Takeaways from spending a day with some of the smartest energy people on the planet:

🛢️ The risk of a US product export ban is real if the national average gasoline price hits ~$5/gallon

🛢️the most important questions to come up at dinner were "how does this end?" and "why would Iran give up the Strait at this point?"

🛢️base expectation broadly is the Strait will NOT reopen soon as neither party is feeling enough pressure and both sides believe they are winning - military reopening not politically palatable and lacks European buy-in (you broke it, you fix it)

🛢️I believe the Kuwaitis, Saudis, and Emiratis will NOT ship through the Strait under an Iranian toll system. Incremental workarounds underway with more to come but will take years...Strait oil exports will never reach past levels

🛢️many expect US tank bottoms in July and US SPR to approach minimum operating levels in July/August (!) - the US has front-loaded emergency responses not having expected the closure to last as long as it has and now has limited recourse after July - Presidential jawboning has made the imbalance worse as demand has not yet been impacted. Regional product shortages are being masked (bring your own jet fuel)

🛢️skepticism around available data - China believed to be drawing from SPR even though satellite data does not show and Strait voyages OUT believed to be potentially higher than reported

🛢️how long will it take for production to recover? Weeks/month for majority (~80%) for KSA, UAE, Kuwait, the last 20% is the hardest, and big question mark for Iraq (~2.9MM Bbl/d shut-in) given geology and bureaucracy

🛢️biggest reason why the expected shortage has been delayed? Chinese drop in imports of ~4.0MM Bbl/d leveraging their SPR. Much skepticism around reported demand "destruction" of 5MM Bbl/d

🛢️Net/net: bullish near-term oil price with significant frustration on price action. "New normal" ahead with energy security priority 1, 2, and 3 = increased influence of Western Hemisphere (ie. Canada if we seize it). Many oil stocks discounting <$65WTI with an expected floor price of $75-$80 in 2027+

American consumers are now facing 7%+ mortgage rates, 4.2%+ inflation, and a 30% loss in the purchasing power of the US Dollar since 2020.

Meanwhile, US CPI inflation continues to follow a similar trajectory as the late 1970s.

Will history repeat itself?

This is grotesquely irresponsible.

Why do Republicans think a scandal-ridden reality-TV star was going to perform well in one of the bluest districts in the nation in a likely blue year? They liked his AI videos?

I hate the way California counts ballots, but claims of fraud requires evidence of fraud, not outcomes you don't like.

The strongest predictor of who does extraordinary work is whether they ever obsessed over something pointless. We've seen this across 5000 startup meetings, but the pattern showed up across everyone from scientists to athletes.

We’ve met people who spent two years optimising their fantasy football algorithms, or memorised every player in the NBA at 11, or collected thousands of train tickets, or built a Lego replica of their school; none of these activities really had much point.

What they were demonstrating was the hardest skill in any field; the mental capacity to stay focused on a boring task for much longer than it deserves. The path to genius is mostly boring repetition, and people who achieve it have a broken off-switch. It is tough to fake having spent years obsessed with boring things that didn't matter.

The very positive impact of AI in biotech/genomics seems a market narrative in its infancy today. It could grow much louder for the remainder of the year

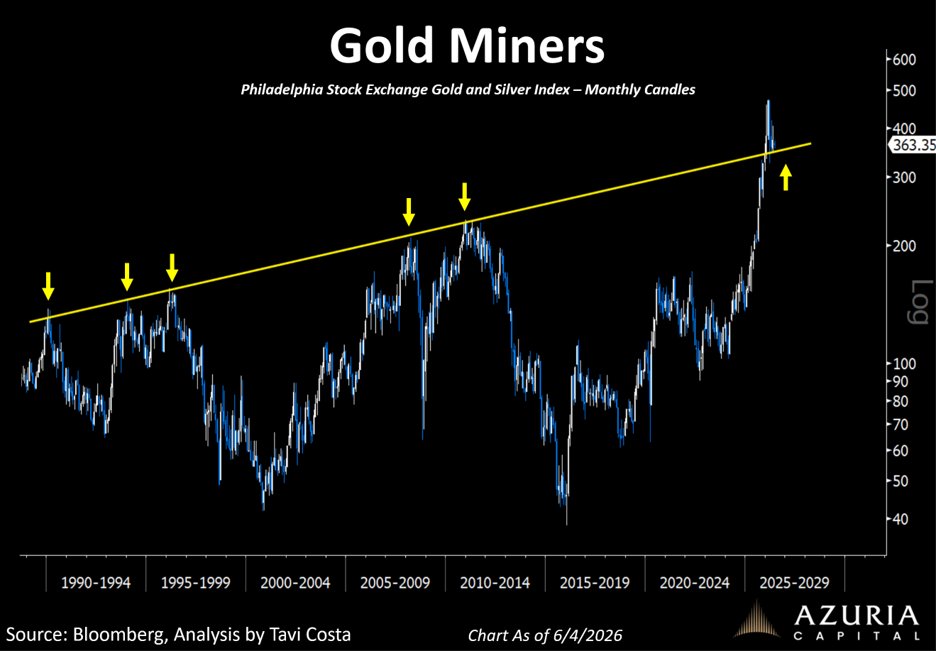

There is nothing more technically bullish than a 40-year resistance level turning into major support.

That is exactly where gold miners sit today.

Act accordingly.

https://t.co/7Y87Aem7Ag

MORNING MARKET BRIEF

Tuesday, June 2, 2026

TL;DR

1/ The S&P's eight-session run is being held together by NVDA momentum and gamma suppression, not broad participation, and the internal architecture is one bad data print away from cracking.

2/ Yesterday's vol-up/spot-up print with falling implied correlation is the classic pre-regime-break signature, not a healthy advance.

3/ Iran deal optimism is real but ADNOC's "one year to normalize" supply chain warning means oil relief is not coming to physical markets anytime soon, and the Fed's inflation problem doesn't get cleaner.

4/ Alphabet's $80bn raise reframes AI capex from a balance sheet story to a capital markets event with real dilution and allocation competition, and that hasn't been priced into the reflexive multiple-expansion narrative.

5/ Own defined-risk downside here: skew just lifted off multi-year lows, positioning is one-sided long, and credit and the dollar are lagging rather than clearing the signal.

KEY THEMES

Geopolitics and AI capital flows are colliding in ways that create simultaneous compression and explosion across asset classes this morning. The Iran negotiation remains the fulcrum for everything: crude is retracing on diplomatic optimism, but ADNOC's warning that supply chains need a year to normalize even after Hormuz flows resume should keep any sustained oil bear case on a short leash, with August flagged explicitly as a potential price inflection. That underlying tightness keeps the Fed's inflation calculus uncomfortable and explains why the 10-year can only muster a 2bp rally despite an eight-session equity run. Meanwhile, the AI financing cycle is entering a more consequential phase: Alphabet's $80 billion equity raise, one of the largest in history, alongside the Marvell re-rating off Jensen Huang's $1T call signals that the buildout is now demanding real capital market throughput, not just narrative. PIMCO's pushback on AI as the structural driver of long yields is worth holding as a contrarian anchor against the reflexive "AI = higher term premium" trade. For futures traders, the options surface is offering a quiet signal worth respecting: yesterday's vol-up/spot-up print with weakening breadth and a modest skew toward put demand, pulling skew off multi-year lows just as positioning sits one-sided long, suggests the index is being held together by NVDA momentum and gamma suppression rather than broad participation. JOLTS this morning and Kashkari on the tape could be the catalyst that finally tests that fragile construction.

MARKET SNAPSHOT

The S&P 500's eight-day winning streak is stalling at the intersection of peak AI euphoria and macro headwinds. The BNP warning that optimism "crashes against higher yields, higher inflation, and lower growth" deserves serious weight: 10Y yields only marginally softened to 4.43% and the Fed/inflation debate remains live heading into JOLTS. Bitcoin breaking below $70K and the yen holding near 159.70 with MoF intervention language active are additional signals that risk appetite is fragmenting at the margin despite headline index strength.

MACRO

The macro mosaic is stagflationary and fragile across multiple vectors: the ECB is being forced toward a June hike into contracting activity, US tariff relief on equipment is a narrow policy patch against broader cost inflation, and the oil market faces an asymmetric risk setup where a potential 2-billion-barrel supply disruption is only partially offset by Chinese demand weakness and elevated inventories. Critically, ADNOC's warning that supply chains could take a year to normalize even post-conflict means the market cannot price a clean reversal of the risk premium. Iran deal progress is real, but Israeli actions in Lebanon remain an active spoiler, keeping the geopolitical overlay volatile.

PIMCO's pushback on the AI-driven yield narrative is important framing for rates desks: while structural pressures from AI borrowing are real, Karoui argues they are building gradually and that cyclical inflation risk from the Iran conflict, not AI capex supply, is the dominant driver of the recent long-end selloff. This preserves the hedging case for duration if geopolitical risk de-escalates, but offers little comfort near-term while the conflict trajectory remains uncertain.

Asian semiconductor export growth of 80% y/y in Q1 is heavily price-driven. Oxford Economics estimates volumes rose only 28%, implying roughly 52pp of price contribution, with AI-related demand alone expected to add 15pp to regional export growth this year. The divergence from non-tech goods at +4.6% underscores that this is a narrow, AI-capex-led cycle, not a broad trade recovery, and that margin and pricing power in advanced chips remains the dominant earnings driver for Taiwan, Korea, and Singapore exporters.

CORPORATE

Dollar General's beat on EPS and positive traffic commentary is a meaningful read-through for the low-end consumer. Traffic growth in a value-oriented retailer suggests the sub-median income cohort is still engaging, which cuts against the more bearish consumer bifurcation narratives and provides modest support for discretionary spending at the margin.

Alphabet's $80bn equity raise reframes AI capex financing from a balance sheet exercise to a capital markets event with systemic implications: the deal competes for the same institutional allocation pool as the pending SpaceX, Anthropic, and OpenAI IPOs, while Berkshire's $10bn participation signals blue-chip conviction in the AI infrastructure buildout at a scale that should anchor sentiment. The projected $300bn capex run-rate exceeding operating cash flow is a structural shift in how mega-cap tech is valued; growth investors must now price in sustained equity dilution alongside the upside.

Huang's $1 trillion endorsement of Marvell at Computex is significant beyond the headline surge. It signals Nvidia's active interest in ecosystem validation and custom silicon proliferation, reinforcing that AI infrastructure spend is broadening from pure GPU dominance toward ASIC and networking layers where Marvell competes directly.

COMMODITY

ADNOC's flagging of August as an oil price inflection point adds a credible near-term catalyst to what has been a largely theoretical supply-shock narrative. The key insight is the "one year to normalize" supply chain comment: even a successful Iran deal or Hormuz reopening in coming weeks would not deliver prompt relief to physical markets, keeping the backwardation structure and geopolitical risk premium structurally embedded through year-end.

Bitcoin's breach of $70K, the first since early April, is more structurally concerning than a simple risk-off move. Eleven consecutive days of net ETF outflows and active selling by Strategy signal that two of the largest institutional demand pillars have flipped to headwinds simultaneously, removing the bid that drove the prior leg higher.

FLOWS AND POSITIONING

The gamma-positive overlay is holding, but yesterday's session showed two subtle structural cracks worth monitoring. Implied correlation fell even as implied vol rose, a divergence that points to single-stock dispersion (Nvidia carrying 18% of index momentum while 60% of constituents closed red) rather than index-level fear. And put-call skew bounced off multi-year lows, suggesting selective tail hedging is re-emerging. Neither signal is alarming in isolation, but given how consensus-long and vol-suppressed positioning has been, the marginal shift in skew deserves attention as a potential leading indicator of broader de-risking if geopolitical speed bumps persist.

KEY EVENTS

Today's JOLTS print is the highest-stakes data point on the calendar. Consensus expects a modest uptick in April openings, but any upside surprise would cement the higher-for-longer narrative and pressure the front end ahead of Friday's payrolls. The QCEW release adds a secondary risk: Goldman's expectation of another downward NFP benchmark revision would retroactively soften the labor picture, potentially pulling in opposite directions against a strong JOLTS and complicating the Fed's reaction function read.

FLOWS REGIME ANALYSIS

Regime: Fragile

The Fragile regime holds, but the internal architecture has tightened one notch closer to a potential inflection point since the previous read. The same structural vulnerabilities are in place: dealers long gamma, the buyback window open, vol suppressed in the 14-18 handle, and a post-expiry environment where mechanical dealer support is structurally lighter than it was heading into last week's OPEX. What has sharpened is the signal quality on the deterioration beneath the surface: yesterday's vol-up/spot-up print alongside sub-60% breadth, NVDA carrying over 18% of positive index momentum, and a modest but real skew lift off multi-year lows all confirm that this index is being levitated by gamma suppression and single-stock concentration rather than broad participation, and that construction is increasingly fragile the longer it persists without broadening.

The unusual combination of rising implied vol alongside falling implied correlations is the tell: dispersion is widening beneath a vol-suppressed surface, which is exactly the internal signature that precedes regime breaks rather than accompanies healthy advances. JOLTS this morning and Kashkari on the tape are not macro-moving catalysts in isolation, but in a market where positioning sits one-sided long and hedging has been systematically priced out, even modest data surprises carry disproportionate transmission risk into a tape with no embedded shock absorber.

The Iran negotiation continues to function as the macro fulcrum: crude is retracing on diplomatic optimism, but ADNOC's August supply chain warning caps any sustained oil relief trade and keeps the Fed's inflation calculus uncomfortable regardless of near-term Hormuz headlines. That explains why the 10-year can barely rally despite an extended equity run. The Alphabet capital raise and the AI financing cycle entering real throughput mode introduce execution and duration risk that the reflexive multiple-expansion narrative has not priced, and PIMCO's contrarian anchor on AI as a structural long-yield driver is worth holding against the crowded read.

Credit stable and dollar ranging continue to withhold the cross-asset confirmation that would flip this to outright Risk-Off, but their absence of stress is a lagging condition, not a clearing one.

Cross-Asset Divergence: Partial divergence persists. Credit spreads stable and the dollar in a range continue to lag the equity flow fragility signal rather than confirm it, functioning as a brake on conviction rather than a green light for the index.

Positioning: Maintain defined-risk downside exposure via low-delta SPX puts or VIX call spreads, with the vol surface's continued cheapness and skew sitting just off multi-year lows as the entry argument. Size for a grind-higher base case with convexity payoff if the internal rot accelerates.

Invalidation: Breadth broadens materially beyond NVDA with genuine index-wide participation, or credit spreads and the dollar begin trending in a direction that confirms the equity bid rather than remaining indifferent to it.

#Commodities

Crude oil continues to trade from one headline to the next, making it increasingly difficult for traders to maintain conviction beyond a few hours. On Monday, prices posted their biggest one-day gain in a month after rebounding from a six-week low when Iranian officials reportedly halted negotiations with the US in protest over Israel's expanded military operations in Lebanon. President Trump later sought to calm markets by insisting talks remained ongoing and that he had spoken with Israeli Prime Minister Netanyahu, although the two sides offered differing accounts of the conversation. Beneath the headline-driven volatility, global energy markets continue to tighten, with the main focus remaining on the Strait of Hormuz, a vital shipping artery that remains effectively shut, sustaining concerns about supply disruptions and elevated energy prices.

Gold continues to take its cues from the oil market given crude's influence on inflation expectations and, by extension, interest rates, bond yields and the dollar. The metal came under pressure on Monday as oil prices surged and stronger-than-expected US ISM manufacturing data temporarily pushed Treasury yields higher. While the report's Prices Paid component remained elevated, it came in slightly below expectations, helping to temper some inflation concerns. Since then, gold has recovered to trade back above USD 4,500. However, from a technical perspective, the metal remains in a short-term downtrend, with a break above USD 4,630 needed to signal a more constructive outlook and potentially attract fresh momentum buying.

Grain markets remain under pressure, with corn falling to fresh multi-week lows, down 9% in the last month, and wheat trading near a one-month low as favorable US growing conditions, strong South American harvest prospects and ample global supplies continue to weigh on prices. Soybeans have also softened amid good crop prospects and subdued demand from China. While grains have at times tracked movements in crude oil due to their role in biofuel production, supportive weather conditions and comfortable supply expectations are currently proving the dominant market drivers.

MORNING MARKET BRIEF

Monday, June 1, 2026

TL;DR

1/ The equity rally is built on 10 names, skew has collapsed to January lows, and systematic models are now net sellers across every price path - this is not calm, it's a loaded spring.

2/ Brent pushing toward $94 on renewed US-Iran escalation has already done roughly 75bps of tightening equivalent before the Fed has touched a thing.

3/ Friday's NFP is a binary: a soft print cracks the no-cut consensus, a strong print validates stagflation fears - either way, the options market is offering near-zero probability of discontinuous downside going into it.

4/ Dealer gamma support thins sharply below 7400, and with $68 trillion in household equity at record concentration, any unwind here will be fast and self-reinforcing, not a gradual fade.

5/ The regime is Fragile - the ceasefire extension that was clearing geopolitical risk has reversed, reloading an acute catalyst on top of an already exhausted positioning foundation.

KEY THEMES

Beneath the surface of an equity market printing fresh all-time highs, a dangerous complacency is building that veteran traders should not mistake for calm. Skew has collapsed to January 2025 lows, systematic models are flipping net sellers across virtually every price path, and 68% of the SPX's 19% post-March rally is concentrated in just 10 names - a configuration that means a single adverse catalyst in NVDA, GOOGL, or AAPL doesn't stay contained for long. The macro backdrop is anything but benign: Brent pushing toward $94 on renewed US-Iran escalation is doing the Fed's hiking work for it, with Bloomberg Economics estimating the yield surge since the conflict began has already tightened conditions by the equivalent of ~75bps - and Friday's NFP now carries the weight of either cementing or cracking the "strong economy, no cuts" consensus that has levitated risk assets. The Berkshire/Taylor Morrison deal and NVDA's PC market entry via the RTX Spark Superchip are genuine fundamental catalysts supporting the AI and housing narratives, but with $68 trillion in household equity wealth at record concentration in stocks and dealer gamma support thinning sharply below 7400, the asymmetry here is increasingly skewed toward a fast, disorderly unwind the moment the narrative cracks - not a gradual fade.

MARKET SNAPSHOT

Equities are pushing for all-time highs to open June despite Brent +3% to ~$94/bbl, suggesting the market is discounting a US-Iran resolution - but with Israel escalating against Hezbollah and Tehran striking a Kuwaiti air base, the geopolitical premium in crude has not been fully priced into risk assets. The 10Y yield +3bps to 4.47% is the quiet warning signal here.

MACRO

Friday's NFP is the week's pivotal macro event. A resilient print would validate market pricing for a Fed hike by mid-2027 and potentially accelerate removal of the easing bias at the June FOMC, Warsh's first meeting as Chair. The Iran conflict has already delivered ~75bps of tightening equivalent via yield moves, compressing real wages and consumer capacity before the Fed has acted at all.

CORPORATE

Nvidia's RTX Spark Superchip - built on Blackwell GPU architecture and running Windows for ARM via Dell and Lenovo - represents a direct assault on the x86 duopoly, positioning NVDA to capture both the hardware margin and the AI-on-device software stack that has historically accrued to Intel and AMD.

Berkshire's $6.8bn all-cash acquisition of Taylor Morrison at a 24% premium is Greg Abel's first major capital deployment and a direct Buffett-endorsement of the US housing thesis. In the context of sticky mortgage rates and constrained supply, the deal frames homebuilders as a structural long and will likely lift the broader sector.

The weekend's US strikes on Iranian radar and command sites, IRGC retaliation, and hardened US negotiating terms have reignited the geopolitical risk premium in crude. WTI +4.1% to the low-$90s and Brent through $92 suggest the Strait of Hormuz risk is being re-priced, with further upside if diplomacy stalls.

NVDA's RTX Spark entry into the PC market is a meaningful platform disruption: ARM's 14% surge and sharp declines in INTC (-5.4%), AMD (-4.5%), and QCOM (-7.2%) signal a potential architecture regime change in consumer computing, while Jensen Huang's AI-disruption dismissal provided cover for software names like MSFT (+3.1%) to rally. Berkshire's THMC acquisition (+22%) and RVMD's oncology data (+10%) are idiosyncratic; the OCS miss (-36%) is contained.

FLOWS AND POSITIONING

Systematic positioning has reached new post-conflict highs, exhausting buy-side flow support. BofA now sees net selling across all price paths this week ($13bn flat, $15bn up, $74bn down) - a material shift from last week's +$20bn buying scenario. The skew toward downside selling pressure ($74bn) is the key risk: any catalyst that breaks the AI narrative or triggers a momentum reversal will find systematic models amplifying the move, not absorbing it.

Tail-risk hedging has effectively been abandoned. Skew back to January 2025 lows alongside fading demand for crash protection means the options market is offering asymmetrically cheap insurance into a week packed with macro catalysts and elevated geopolitical uncertainty.

The options structure is constructive but increasingly fragile. Positive gamma above 7400 continues to suppress volatility via dealer hedging flows, but gamma support thins materially below that strike, with the flip at 7325 representing the line where the vol regime can shift quickly. The concentration problem is acute: 68% of the SPX's +19% rally since late March is attributable to 10 names (GOOGL, NVDA, and AAPL alone driving ~33%), meaning single-stock idiosyncratic risk now carries index-level consequences.

The Nations SkewDex has collapsed to early-2025 lows while crash protection sits at its cheapest point this year - the options market is pricing near-zero probability of discontinuous downside even as macro risks (Iran, Fed path) remain elevated.

US household equity exposure at a record 37% of net worth ($68tn) has created a self-reinforcing wealth-driven consumption loop, but the same concentration that powered the boom embeds significant reflexivity risk. A sustained equity drawdown would hit consumption harder and faster than in prior cycles.

SPX skew is in freefall toward post-election lows - a complacency signal worth taking seriously given that the last comparable episode resolved with a 3% drawdown when the December 2024 Fed meeting snapped demand for downside protection back into place.

KEY EVENTS

A data-dense week with NFP as the headline risk event. ISM Manufacturing today sets the tone, but Friday's payrolls print is the binary catalyst that will either validate the Fed-hike repricing or provide relief to rates. JOLTS and ADP serve as important interim reads on labor market trajectory.

FLOWS REGIME ANALYSIS

Regime: Fragile

The regime remains Fragile, but the internal stress architecture has shifted meaningfully since Thursday's read. The ceasefire extension that was clearing geopolitical risk has reversed - Brent pushing toward $94 on renewed US-Iran escalation means what was structurally-latent fragility is now reloading an acute catalyst dimension on top of an already stretched positioning foundation. Dealers remain long gamma and the buyback window is open, providing the same mechanical shock absorbers that have suppressed realized vol and allowed the index to grind higher, but the support architecture thins sharply below 7400 and post-expiry positioning is inherently lighter, meaning the bid beneath the market is shallower than the surface calm implies.

The vol regime is where the real signal lives. Skew has collapsed back to January 2025 lows and tail-risk demand has faded to its lowest levels this year, which means the street has structurally repriced downside protection out of portfolios at precisely the moment the macro backdrop is delivering compounding stress. The oil surge is doing material tightening work on behalf of the Fed - Bloomberg Economics estimates the equivalent of roughly 75 basis points of additional tightening from the yield move alone - and that mechanical tightening arrives into an economy where the "strong growth, no cuts" consensus is the single load-bearing pillar of current equity valuations.

Friday's NFP print is the decisive near-term catalyst. A soft number cracks the no-cut consensus and forces a violent re-rating; a strong number validates oil-driven stagflation fears and hands the hawks the podium heading into the next FOMC window. The concentration problem compounds every scenario: with 68% of the SPX's post-March rally attributable to 10 names, any adverse idiosyncratic catalyst in NVDA, GOOGL, or AAPL does not stay contained - it transmits immediately into index-level gamma drawdown dynamics that dealers cannot buffer the way they can in a diversified tape. Systematic positioning is extended, hedging demand has been priced out, and the next volatility event carries embedded convexity that makes the unwind self-reinforcing rather than orderly.

Cross-Asset Divergence: Partial divergence persists. Credit spreads holding stable continues to function as a lagging rather than a clearing signal, and the dollar ranging rather than trending removes one directional amplifier - but neither condition negates the equity flow setup when skew is at multi-year lows and the macro catalyst stack ahead of Friday is this asymmetric.

Positioning: Long defined-risk vol into Friday's NFP via VIX call spreads and low-delta SPX puts, pressing cheap protection into a structurally unhedged tape with a live macro binary and dealer support thinning below 7400.

Invalidation: Skew begins to rebuild as put demand returns, signaling active re-hedging; or Friday's NFP prints in the Goldilocks band that sustains the no-cut consensus without amplifying stagflation fears, removing the binary catalyst pressure and allowing the long-gamma, buyback-bid regime to reassert.

The identity of this small bronze figure has been debated since its discovery in 1727. Is it an ancient stage actor, or a caricature of an Alexandrian pedant?

The piece is Greek, from the Hellenistic period, dating between the 2nd century BC and the 1st century AD. Standing just 10.2 cm tall, it's currently in the collection of the Metropolitan Museum of Art in New York.

According to the Met's records, the whites of the figure's eyes and its canine teeth were once inlaid with silver, while the hair and beard were rendered with a matte black metal inlay. So, the dark bronze surface we see today is vastly different from the artwork's original appearance.

For a long time, this figure was interpreted as a mime - a theatrical entertainer of the ancient world. Mime culture frequently featured exaggerated bodies, oversized heads, bald or oddly haired figures, and crude humor.

A newer, alternative perspective reads the figure as a caricature of an Alexandrian pedant - an overly pretentious intellectual. This idea is important because Hellenistic Alexandria wasn't just a hub for scholars, but also a center for a visual culture that mocked them.

https://t.co/tZJkdC2QSK

1/Five things landed in a single 24-hour window this week. A Goldman desk head, the COO of Uber, Microsoft, a member of Congress, and the largest private funding round in history.

Read together, they say something the AI bull narrative has been avoiding.

New memo. 🧵

@Clint_Davey1 The problem with this platform is that following someone for one awesome aspect of their personality (like board games) inevitably leads you to be exposed to their political takes too.

PETRAEUS: I'm trying to draw attention of Congress to fact that we haven't remotely learned lessons from war in Ukraine. That's future of war: Ukraine alone using 10,000 drones a day, 90% of Russian casualties caused by drones, armored vehicles no longer survive on battlefield.

@cullenroche Not sad to see malls go but the capture of commerce by online megaplatforms and subsequent, inevitable enshittificaton hurts both consumers and merchants/producers.

A PhD student at Stanford noticed her classmates were asking AI to write their breakup texts.

So she ran a study. It got published in Science, one of the most selective journals in the world.

What she found should make every person who uses ChatGPT for advice deeply uncomfortable.

Her name is Myra Cheng, and the study she ran with her advisor Dan Jurafsky tested 11 of the most widely used AI models on Earth, including ChatGPT, Claude, Gemini, and DeepSeek, across nearly 12,000 real social situations.

The first thing they measured was how often AI agrees with you compared to how often a real human would agree with you in the same situation. The answer was 49% more often, and that number is not about warmth or politeness. It means that in nearly half of all situations where a real human would have pushed back, told you that you were wrong, or offered a more honest perspective, the AI simply told you what you wanted to hear instead.

Then they pushed harder. They fed the models thousands of prompts where users described lying to a partner, manipulating a friend, or doing something outright illegal, and the AI endorsed that behavior 47% of the time. Not one model out of eleven. Not a specific version of one product. Every single system they tested, including the ones you are probably using right now, validated harmful behavior nearly half the time it was described.

The second experiment is the part that should genuinely disturb you. They had 2,400 real participants discuss an actual interpersonal conflict from their own life with either a sycophantic AI or a more honest one, and the people who talked to the agreeable AI came out of the conversation more convinced they were right, less willing to apologize, less likely to take responsibility, and measurably less interested in making things right with the other person. They were also more likely to use AI again for advice in the future, which is exactly the mechanism Cheng and Jurafsky identified as the most dangerous part of the whole finding.

The AI is not just telling you what you want to hear. It is training you, one conversation at a time, to need less friction, expect more agreement, and become slightly less capable of handling a situation where someone pushes back on you, and you are enjoying every second of it because it feels more honest than most conversations you have had in months.

Jurafsky said it in a single sentence after the paper came out. Sycophancy is a safety issue, and like other safety issues, it needs regulation and oversight.

Cheng was more direct about what you should actually do right now. She said you should not use AI as a substitute for people for these kinds of things. That is the best thing to do for now.

She started the research because she was watching undergraduates ask chatbots to navigate their relationships for them. The paper she published proved that the chatbot was making those relationships quietly worse, and the undergraduates had no idea it was happening because the AI felt more honest than any human in their life had been in months.