@EhrmantrautCap_ This is crazy.

People are still sleeping on $AMPG.

And this is just one part of the call. They're also planning to expand across Europe and the UK.

https://t.co/ux7gwdlEcr

The catalysts for $AMPG are clear the coming period; new purchase orders from multiple major MNOs that will be announced in the coming quarter, on top of any other material news they may announce.

From Q1 2026 earnings call:

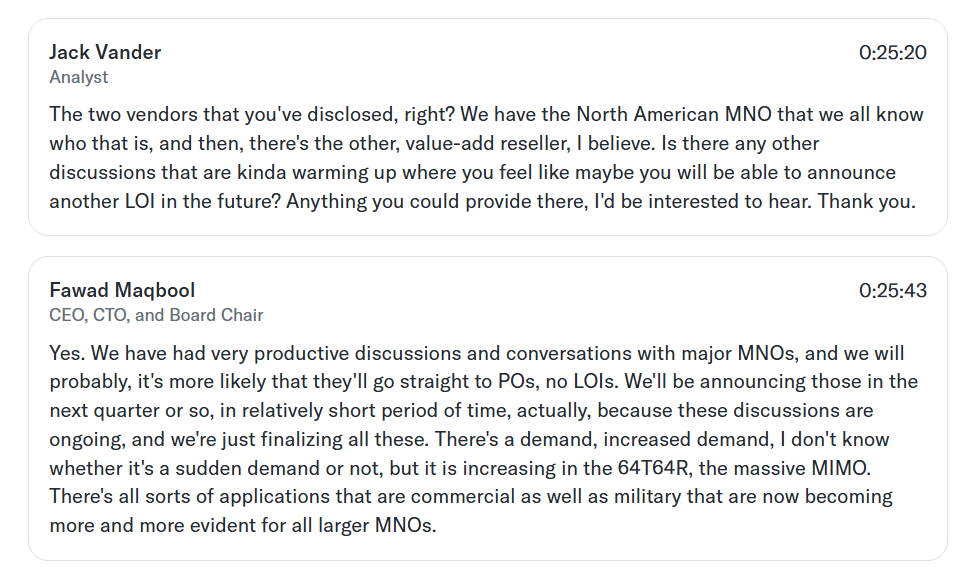

Question analyst Jack Vander: "The two vendors that you've disclosed, right? We have the North American MNO that we all know who that is, and then, there's the other, value-add reseller, I believe. Is there any other discussions that are kinda warming up where you feel like maybe you will be able to announce another LOI in the future? Anything you could provide there, I'd be interested to hear. Thank you."

Answer from CEO Fawad Maqbool: "Yes. We have had very productive discussions and conversations with major MNOs, and we will probably, it's more likely that they'll go straight to POs, no LOIs. We'll be announcing those in the next quarter or so, in relatively short period of time, actually, because these discussions are ongoing, and we're just finalizing all these. There's a demand, increased demand, I don't know whether it's a sudden demand or not, but it is increasing in the 64T64R, the massive MIMO. There's all sorts of applications that are commercial as well as military that are now becoming more and more evident for all larger MNOs."

One thing I found interesting about $AMPG recently wasn’t a product announcement, it was a strategic hire.

AmpliTech hired Asif Hussain, a telecom veteran who spent nearly 19 years at Nokia managing multimillion-dollar carrier accounts and strategic engagements.

His background includes:

• 20+ years in telecom sales and business development

• Deep experience with Tier 1 operators

• Large-scale 5G and network transformation programs

• Carrier relationships across North America, the Middle East, and South Asia

Why does this matter?

AmpliTech already has the technology. The challenge now is converting technical validation into commercial wins.

Carriers don’t award major Open RAN contracts overnight. These deals are built on years of relationships, trust, and industry credibility.

That’s what stands out about this hire.

Asif spent nearly two decades at Nokia working directly with the types of operators $AMPG is targeting today.

But there’s another angle investors may be overlooking.

Nokia is one of the largest telecom infrastructure companies in the world. Asif could have continued building his career there or moved to another established industry leader.

Instead, he chose to join a company with a market cap under $250 million that is still in the early stages of scaling its Open RAN business.

To me, that’s a meaningful signal.

People with decades of industry experience often have a better understanding of where the market is headed than retail investors do. While no hire guarantees future success, experienced telecom executives generally don’t leave stable roles unless they believe the opportunity in front of them is compelling.

Technology gets you in the room.

Relationships help close the deal.

As they expand its Open RAN and Massive MIMO efforts, this could prove to be a more important hire than many investors realize.

Why i am bullish $ASPI

The world is obsessed with GPUs, AI models, and next-gen nuclear reactors. But the market is entirely missing the single, microscopic bottleneck holding all of them back: Isotopes.

Right now, the global supply chain for these critical elements is broken, monopolized, and relies on 1940s technology.

ASP Isotopes Inc $ASPI is not just another materials company. It is a deep-tech enabler that is uniquely positioned to revolutionize three multi-billion-dollar industries by unlocking elements the world has been desperate for.

The world’s isotope supply relies almost exclusively on massive, spinning mechanical centrifuges technology that is capital-intensive, slow, and dangerously inefficient for the light elements needed for modern tech

ASPI’s weapon is its proprietary Aerodynamic Separation Process (ASP) and Quantum Enrichment (QE) technology.

Think of it as a "stationary wall centrifuge." It uses advanced gas dynamics rather than clunky spinning parts to separate isotopes with precision, efficiency, and speed that legacy systems cannot match

This technological moat allows ASPI to process gases and isotopes that others simply can’t, faster and at a lower cost.

They are bringing 21st-century physics to a 20th-century industry.

ASPI is the picks and shovels play for the most important technologies on earth. They are constructing the foundational materials required for:

Silicon-28 isn't just better silicon; it is the required architecture for Silicon Nanowires and unlocking quantum computing’s true potential. By removing noise from Silicon-29 and 30 isotopes, ASPI can enrich Si-28 purity to >99.995%

This extreme purity allows qubits to hold their entangled state for significantly longer, solving the main hurdle standing between quantum labs and commercial reality. Moreover, enriched Si-28 conducts heat far better, allowing conventional chips to run cooler and faster.

The West wants advanced nuclear reactors (SMRs) to battle climate change. However, these reactors need a specific, unavailable fuel: High-Assay Low-Enriched Uranium (HALEU) Legacy infrastructure cannot produce it at scale.

ASPI, through its subsidiary Quantum Leap Energy (QLE), is applying its technology to address the projected $37B+ demand for HALEU by 2037. QLE recently signed an MOU with a European partner for potential HALEU supply, positioning $ASPI as a strategic Western player in the global green energy transition.

The medical world is experiencing severe shortages of medical isotopes like Molybdenum-100 and Ytterbium-176, critical for diagnostics and targeted cancer therapies.

ASPI’s technology solves the light-element separation bottleneck, allowing them to produce highly enriched stable isotopes efficiently. Radiopharma currently leads their revenue narrative, and shipments of Yb-176 are targeted for 2026.

Perhaps $ASPI’s most undeniable advantage is geopolitical supply chain security.

Currently, the West is dangerously reliant on Russia and China for multiple critical isotopes. $ASPI is building the West’s only independent enrichment capacity for several of these vital elements, breaking these authoritarian monopolies.

They aren't just selling materials; they are selling national security for Western tech and energy infrastructure.

The Inflection Point is Now

$ASPI is moving from R&D to active commercial scale. They contracted Silicon-28 supply to a global semiconductor company through 2030 and beyond. Four facilities including isotope, medical, and heliumare expected to begin commercial production over the next 12 to 18 months, generating free cash flow.

Backed by a strong cash position of $333 million to scale their commercial pipeline, $ASPI is positioned as the indispensable foundational architect for the future of medicine, energy, and AI.

$ASPI #Isotopes #Semiconductors #DeepTech #NuclearEnergy #HALEU #SupplyChainSecurity #WesternDemocracies

This article is extremely bullish for Sivers. $SIVE 👀

The entire AI optics stack ultimately depends on one unavoidable reality: silicon can process light, but it cannot efficiently generate it. That makes high-performance InP laser sources a critical bottleneck for 1.6T optics, CPO and Optical I/O.

With its DFB laser arrays, partnerships with GlobalFoundries $GFS, Jabil $JBL, O-Net and WIN Semiconductors, Sivers is not merely exposed to the AI optics boom it is targeting one of the most essential and hardest-to-scale components in the entire value chain.

AI compute cannot scale without optical connectivity. Optical connectivity cannot scale without reliable light sources. And Sivers is building those light sources.

Why did I even get interested in $IQE?

When the entire market went absolutely crazy over $AXTI - I was swallowing the bitter pill of being late to that specific party.

But since I hate losing, I immediately started asking myself: what is next?

I always try to look one step ahead.

That is exactly how I managed to get early into names like $IQE or $LPKF and others before the masses caught on.

But back to $IQE - why this specific company?

The global frenzy and massive demand for optical lasers are just getting started.

The market quickly realized that Indium Phosphide (InP) - the core substrate material - does not just fall from the sky.

Hence, the massive explosive run on $AXTI.

But a raw InP wafer by itself is practically useless for high-performance photonics.

You have to actually do something with it before it can become a functioning laser.

Epitaxy.

Epitaxy is the atomic-scale deposition of crystal layers onto that substrate.

Only a handful of companies globally possess the highly specialized MOCVD and MBE machinery required for this advanced process.

One company listed on the London Stock Exchange owns a significantly larger fleet of these reactors than almost anyone else, giving them a massive structural scale advantage.

Say hello to $IQE.

Look at the pure-play competition for epi-wafers. Landmark Optoelectronics possesses far fewer machines, yet because it sits on a different exchange (Taiwan), it historically traded at multiples that make IQE look like an absolute deep-value steal.

And if you want proof of their technological moat:

IQE was just confirmed as the second largest patent filer in the entire UK for semiconductor devices.

This isn't a speculative small-cap; it’s an IP powerhouse.

Now, to be completely fair, IQE had a dark cloud hanging over it.

The cyclical semiconductor downturn cut their 2025 revenue to £97m, and because chip fabs have massive fixed costs, underutilization completely crushed their near-term margins.

Worse, geopolitical tensions flared as China introduced strict export controls on critical raw materials like Gallium and Antimony.

If you check most standard financial screeners today, that ugly debt and supply-chain risk warning still pop up.

But the market is looking backward.

First, IQE completely neutralized the China risk by successfully recycling 100% of their Gallium Arsenide and Indium Phosphide wafer waste directly back into ultra-pure raw materials for their production lines.

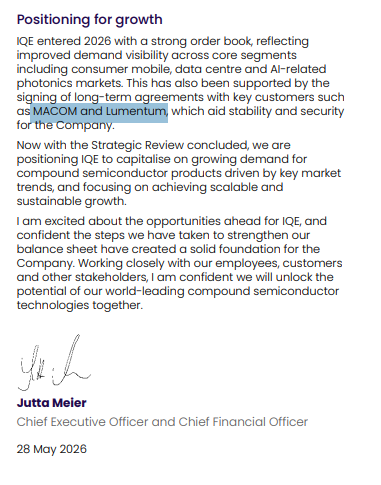

Second, on May 28, 2026 - the ultimate balance sheet reset happened.

IQE officially completed a transformational £81 million strategic recapitalization package.

MACOM Technology Solutions ($MTSI) stepped up to anchor the deal - injecting £30m in direct equity and £15m in new convertible notes to secure a ~15% strategic stake.

Existing institutional notes were swapped into equity, and the old HSBC bank debt was entirely wiped out.

The balance sheet is clean. The financial risk is gone.

So, who is MACOM and why does this partnership matter?

MACOM is a heavyweight in high-performance semiconductor products for Data Centers, Aerospace, and Defense.

They design the brains - the optical components and ICs that power next-generation networks.

By deeply aligning with IQE, MACOM secures a stable Western supply chain for advanced epi-wafers.

For IQE, it guarantees immediate structural volume demand to fill those empty reactors and unlock massive operating leverage.

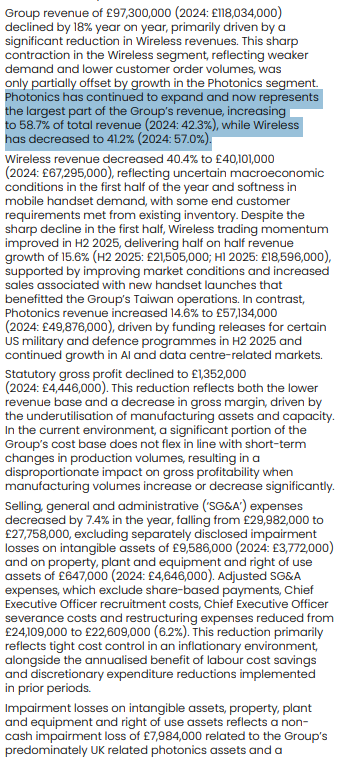

And the momentum shift is already visible.

Photonics has officially overtaken wireless to become IQE’s largest segment (58.7% of revenue), propelled by surging AI data center demand and immediate US military and defense funding releases.

Think that is all?

We got another massive confirmation of their turnaround strategy.

IQE followed this up by solidifying their multi-year agreement with Tower Semiconductor ($TSEM).

Together, they are scaling Silicon Photonics (SiPh) via the heterogeneous integration of IQE’s advanced epitaxy layers directly onto Tower’s silicon wafers.

This allows them to build optical transceivers that handle the insane data transfer speeds required by modern AI architectures.

The pieces of the puzzle are coming together perfectly.

The market is still pricing $IQE like a distressed, underutilized UK small-cap because backward-looking financial data feeds haven't adjusted to the new post-deal reality.

They are missing the bigger picture.

The debt is gone, the largest players in the chip space are anchoring equity deals to secure capacity, and IQE sits right at the choke point of the entire optical computing revolution.

While the crowd is still chasing raw substrates, the smart money is moving to the epitaxy bottleneck.

Now you understand why $IQE?

Why did I even get interested in $IQE?

When the entire market went absolutely crazy over $AXTI - I was swallowing the bitter pill of being late to that specific party.

But since I hate losing, I immediately started asking myself: what is next?

I always try to look one step ahead.

That is exactly how I managed to get early into names like $IQE or $LPKF and others before the masses caught on.

But back to $IQE - why this specific company?

The global frenzy and massive demand for optical lasers are just getting started.

The market quickly realized that Indium Phosphide (InP) - the core substrate material - does not just fall from the sky.

Hence, the massive explosive run on $AXTI.

But a raw InP wafer by itself is practically useless for high-performance photonics.

You have to actually do something with it before it can become a functioning laser.

Epitaxy.

Epitaxy is the atomic-scale deposition of crystal layers onto that substrate.

Only a handful of companies globally possess the highly specialized MOCVD and MBE machinery required for this advanced process.

One company listed on the London Stock Exchange owns a significantly larger fleet of these reactors than almost anyone else, giving them a massive structural scale advantage.

Say hello to $IQE.

Look at the pure-play competition for epi-wafers. Landmark Optoelectronics possesses far fewer machines, yet because it sits on a different exchange (Taiwan), it historically traded at multiples that make IQE look like an absolute deep-value steal.

And if you want proof of their technological moat:

IQE was just confirmed as the second largest patent filer in the entire UK for semiconductor devices.

This isn't a speculative small-cap; it’s an IP powerhouse.

Now, to be completely fair, IQE had a dark cloud hanging over it.

The cyclical semiconductor downturn cut their 2025 revenue to £97m, and because chip fabs have massive fixed costs, underutilization completely crushed their near-term margins.

Worse, geopolitical tensions flared as China introduced strict export controls on critical raw materials like Gallium and Antimony.

If you check most standard financial screeners today, that ugly debt and supply-chain risk warning still pop up.

But the market is looking backward.

First, IQE completely neutralized the China risk by successfully recycling 100% of their Gallium Arsenide and Indium Phosphide wafer waste directly back into ultra-pure raw materials for their production lines.

Second, on May 28, 2026 - the ultimate balance sheet reset happened.

IQE officially completed a transformational £81 million strategic recapitalization package.

MACOM Technology Solutions ($MTSI) stepped up to anchor the deal - injecting £30m in direct equity and £15m in new convertible notes to secure a ~15% strategic stake.

Existing institutional notes were swapped into equity, and the old HSBC bank debt was entirely wiped out.

The balance sheet is clean. The financial risk is gone.

So, who is MACOM and why does this partnership matter?

MACOM is a heavyweight in high-performance semiconductor products for Data Centers, Aerospace, and Defense.

They design the brains - the optical components and ICs that power next-generation networks.

By deeply aligning with IQE, MACOM secures a stable Western supply chain for advanced epi-wafers.

For IQE, it guarantees immediate structural volume demand to fill those empty reactors and unlock massive operating leverage.

And the momentum shift is already visible.

Photonics has officially overtaken wireless to become IQE’s largest segment (58.7% of revenue), propelled by surging AI data center demand and immediate US military and defense funding releases.

Think that is all?

We got another massive confirmation of their turnaround strategy.

IQE followed this up by solidifying their multi-year agreement with Tower Semiconductor ($TSEM).

Together, they are scaling Silicon Photonics (SiPh) via the heterogeneous integration of IQE’s advanced epitaxy layers directly onto Tower’s silicon wafers.

This allows them to build optical transceivers that handle the insane data transfer speeds required by modern AI architectures.

The pieces of the puzzle are coming together perfectly.

The market is still pricing $IQE like a distressed, underutilized UK small-cap because backward-looking financial data feeds haven't adjusted to the new post-deal reality.

They are missing the bigger picture.

The debt is gone, the largest players in the chip space are anchoring equity deals to secure capacity, and IQE sits right at the choke point of the entire optical computing revolution.

While the crowd is still chasing raw substrates, the smart money is moving to the epitaxy bottleneck.

Now you understand why $IQE?

@investingluc Well said. A successful business acquaintance has just taken his own life after getting in too deep with gambling. Wife and kids left behind