I am very pleased to announce that "Financial Economics" has printed and that MIT Press would make it available very soon (officially, from Nov. 22, 2022)!

Great to see our research inspiring other quants! 🚀

The @quantpedia team just published an excellent deep dive on our paper “The Volatility Edge” — co-authored with @BearBullTraders and Prof. @anmele — exploring how our dual-volatility framework can be used to add a tail-hedging overlay to a passive long-term equity exposure.

Their article does a great job highlighting the key ideas:

🔹 How volatility ETFs like VIXY can serve as effective tail hedges during crisis periods.

🔹 How to balance hedging costs vs. protection, testing multiple robustness scenarios.

🔹 And how our VIX-level-based sizing approach, introduced in the paper, helps make the hedge adaptive to changing market regimes.

It’s really nice to see extensions of our base model — and to watch how others are applying The Volatility Edge framework to practical portfolio design.

You can find useful materials in the comments 👇👇

If you have any questions, don’t hesitate to DM me or reach out at [email protected]

Glad to see our nextVol model finding new market applications beyond volatility targeting. Thanks to Carlo Zarattini at @ConcretumR and Walter Distaso for the great collaboration!

❓ Can We Time Volatility with nextVoL ❓

Last week, we introduced our new volatility forecasting model, nextVoL — a tool designed to enhance the construction of volatility targeting indexes, which are the underlying assets of many Fixed Indexed Annuities (FIAs), a multi-billion dollar industry.

As we previously highlighted, nextVoL would have done an excellent job over the past 20 years in maintaining a predefined level of market volatility, with only minor deviations. A significant achievement — not only for investors, but also for hedgers who need to replicate option payoffs.

Naturally, many of our followers asked a powerful question:

Can the nextVoL model also be used to time VIX futures or VIX ETNs?

To explore this, we built a VIX equilibrium model that incorporates nextVoL as one of its key explanatory variables. From this, we derive the daily fair value of the VIX based on current market conditions.

🔺 If the fair value is above the actual VIX, we assume the VIX is underpriced and go long volatility (via VXX).

🔻 If the fair value is below the actual VIX, we assume the VIX is overpriced and go short volatility (via SVXY or similar instruments).

Despite its simplicity, this timing model proved effective. From 2008 to 2025, it delivered a Sharpe Ratio of ~1.25 with a daily hit ratio of 60%. Notably, it performed strongly during bear markets:

2008: +25%

2009: +42%

2022: +9%

Even in the challenging "Volmageddon" year (2018), losses were limited to just -1.60%.

While this is not an out-of-the-box strategy, it clearly shows that a robust risk management tool like nextVoL can also be leveraged for market timing.

Although the rules behind nextVoL are proprietary, we plan to launch a dedicated section on our website where we will publish daily volatility estimates for several well-known market indexes.

Stay tuned! If you have any questions, feel free to reach out at [email protected] or simply send me a DM here.

A special thanks to @anmele and Walter Distaso — two brilliant minds behind the nextVoL engine!

Delighted to have worked with Carlo Zarattini, the Concretum team, and Walter Distaso on nextVoL 💡📊. The results over the past two decades speak for themselves.

#Volatility#QuantFinance#RiskManagement

🎯 nextVoL: a Tool for Volatility Target Indexes🎯

A few weeks ago, we were contacted by a large institutional client active in the business of volatility target indexes and fixed index annuities.

His question was crystal clear: “Can you build a volatility forecasting model that, when deployed in a volatility target index, consistently hits a predefined yearly volatility target with great precision?”

We took on the challenge and quickly teamed up with two outstanding econometricians, Antonio Mele and Walter Distaso. Combining our experience in volatility trading and intraday modeling with the academic rigor of our partners, we started building what we now call nextVoL.

The results exceeded our expectations!

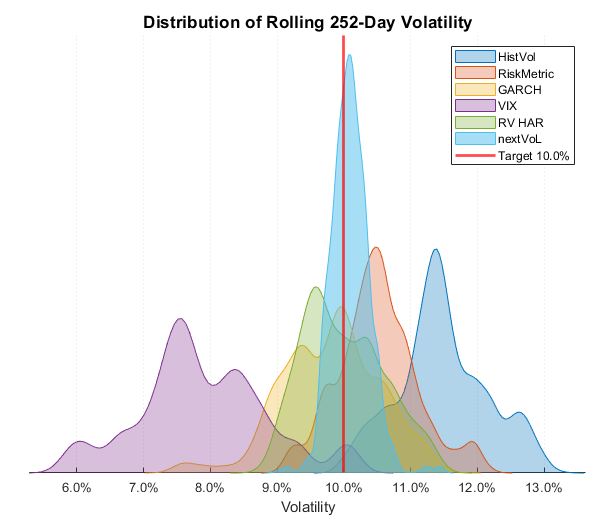

Compared with classic volatility forecasting methods such as Historical Volatility, Implied Volatility, GARCH, RiskMetrics or even High-Frequency HAR, our nextVoL approach consistently outperformed over the past 20 years.

As shown in the figure attached, the distribution of the rolling 1-year volatility of the SPX Volatility Target Index powered by nextVoL is tightly concentrated around the 10% target, with minimal dispersion. By contrast, other well-known methods either display systematic bias or excessive volatility around the target.

We also benchmarked our nextVoL against another sophisticated model developed by a leading player in this field. The outcome was clear: our model reduced forecasting error by more than 30%. Here the study is conducted on NDX 5% Volatility Target Index.

The beauty of this engine lies in its combination of intuition, practical trading experience, and high-frequency econometrics. The approach is adaptive and can be applied across a wide range of financial instruments — from equity indexes to single stocks. Updating next-day volatility estimates takes just seconds, enabling flawless alignment with market moves — whether for adjusting option Greeks, managing portfolio risk, or sizing an intraday momentum trade.

Choosing the right volatility forecasting method can significantly improve investors’ risk-adjusted returns and allow options dealers to achieve smoother, more predictable PnL trajectories.

The topic may sound complex, but we’ll be publishing some simple notes in the coming weeks.

In case you have any questions do not hesitate to contact me at [email protected]

Just completed a substantial revamp of my Market Volatility page—what happens when models hit the real world.

📄 A full PDF is available for those who want to dig deeper. 🧭 Cleaner UX coming soon.

👉 https://t.co/0oljW5vs5C

#finance#volatility#creditrisk#interestrates

Do not buy the “no pain no gain” emerging argument from the Trump team.

Sometimes the argument makes sense: A fiscal consolidation may put debt back on a sustainable course, but may also lead initially to a recession. Stronger regulation may slow activity now but make the system more resilient later.

What we are seeing now has nothing to do with this. The reason for the apparent slowdown is extreme policy uncertainty, which is leading consumers to worry, firms to wait to invest, and demand to fall. In exchange for nothing particularly good in the future. Just a pure loss.

FRB-Atlanta has now revised its real time estimate of Q1 GDP growth down to -2.8%. Surely, some of it is noise, but it is too large to be just that. I had thought earlier that the expansion would go until 2026. But the Musk/layoff/scares and the even larger than expected policy uncertainty and chaos may mean the downturn will happen sooner. If so, what will Trump do? Try hard to get the Fed to drastically cut rates? Double down on fiscal expansion? Fire Musk? To be continued.

Systematic trading is often considered as an approach to trading that is free from emotion. While it can greatly reduce the emotional rollercoaster faced by active discretionary day traders, quantitative trading also demands considerable self-discipline and control.

Simulating a 20-year backtest in just a matter of seconds can instill a sense of impatience and invincibility in quants. This overconfidence may become a liability when a strategy goes into production, as the quant then faces the slow progression of time and the temporary drawdowns that the strategy might encounter.

To address this issue, when we explore new trading strategies, we create an animated version of the backtest. The performance trajectory is revealed gradually, helping us prepare emotionally for the daily volatility our portfolio might face once it goes live.

The animation attached comes from a volatility trading program we developed in partnership with Prof. Antonio Mele, the brilliant mind behind fixed-income VIX indexes. Although historical tests were impressive, our nerves would have been tested during the inevitable drawdowns.

Looking ahead, we plan to co-publish with Prof. Antonio Mele a practical paper on volatility trading in the summer of 2025. This resource will offer traders and speculators an accessible guide to the fundamentals of volatility markets, complete with real-world insights gleaned from our own research and experience

Dear Fed: As some of us have been saying for a while, you’re well behind the curve. Inflation has been beaten; labor market weakening fast. Cut, cut, cut.

NEWS: Cboe Global Markets and @SPDJIndices to Launch New Credit VIX Indices on October 13

Learn more about the four indices aiming to track expected levels of volatility across North American and European credit markets in the press release: https://t.co/lX4ldE08k8

Lavoisier's Law

In 1774, Antoine Lavoisier showed that in a chemical reaction even though matter can change its state the total mass of matter in the system is conserved.

"Nothing is lost, nothing is created, everything is transformed."