$NBIS SIGNS 18 MW CAPACITY AGREEMENT IN SPAIN 🇪🇸

Spanish newspaper El Mundo reported that Nebius agreed to the capacity with Merlin in Madrid

This marks the 5th European country Nebius will plant its flag

I don’t understand why supporters of Chinese open source keep pretending not to see what is happening right now: even Chinese “open-source” players are raising prices or gradually shifting toward more closed models.

I think China’s token dumping has already bottomed.

Just look at Zhipu, the company behind GLM-5.2. Even Zhipu has raised prices several times this year.

Chinese LLM developers cannot ignore ROI forever.

Open source is not the same thing as cheap API pricing.

So …CoPoS Mass Production 2029 H1? And glass free?? 😨😨

Then why are Taiwan’s CoPoS + glass substrate supply chain stocks are already up 5x… ?

Is it a joke?

Laura Bratton, The Information:

“Karp told me that, with Palantir’s help, some of his company’s U.S. government customers recently switched to using open-source models developed by Nvidia from proprietary models developed by the likes of Anthropic.

He said he wasn’t permitted to disclose which agencies or units he was referring to, but his other comments implied the Department of Defense was at least testing Nvidia’s models.”

“Karp told me he expects every one of Palantir’s clients, including commercial ones, to leverage an open source model “as soon as they see it as being at parity” with proprietary ones.

He said that, since the new “engine” from Palantir to improve Nemotron models was announced, his phone has been “blowing up” with calls from interested customers.”

Call me crazy, and I might be totally wrong on this, but this feels to me like a new axis of AI power is forming around $NVDA, $PLTR, and neoclouds like $NBIS.

Chips, ontology, open models, and inference. Complete sovereign AI stack. Budget friendly and secure.

With every headline like this, I see less Nebius x Anthropic and more Nebius x Palantir. Sovereign AI application layer on sovereign AI compute infrastructure.

Anthropic, right now, looks increasingly outside the Nvidia–Palantir orbit.

Again, just my read. Could be totally wrong here. Time will tell. Just think this is something worth following closely.

(Not investment advice.)

"…most AI companies are going to die - Anthropic and OpenAI give no value and take your IP"—Alex Karp

The OpenAI podcast host get nervous.

This is what happens when you are anti-open source.

Will Anthropic and OpenAI learn?

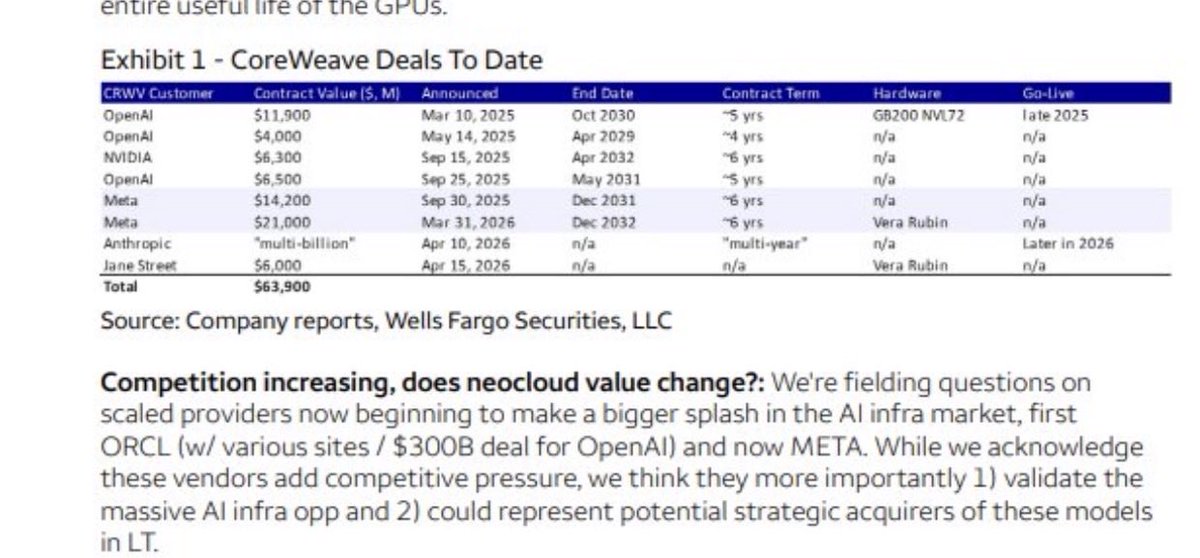

SemiAnalysis on $META “overcapacity” and market reactions with $NBIS and others:

“We believe Meta’s datacenter and compute will accelerate”.

“Capex in 2027 will be shockingly high”.

Recent global crash, especially in the photonics sector was stupid… Off misleading narratives of Meta dropping out of AI race to sell excess compute…

When in fact things are likely to accelerate from Meta catching up to GPT5.5.

I’m personally expecting a sharp V recovery, especially with the names that crashed 50%+ from this narrative.

Samsung to Raise Q3 DRAM Prices by Up to 20%, AI Demand Remains Solid

Korea's memory semiconductor industry is understood to be pushing to raise the average selling price (ASP) of commodity DRAM in the third quarter of this year by as much as 20% versus the prior quarter.

With supply shortages persisting across the entire product lineup on the back of AI infrastructure investment, memory makers are interpreted to be extending a strategy of maximizing profitability. The pace of price increases will slow thereafter, but industry sources say an extremely high profitability trend will continue into next year as well.

According to the industry on the 3rd, Samsung Electronics is in negotiations with customers targeting a Q3 DRAM ASP increase of up to around 20% versus the previous quarter.

DRAM prices have shown a sharp upward trend, driven by aggressive AI infrastructure investment from global big tech firms. This is because supply shortages have intensified across the entire product lineup, spanning not only server DRAM and high bandwidth memory (HBM) but also low power DRAM (LPDDR), which is drawing attention in the AI inference space.

Samsung's DRAM ASP increase is especially pronounced relative to SK Hynix. The industry assessment is that commodity DRAM, which carries high price volatility, accounts for a large share of Samsung's total output, and that the company has been the most aggressive in raising prices.

In fact, Samsung's first quarter DRAM ASP rose by the low 90% range versus the prior quarter. The second quarter is estimated at around 50 to 60%. Furthermore, it is targeting an increase of around 20% in the third quarter as well. SK Hynix, which has a relatively high share of HBM production, is estimated to come in somewhat below this level.

A semiconductor industry official said, "Samsung is negotiating very aggressively on pricing in the third quarter this year. We understand it will also raise LPDDR, which has recently seen severe bottlenecks in both server and mobile, by more than 20%," adding, "That said, it is not certain whether customers will accept all of this."

DRAM prices are seen as highly likely to remain stable going forward. Although the pace of DRAM price increases is gradually easing, the share of long term agreements (LTAs) signed with key customers is steadily expanding.

For example, Micron of the United States disclosed through its earnings release late last month that it had signed a total of 16 long term agreements with customers. These contracts carry binding commitments to purchase a certain volume and set a price floor that guarantees very high margins. This is interpreted as reflecting customers' judgment that memory supply and demand will remain tight over the medium to long term.

The recently raised possibility of Meta entering the cloud business is also not expected to weigh on memory demand as a negative. Some had read Meta's move to sell its internal surplus computing resources externally as a sign that its AI production capacity may already be sufficiently built out.

However, Meta has maintained an aggressive investment stance, in April raising its annual AI infrastructure investment plan from an initial 115 billion to 135 billion dollars to 125 billion to 145 billion dollars.

Another industry official explained, "With the expansion of LTAs that include price floors and HBM price renegotiations, there will be no sharp decline in the DRAM market next year either," adding, "In Meta's case, it is more accurate to view this as a way to efficiently utilize its internal computing resources."

Why markets got hit with some downside today…

So, it’s important to note that the S&P $SPX was down a mere 0.13% to end the day and is up 2.2% over the past week.

Even the Nasdaq is up 1% over the past week.

It feels like we had some momentum unwind today which is why the most high-beta names, in this case the semis, were down 10-15%.

Why the unwind?

- July is usually good month for stocks but in the past 5 years, has been down 5% on average for momentum stocks. My logic is people take profits going into the summer after a strong Q1 but regardless, July is not good for momentum historically.

- The $META news basically scared the street into thinking there are no more compute constraints and that the capex build is over.

- Nvidia launching a new product today to backstop neoclouds is once again leading to claims of circular financing.

To me, this drawdown feels normal to start July but also it is the 5th type of ugly day we’ve seen in the past few weeks where momentum just dumps hard. The bearish angle on that is the market wants to have a full correction and these dumps are a warning. The bullish angle is these dumps are very, very normal and part of a bull market. $MU having a monster earnings and taking a breather to consolidate isn’t the end of the memory trade but it is a short term stop to the massive euphoric sentiment around it. Same with the neoclouds, same with the photonics names, etc.

I think labor market news today is noise. The market might actually care but it really doesn’t. All they care about is capex because thats what stocks are priced on right now. Not fed hikes or cuts on a potentially weak labor report.

What matters deeply is if the demand side picture around compute has changed. If it has, the whole AI trade is over. If it hasn’t, then there is a long way to go on all levels of the stack but once again, the only alpha over the past few months has been taking advantage of these dips as the market has a mini deepseek every other week if they start to question the AI thesis.

Q2 earnings will be super important to continue justifying the earnings multiple expansion and capex guide but if the summer takes a breather on momentum, it feels like that’s probably the opportunity to continue gaining exposure to the broader AI thesis.

Without those opportunities, there would be a bubble since vertical moves always get punished and one could argue that we’ve gone so vertical that this type of a drawdown over the past few days is the healthy part of a bull market which creates the opportunities for it to continue.

$META CEO Mark Zuckerberg told employees in an internal town hall that AI agent development over the last four months has not “accelerated in the way we expected.” - Reuters

$META: upcoming AI model “Watermelon” has caught up to OpenAI’s GPT 5.5.

Wang noted it uses an "order of magnitude" more compute than its predecessor “Avocado”.

Who said they were out of the AI race again?

I dont think this means there isnt demand for AI compute... it just means $NVDA is trying to ensure theres competition from Neo-Clouds vs Hyperscalers... who are rapidly trying to move away from $NVDA with their own custom ASIC's.

The problem is margins. If $NVDA wants to really help the Neo-Clouds, it has to cut its own profit margins to allow for more of the Neo-Clouds to effectively compete long term.

Hyperscalers are tired of paying the $NVDA tax and while they are still friends, its likely they are also competitors... especially now with $GOOGL willing to sell TPU's and Amazon selling Tranium.

$NVDA is likely now going to push its own Open Source models that are optimized for its hardware. The reason is very simple...

If you're a software company like $NOW and will be selling both Seat subscriptions and Consumption based tokens, you want the highest margins possible to keep your margins up.

By working with $NVDA and using models like Nemotron, you can optimize for MAX customer value generation... ON TOP OF $NVDA silicon.

Todays announcement by $PLTR reflects this as well.

Wells Fargo: $META intent to sell excess compute is a positive signal around underlying demand and unit economics of AI.

“Despite this shift, we don’t expect a pullback in Meta’s capex or that overall compute needs are lower”

Regarding Neoclouds: WF thinks it validated the massive AI infra opportunity as well as acquisition opportunities. Despite any potential competition for Neoclouds.

I’m inclined to agree with Wells Fargo here and say markets completely misunderstood Meta’s excess compute comment.

For the record.

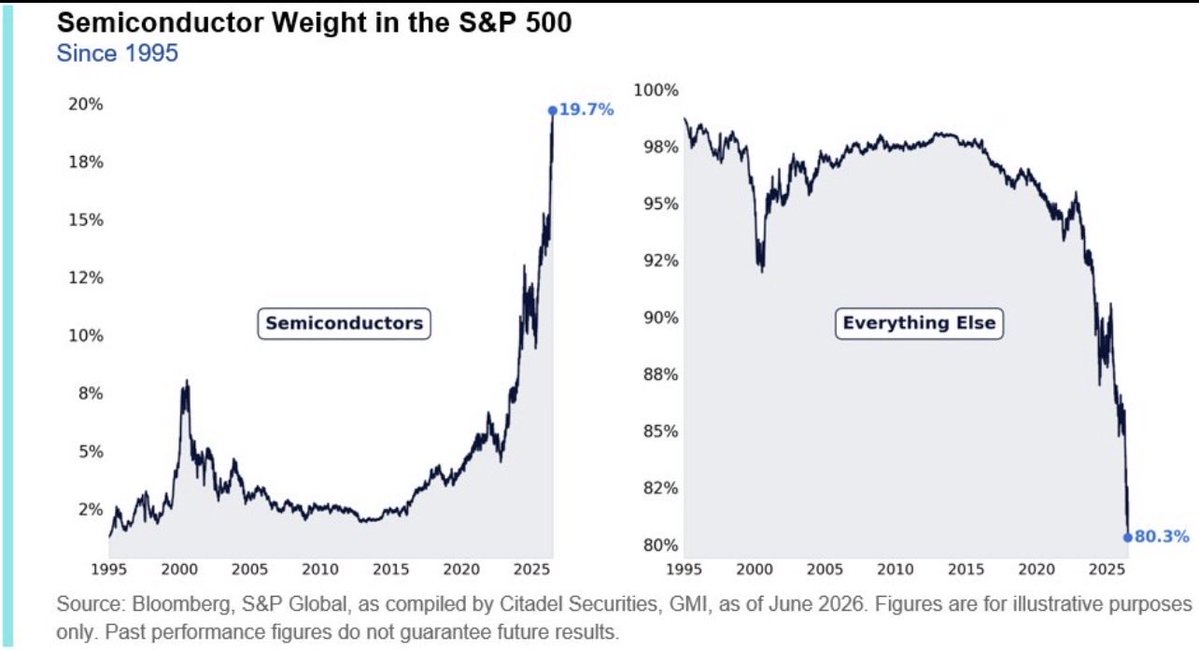

The Market Has Already Moved On

A leadership change is already

underway, but most investors are still clinging to the last trade. Everyone is crowded into semiconductors and memory, propped up by passive flows and a sell-side still extrapolating an era of outsized earnings surprises that is now behind us. The big earnings revision cycle in semiconductors and AI power is over.

The bottleneck trade is crowded and over-owned, and that playbook is exhausted. Semis now represent 20% of the S&P 500. A period of digestion is needed.

The market is broadening. Beneath the surface, the median stock is delivering double-digit earnings growth, with second-quarter earnings tracking toward 25% year-over-year. This is a rolling recovery, not a narrow AI story.

The AI cycle is not over, but it is evolving. Hyperscalers may be near a bottom and are beginning to convert capex into revenue, extending the cycle. But the bottleneck trade, owning semiconductors and AI Power, is no longer sufficient.

The era of massive upside earnings surprises is over IMHO

These stocks are crowded, expectations are elevated, and future earnings beats are unlikely to surprise as they have.

Leadership is rotating. Equal-weight indices, small caps, and domestic cyclicals are gaining traction, supported by improving earnings and still-muted positioning. Policy is reinforcing the shift, with a more Hamiltonian focus on domestic investment and productive capital.

Liquidity is also changing. Credit creation is moving from the Fed to the private sector, with bank deregulation playing a key role.

This is a more selective regime.

Investors can wait, or adapt. The market has already decided.

Woah.

Nvidia $NVDA just created a new line of business for themselves.

So, all those neoclouds like $CRWV $NBIS $IREN $APLD $SPCX that have been getting deals with hyperscalers worth billions?

It’s because demand for compute, according to Jensen, is growing at a level that is beyond imagination. So, companies need to secure more compute.

But, many of these neoclouds are struggling to finance large GPU deployments, even after securing long-term compute demand.

So…Nvidia is going to help them out and share in the upside.

“This new model enables AI clouds to procure NVIDIA infrastructure for AI-native, enterprise and ISV customers through economic alignment with a revenue-sharing and credit-support model. Through the partnership, AI clouds will sell NVIDIA-powered cloud services, with NVIDIA earning both standard product revenue and a share of the cloud revenue on the supported capacity. This structure accelerates adoption of NVIDIA platforms among the high-growth, high-conviction AI native sector, and provides NVIDIA with a recurring, usage-linked earnings stream.”

Looks like Nvidia is going to make sure the best neoclouds don’t fail and this also shifts from a one-time GPU sale to a recurring, usage-based revenue stream…which just creates many more longer-term monetization opportunities.

$nbis, $meta, $crwv, $orcl Mstanley out tonight w/ clarifying comments re: bb report. Tldr: If meta does sell compute, it will be as a bare-metal offering of spare internal 1P capacity (not 3rd party-leased) to serve as an "eps bridge" while they develop their core products.

What's key is ms doesn't believe meta can or wants to compete as a full-service stack, since their models are limited & they don't have the expertise, software, or salespeople to service specialized, high-touch enterprise inference markets (precisely the markets $nbis, for instance, seeks to serve). MS suggests meta is not contractually-allowed to resell any of their 3P leased raw silicon from nbis, crwv, orcl, etc., Believes they will save their cutting-edge contracted capacity (e.g., the nebius 12B Vera Rubin order), for internal use.

Net/net: If meta does enter the compute market it will be as a stopgap, and in the bare-metal, older chip market. A minor supply addition, at best; least threatening, arguably, to nebius of all the neo's; and all this only assuming a backdrop where the compute supply were to materially loosen.