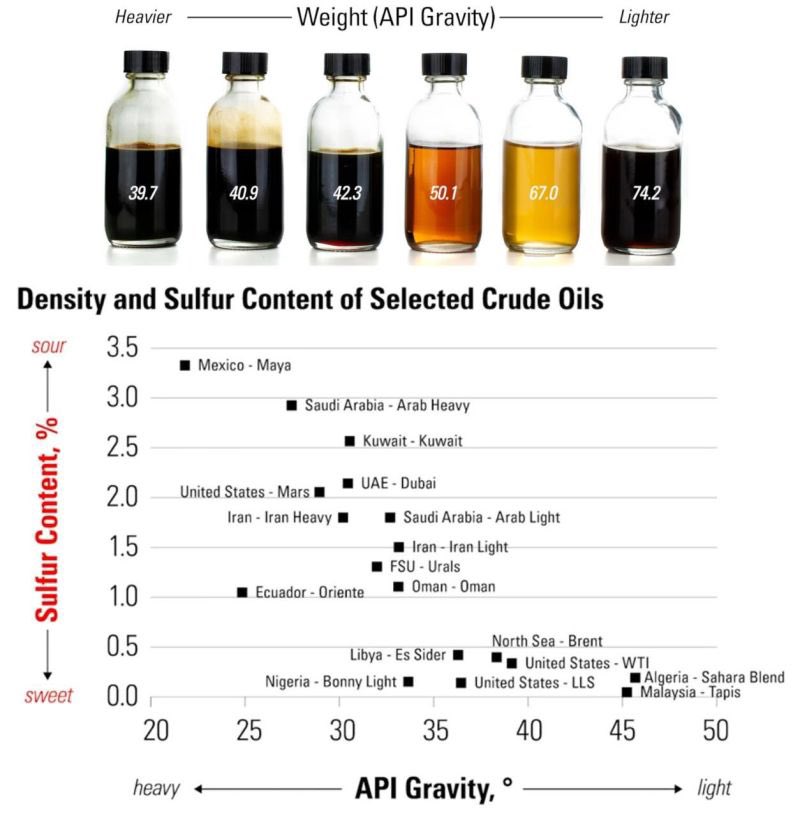

🚨Why U.S. Refineries Still Rely on Middle Eastern Heavy Sour Crude ; And Why Sour Matters for Diesel:

Despite the shale boom making the United States the world’s largest crude oil producer, America remains a net importer of crude oil. In early 2026, U.S. refineries continue to import around 6.5 million barrels per day of foreign crude while exporting roughly 3.8 million, a structural gap driven not by overall volume, but by chemistry and refinery design.

WTI light sweet crude, the benchmark from the Permian and other U.S. basins, is ideal for producing high yields of gasoline and jet fuel with minimal processing. It’s light (flows easily, high API gravity) and sweet (very low sulfur, typically under 0.5%). But most American refineries, particularly the complex Gulf Coast facilities that make up nearly 70% of U.S. capacity, were engineered decades ago to run on a blend that includes heavier, sour crudes from the Middle East, Canada, and Latin America.

⭕️Here’s where heavy sour crude becomes essential, especially for diesel production:

Heavy sour grades have higher density and significantly higher sulfur content (often >0.5%, sometimes much more). They contain more complex, longer hydrocarbon chains that end up in the “bottom of the barrel” during initial distillation. U.S. Gulf Coast refineries are equipped with advanced upgrading units, cokers, hydrocrackers, and hydrotreaters, precisely to break down these heavy residues and convert them into valuable middle distillates like diesel and jet fuel.

Sour crude’s sulfur must be removed through energy-intensive hydrodesulfurization (hydrotreating), a process that turns sulfur compounds into hydrogen sulfide for capture. This step is critical because modern environmental regulations demand ultra-low-sulfur diesel (ULSD) for cleaner combustion in trucks, ships, and heavy equipment. Without the heavy molecules from sour crude, and the sophisticated equipment designed to process them, refiners couldn’t maximize diesel output efficiently. Running pure light sweet WTI would leave expensive upgrading capacity underutilized, reduce overall yields of diesel, and hurt refinery margins.

In practice, about 90% of U.S. crude imports are heavier than domestic shale oil for exactly this reason: the blend optimizes the full product slate (gasoline + diesel + petrochemicals) while keeping costs competitive for American consumers and exporters.

Middle Eastern heavy sour barrels (from Saudi Arabia, Iraq, and others) remain strategically important not just for volume, but for the molecular profile that keeps the world’s largest refining system running at peak efficiency.

Disruptions to these supply chains, whether from geopolitical tensions or Hormuz risks, could force costly adjustments, lower diesel availability, and raise prices at the pump and for freight.

#OilMarkets #WTI #Diesel #EnergySecurity #USRefineries

As some of you are asking:

Brent (physical) trading prompt delivery: >$125 a barrel

WTI (paper) trading **May** futures: $112 a barrel

Brent (paper) trading **June** futures: $109 a barrel

(Again: WTI futures front-month is *May*; but Brent futures front-month is now *June*)

🚨 BREAKING 🚨

The Chinese government has banned all silver exports indefinitely and announced that they will pay $150 per ounce on all imports

SHFE and SGE silver prices immediately spiked to $150 on the news!

“Today’s 2 yr auction was terrible:” @pboockvar The bid-to-cover ratio was the weakest since May 2024 and dealers got stuck with the largest amount since October 2022. Traders are having a hard time pricing Fed policy as oil prices swing higher.