@40yoap I found it hardest to meet people on the tenure clock because I was just so stressed. Even though I wouldn’t have said I was stressed at that time, it was affecting my ability to connect with people. I think you will have that issue out of the way very soon!

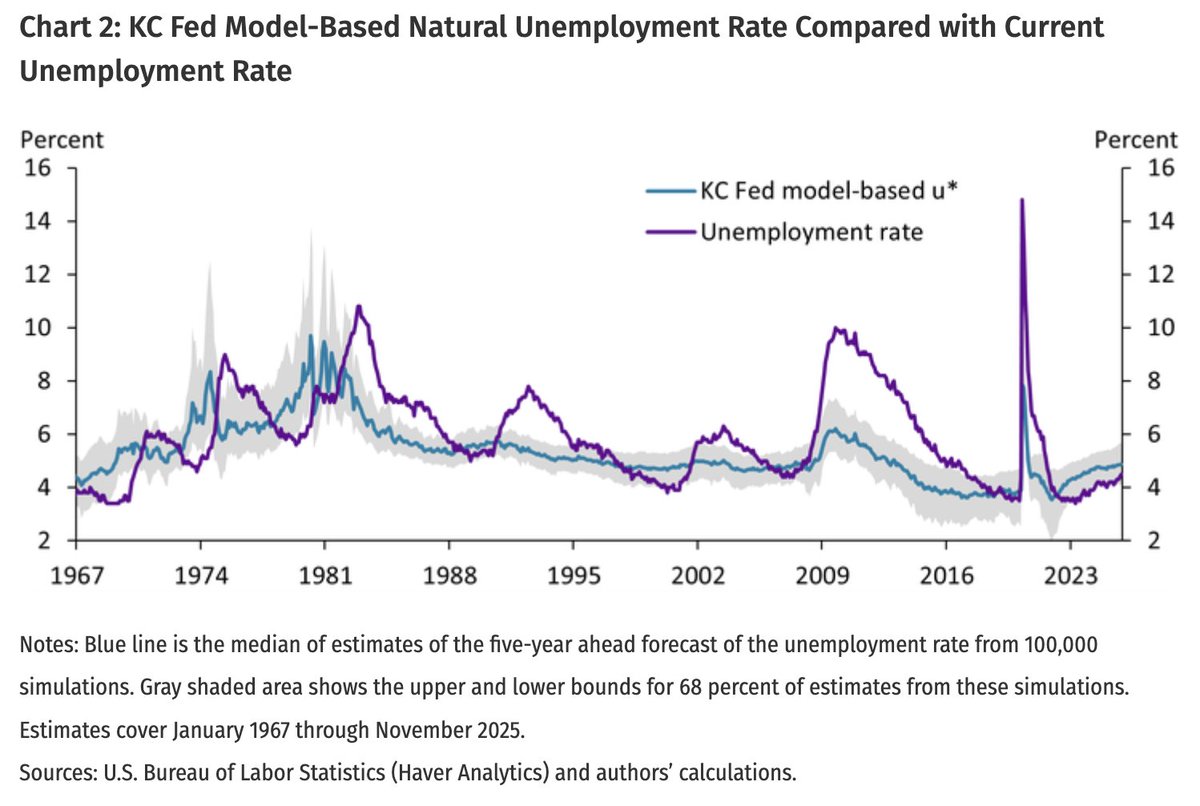

@econJaredB Thanks, Jared. In our write up (https://t.co/pMYLH6lczv), we take the credible set of u* seriously when talking about whether labor markets are tight/slack.

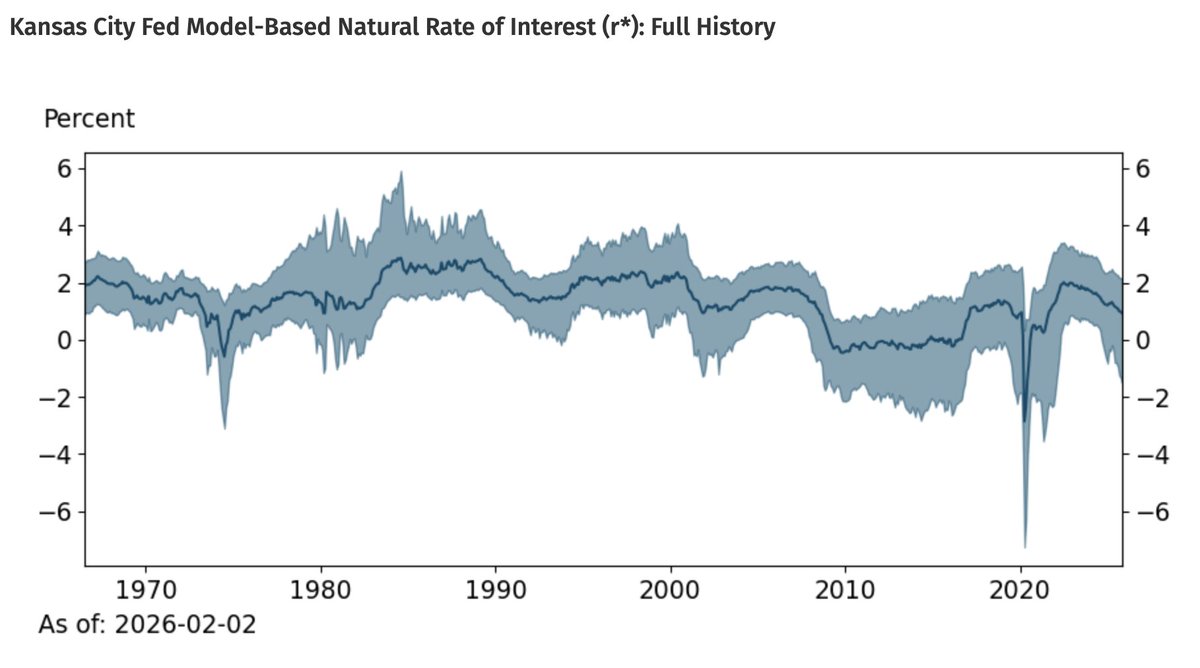

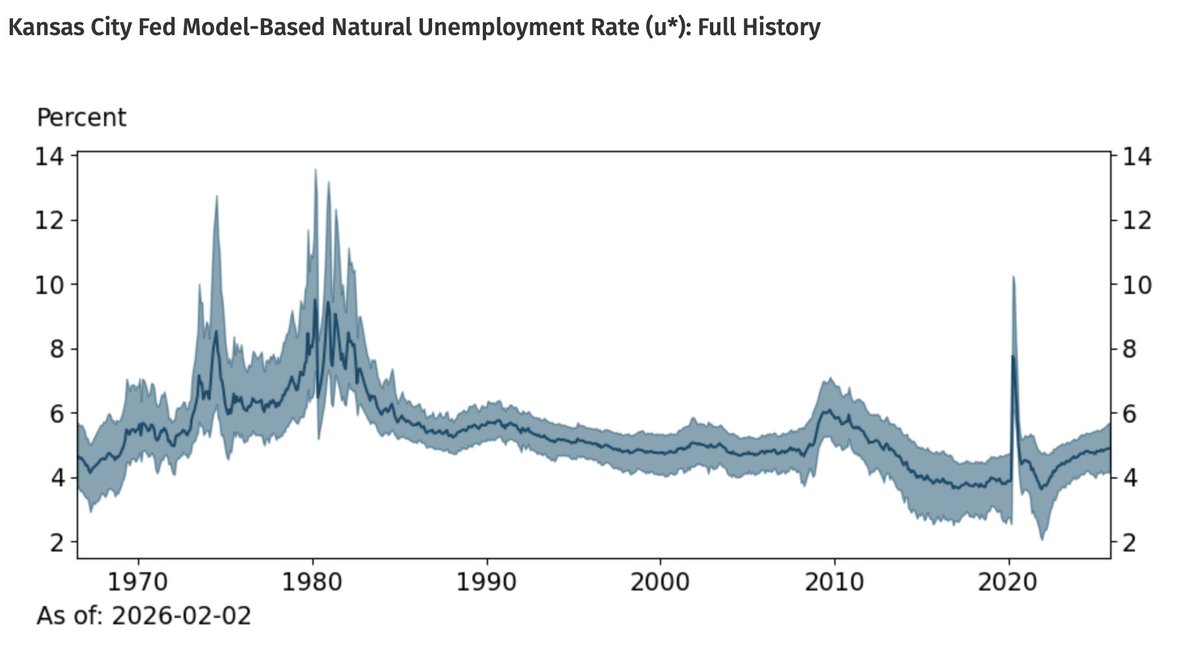

The Federal Reserve has a dual mandate to ensure price stability and full employment. But how to tell if labor markets are at full employment and how to know what interest rate achieves the dual mandate? This requires estimating two time-varying objects: u* and r*.

@lucasian76 Lubik, Merone, and Robino estimate r* measures for Canada, the Eurozone, and the UK

https://t.co/GMjpGb9P2m

But yes, the methodology could be applied to any country for which you have the relevant variables over a reasonably long period.

These series will be updated monthly from now on and available on a link that I will post in just a minute (I still don't quite know why, but people say not to post links on X).

Relatedly, the KC Fed Model-Based u* indicates that labor markets were slack for most of the 2010's even with inflation below 2% and policy rates near zero. Labor markets became balanced a few years before the pandemic, became tight in 2022, and are now roughly balanced again.

@conlon_chris@BrianCAlbrecht Hi Chris, thanks for citing us. One of our main points relates to your section 2.8 - in macro models, expectations of marginal costs affect prices today, so passthrough depends on persistence of current cost shocks and news about future cost shocks.

@t_holden I understand the theory for your suggestion, but in practice would it be very similar to using a popular “market-based” estimate of r* (like a real 5y5y forward)?

Did you read Nakamura, Riblier, and Steinsson's 2025 Jackson Hole paper "Beyond the Taylor Rule"? Check it out!

It inspired Johnson Oliyide and I to check how much post-pandemic monetary policy diverged from our own specification of the Taylor Rule

https://t.co/McEnEZtasd

Like Nakamura, Riblier, and Steinsson's, our rule prescribes a higher policy rate post 2021. Our Rule's rates differ quantitatively from theirs, which reinforces their conclusion that optimal policy may not be well described by any given Taylor Rule.

In a new Charting the Economy, we use our own monthly estimate of the natural rate to calculate the prescribed federal funds rate from a Taylor Rule that tracks r* while responding to inflation deviations from 2% and the unemployment gap.