Market buybacks are back, as SEBI notes in its meeting. As usual, I will write a Bill Ackman length post on this. You have been warned.

Buybacks are better ways to return cash to shareholders than dividends. Because in a dividend, future earnings are divided among the same number of shares, but a buyback means the company effectively reduces the number of outstanding shares (the bought back shares are cancelled), so in a buyback future earnings are spread across lesser shares.

There's a tax advantage too, now. Current taxation means long term taxes on shares you sell in the market are at 12.5% long term, 20% short term. Dividends are taxed as income so could be as much as 36%. (Promoters, if they participate in a buyback, pay 36%. For dividends, if they earn more than 2 cr. the dividend income taxation can be 39%. So it's beneficial for promoters too) And then, dividends have a TDS of 10% on payments > 5000 or so, so you get less cash.

Companies can buy back in two ways.

1) A tender issue where there's a window for everyone to tender shares, promoters too. Typically done at a premium to market price so that people will tender. This is bad - why would you prefer that your company pays more for its shares than the market is willing to allow? Inefficient, but the pro is that everyone gets a proportionate buyback so if you have 1% of the shares, you are going to get 1% of the buyback amount at least. You could get more if other people don't tender and you tender more.

2) Market buybacks means the company buys back its shares from the market itself, directly. Efficient because it uses the cash better.

Market buybacks were a pain in the previous taxation regime, where any buyback was taxed at the company level with a tax of 20% paid by the company on the buyback. But that meant only 83% of distributable cash was available to distribute. And also, because the company paid the buyback tax, shares bought from shareholders were tax-free for them.

How does this work in a market buyback? It's a pain.

You sell 100 shares. You have no idea who bought the shares. If 37 shares were bought by the company and the remaining 63 were bought by other participants in the market, only the exchange knows who bought and who sold how much.

So the exchange had to match them through a separate trading window opened for buybacks, operated by a merchant banker. The trading terminals of the exchange would display that an order was being bought by the company. The exchange would send an email to whoever sold shares to the company saying hello, you've sold X shares to the company.

Not only is this a pain, it's also gamed - since the company, brokers and the merchant bankers knew about this separate window and the purchaser identity (which isn't in most front ends of discount brokers, only in some terminals that are available to fewer people), it's also a mess that a few people could use that trading window and get lower tax treatment. A person could be almost all the volume in the regular market and still not get any shares sold to the company at the lower tax rate because they didn't use the window.

Now, it's all changed. No trading windows. No having to reveal company's identity as purchaser. SEBI fixed this.

Tax rules have changed, so market buybacks don't have the pain of having to inform people that the company matched your order. So SEBI has re-allowed market buybacks.

And then, since promoter taxation is worse, promoters being allowed to sell during a buyback would bring back the pain that exchanges would have to track every sale - therefore, SEBI says all promoter sales would be blocked during the buyback period.

Merchant bankers are no longer required for market buybacks. The company can have its own trading account and buy all their shares back. Saves fees. Saves the pain that merchant bankers know when shares are being sold or bought (reduces insider trading issues).

The buybacks now have to be done within 66 trading days, roughly three months. And 40% of it has to be done in the first half. This is there to reduce the mess of a big buyback announcement and then not actually buying. (and then going to sebi and saying oh no, couldn't buy)

A company can buyback shares only once in a six month period or so, and can't issue new shares for six months. That is in the companies act, so that will continue.

In essence, companies that have lots of cash can (and should) buy back through market buybacks now.

That's me off the soapbox for now. Put questions.

Eventually the market tells you what you should have known: the stock doesn't love you back.

Or as @CalmInvestor quotes George Goodman: The stock doesn't know you own it.

https://t.co/FSQP5na62D

the four pillars of loop engineering.

the loop itself is six lines, and nobody competes on it. every serious agent framework lands on the same tiny while-loop. model reads context, calls a tool, you feed the result back, repeat until it stops asking.

so if that part is solved, what is everyone actually engineering?

the answer is everything around the model. Boris Cherny, who built Claude Code, put it plainly. he doesn't prompt Claude anymore, he writes loops and lets them run.

that shift has a name now, and it rests on four pillars that are harder than the six lines make them look. these are the parts that actually break:

→ knowing when to stop. a terminal message ends the turn, not the task. an agent will write failing code, glance around, and declare victory. "done" has to mean the tests pass, not the agent feeling good about its work.

→ keeping the context clean. long loops rot from the inside as old outputs and dead ends pile up. a worse context produces a worse decision, which adds more noise, and the agent gets dumber the longer it runs. you fight it by treating context as a budget, not a bucket.

→ tools the agent can actually use. pile on a hundred tools and it loses track of which one to reach for. writes have to be safe to repeat, because loops retry, and a retried "create customer" call leaves you with duplicate records.

→ something that can say no. left alone, an agent agrees with itself. the fix is to separate the maker from the checker so the worker never grades its own homework.

put those four together and your job changes. you stop steering the agent move by move and start designing the system that steers it.

Karpathy runs research loops overnight that tweak a script, test it, keep what works, and throw away what doesn't, with himself nowhere in the loop. he arranges it once and hits go.

the model is becoming a commodity. the loop around it is where the real engineering lives now.

the best builders stopped asking what they should tell the agent to do. they started asking what system would do this without them.

I wrote the full breakdown. the article is quoted below.

stay tuned for more on this!

OpenAI engineer:

“90% of our engineers use Codex subagent harnesses + loops to ship code 5× faster.

close the agent loop. Give an agent a way to verify its own output.”

in 30-minute talk, an OpenAI engineer explains how to build self-improving agentic systems with harnesses.

Worth more than a $500 agentic course online.

Watch it today, then read how hedge funds apply loop engineering in trading.

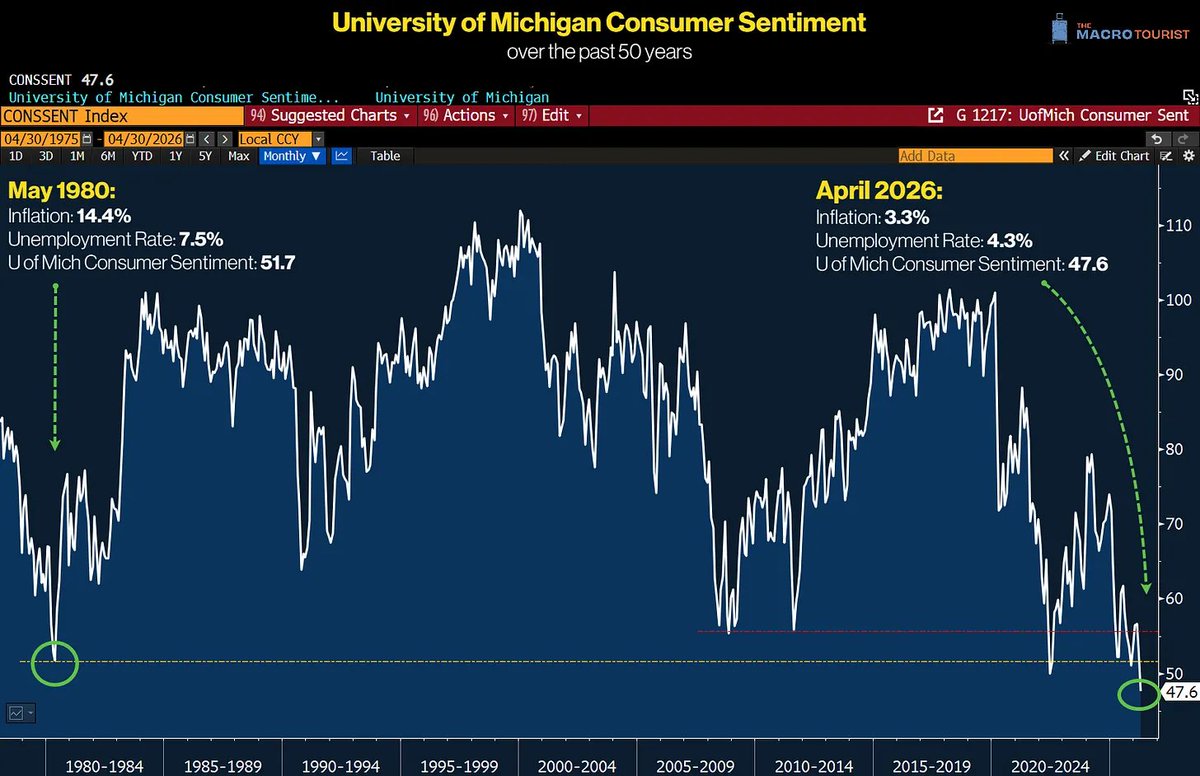

"U of Mich Consumer Sentiment hit an ALL-TIME LOW! It’s kind of shocking that today, with Inflation at 3.3% and Unemployment at 4.3% consumers feel worse off than in 1980 when Inflation was 14.4% and Unemployment 7.5%."

ht @kevinmuir

Stellar 1 yr performance across the memory & storage semiconductor industry

AI infrastructure buildout created insatiable demand for NAND flash & DRAM

One important caveat : this industry is deeply cyclical

Prices can collapse 60-70% in a downcycle as manufacturers overbuild capacity, this has happened across many past cycles (pic attached⏬)

The current upcycle is real, but it will not last forever.

So when does it top?

That's the trillion dollar question. The cycle likely stays strong through 2026 & 2027 as AI capex from hyperscalers (Microsoft, Google, Amazon, Meta) remains elevated & new fab capacity takes 2-3 years to come online.

The risk signals to watch: if AI spending growth decelerates, if Chinese manufacturers flood the market with cheap NAND, or if a technology like Google's TurboQuant which reportedly cuts AI memory requirements significantly

Most analysts expect the cycle to remain in the industry's favour through at least mid to late 2026, with 2027 being the year to watch for signs of a turn.

What do you think?

P.s. Not undermining the reforms and policies made/done/brought by the government and Indian companies but I'm trying to focus on stupid mistakes they have done which will cost us more & are creating a drag for all the work we are doing in positive directions.

As said by investors & RBI executives we are in a "goldilocks phase". I believe if this phase persists without growth rate of 7-8%+ what @Nithin0dha is saying will be seen as self fulfilling prophecy & the low hanging fruit will fix today but not tomorrow's growth.

Asked someone from the industry whether foreign investors are still interested in allocating to India. The TLDR:

Interest has pretty much died out. India is seen as geopolitically exposed, especially to an oil shock. There are no real AI plays. Valuations are rich. And the rupee situation doesn't help.

On top of that, investors who were sitting on gains have taken money off the table and are now looking at markets like Japan, Taiwan, Korea, Europe etc instead.

He also pointed out that our LTCG/STCG structure and the increase in STT have made India less attractive compared to other markets that are seeing inflows.

If we need to attract FPIs back, and we do, fixing this feels like pretty low-hanging fruit.

For Kaveri engine Govt spent is 1B$ in 20 yrs now we r importing 25B+$ worth engines bcuz it didn't do what we intended it to do. We want 70K inr earning engineer to give a product worth Billion $ & Im not ranting just a stupid investor like U, who is still ready to invests in 🇮🇳

$NVDA down 20% from highs. $MU down 20% after blowout earnings. Both stories are intact -- but oversized holders aren't sleeping.

Jim Roppel learned this with 3X leverage on 3 stocks: "Price will hurt you, but size will kill you." His max today is 18% in one name.

The stock can be right and the position can still destroy you.

Every correction is different, but investor behavior doesn’t change.

Bad investors panic and sell.

Good investors get nervous but hold.

The Best investors get excited about potential opportunities.