Markets are unpredictable, true! Also, Markets r all about patterns and tendencies that have an edge

Sharing some scenarios learned with the help of experts in my short investing& trading journey

(Only pre-requisite you’ve got to be passionate about markets😍) (1/n)

#StockMarket

When a Prime Minister tells citizens to stop buying gold, the policy stack has already moved.

India is now somewhere between step three and step four of the standard playbook. Step five is on the table.

Full transmission chain, in one article.

You Won't Be Able To Afford Gold

Grateful to everyone for helping our ET Money podcast cross 100K views. Thank you for the support, here are five key takeaways that matter most:

1. Gold is no longer a retail story anymore - the next leg to $8,000–$9,000 will likely be driven by central banks, not households.

2. Global shift toward gold-backed systems - Gold vault buildouts on the OBOR corridor strengthen our view of future gold-based net settlement mechanisms.

3. China’s surplus has limited options - with $1T+ in surplus, gold stands out over US Treasuries as a strategic reserve asset.

4. Oil, not war, drives markets - $80–85 oil could become the new normal, reshaping inflation, policy, and global supply chains.

5. Nominal GDP is the real lever - in an indebted world, higher inflation + growth is the only way governments manage debt, directly impacting valuations.

Short-term noise is inevitable, but structurally the world is shifting, towards hard assets, reindustrialisation, and a different macro regime.

Watch the full video here: https://t.co/TEuCYsgTzn

Yup

#engineering#electrification#defense#energy transition

I would add MAAS and “blue collar worker” to this list.

Indian benchmarks might not have given any returns but just look at the sectors mentioned above…

Indian benchmarks don’t have tomorrow”s winner.. so stop looking NIFT50 or BSE30….

Every time you accepted a salary, chose a price, or walked into a negotiation, the other person was running GAME THEORY in their head.

You were guessing.

This 1-hour Yale lecture by Professor Ben Polak will permanently change how you read people and make decisions.

Most MBAs pay $150k to learn this. Yale posted it for free:

Instead of watching an hour of Netflix, watch this 2-hour Stanford lecture on AI careers. It will teach you more about winning in the AI race than all the AI content you’ve scrolled past this year.

What Can Warsh Do?

By Vikas Sehgal

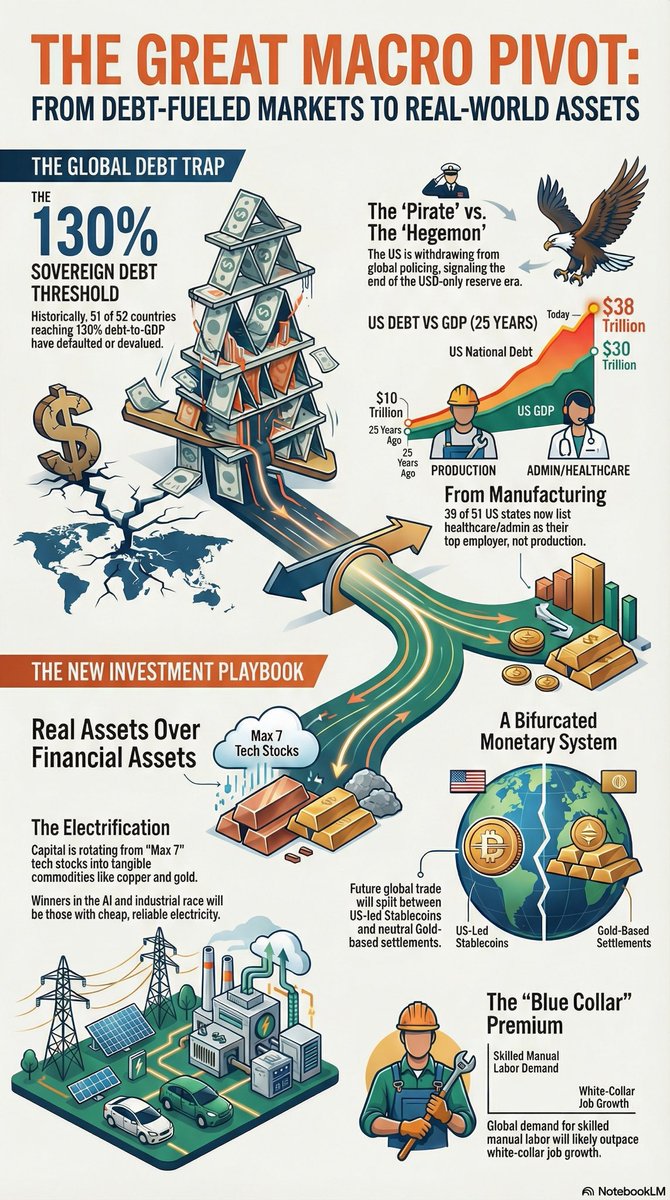

Let’s skip the complex math, the sacred economic texts, and the chanting about repo facilities. This is basic arithmetic. It doesn’t care who the Fed Chair is.

The U.S. economy is roughly a $30 trillion machine carrying about $38 trillion in debt. That debt grows by close to $2 trillion every year, automatically. Interest payments are now approaching $1 trillion annually and compounding at 15–20 percent a year. That’s impressive growth—just not the kind anyone should be celebrating.

At this point, asking what Kevin Warsh will do is like asking which button the elevator will press after the cables have snapped.

The math problem is painfully simple. The U.S. government spends about $7 trillion a year and collects roughly $5 trillion in taxes. This isn’t politics; it’s subtraction. The idea of “paying down the debt” belongs in the same museum as the gold standard and balanced budgets.

To merely stop the debt-to-GDP ratio from getting worse, the United States would need around 8 percent nominal GDP growth every year. For an economy of this size and complexity, that implies something like 5 percent inflation and 2 to 3 percent real growth—and that’s on a good day. To actually reduce the debt burden, the numbers get uglier. You need double-digit nominal growth, which means inflation north of 7 percent alongside positive real growth. At that point, the Fed’s 2 percent inflation target stops being a policy goal and becomes an aspiration.

So what will Warsh do?

Here’s the uncomfortable truth: Warsh doesn’t decide. Arithmetic does. He’s just the narrator, and there are only two possible stories to tell.

In the first story, the Fed fights inflation. Rates rise, inflation comes down, and economists applaud. Then reality intrudes. Interest costs explode, economic growth slows, markets fall, and tax revenues collapse—income taxes, capital gains, stock options, all evaporate. The deficit widens far beyond today’s already grotesque $2 trillion annual increase. Bond yields spike. The dollar wobbles. At that point, the Fed faces a binary choice: print money or default. Default is politically impossible. Printing is patriotic. The dollar dies.

In the second story, the Fed fights the debt. Rates come down and inflation takes off. Eggs begin to cost more than gasoline. Wages chase prices. Voters scream. But inflation at 7 to 8 percent performs the only remaining trick in the playbook: nominal GDP surges into double digits, and the debt suddenly looks manageable—at least on paper. Meanwhile, the dollar quietly slips out the back door. And dies.

Two paths. Same ending.

So no, the real question isn’t what Warsh wants to do. The real question is whether the dollar dies by high interest rates or by inflation. This isn’t policy; it’s choreography. The outcome is already locked in. The only suspense left is how loudly everyone pretends to be surprised.

Which brings us to India—and to you.

Warsh’s fate is sealed. India’s, and yours, is not. There’s no point debating what the RBI or policymakers should have done when the freight train was still in the distance. You should have heard it coming. Now you can see it, and it’s close. So let’s talk about tomorrow.

The survival formula is brutally simple: run, and run fast. Strengthen your balance sheet as quickly as possible. Own assets that effectively short the dollar—the larger your exposure, the better. Watch what China is doing as it buys an extra million barrels of oil a day for its strategic reserves. You may not have storage tanks, but you can position yourself in commodities or equities that benefit from a weakening dollar.

The bottom line is unavoidable. Dollar decline is inevitable. The only question is how fast it happens—and whether you get out in front of it.

Act accordingly.

( Vikas is an investor with @PineTreeMacro )

Government policy appears completely disconnected from market realities.

In a prolonged weak market, stability was needed—higher taxes were delivered.

Markets may crash, investors may lose, FIIs may exit, yet the policy response remains tax hikes.

History is unequivocal: unreasonable taxation destroys volumes first and revenues next.

The STT hike has delivered today’s bloodbath—and a clear verdict on policy failure.

₹53,000 crore - whooping STT collected last year from markets

STT was meant to remove capital gains....but now it is double taxation....!!

This is unnecessary burden on investors...

Either remove LTCG or remove STT....can't have both..

Retweet if you agree..

#abolishSTT

Who would have thought that that the value of Gold in hand of Indian households will be more more than the Marketcap of Indian equities.

If urban areas in India have financialsed due to “mutual fund sahi hai” then rural areas have still kept their traditional investments.

I don’t understand why more people don’t use Google Gemini for stock research.

Not for tips.

Not for predictions.

But for thinking clearly before risking money.

Here are 10 detailed prompts I actually use 👇