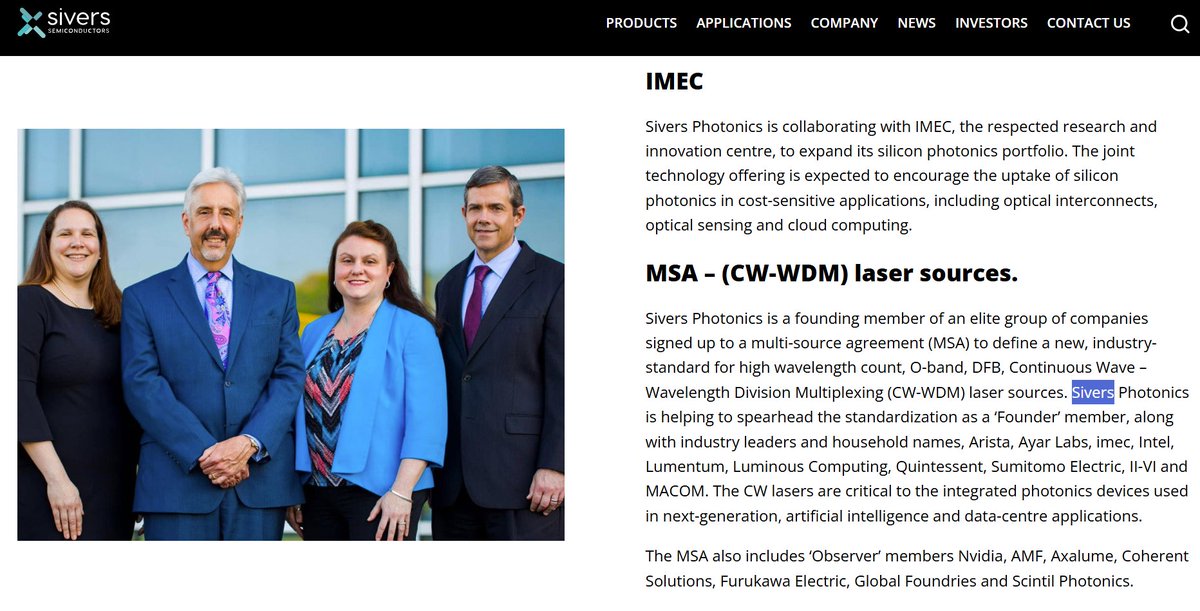

Here is the list of partnering institutions in the PIXEurope Photonic Chip Pilot Line (and yes $SIVE is there through their IMEC partnership). As structured, the funding goes to academic institutions in the network.

So, to understand which companies might benefit, you need to research the industry partners for each institution.

Luckily, I did the research for you. I only focus on EU publicly traded companies:

Sivers Semiconductors AB ($SIVE) – IMEC

STMicroelectronics N.V. ($STM) – CEA-Leti

Thales S.A.* – CEA-Leti / III-V Lab

Nokia Corporation ($NOK) – CEA-Leti / IMEC

BASF SE ($BAS) – ICFO

ABB Ltd. ($ABBN) – ICFO

I might have missed some. I would love it if folks could update the list.

*I know Thales is primarily an aerospace and defence corporation, but they co-manage III-V Lab and participate in STARLight / photonixFAB silicon photonics projects.

Might be interesting @aleabitoreddit.

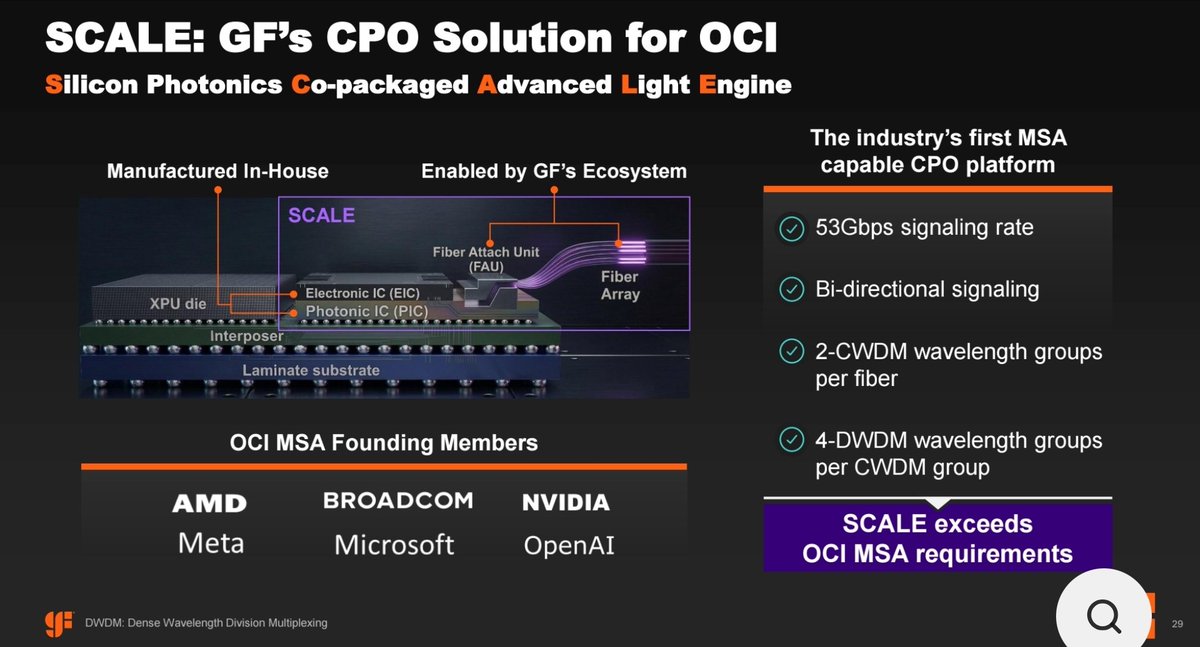

Many people read the Sivers $SIVE/GlobalFoundries $GFS PR and see "AI optics."

I see something more: GF's SCALE platform is explicitly positioned as a CPO solution for OCI (Optical Scale-Up Initiative), whose founding members are: NVIDIA, AMD, Broadcom, Meta, Microsoft, OpenAI

Hennce, Sivers $SIVE just became the first publicly named laser partner integrated into SCALE reference designs. GF CPO solution for OCI. SCALE is the Industry First MSA capable CPO platform.

OCI drives the transition from 800G EMLs to 1.6T/3.2T SiPh + CW laser architectures, this partnership hence is highly strategically important.

Not just a partnership announcement, it is an ecosystem announcement.

"Sivers’ laser arrays will also be available in GF’s Silicon Photonics Co-packaged Advanced Light Engine (SCALE™) platform for next-generation optical sub-assemblies and light engine architectures":

https://t.co/MKT1Lu4evA

"Optical Scale-up Consortium Established to Create an Open Specification for AI Infrastructure Led by Founding Members AMD, Broadcom, Meta, Microsoft, NVIDIA and OpenAI"

https://t.co/9KeYxFJ4b4

We're excited to announce a strategic collaboration with @GlobalFoundries to develop advanced silicon photonics solutions for the rapidly growing AI infrastructure market.

Our laser arrays will support next-generation optical connectivity architectures, including CPO, LPO, and other emerging data center interconnect solutions, while complementing GlobalFoundries' silicon photonics platform and SCALE™ optical engine offerings targeting a projected $25 billion pluggable optics market by 2030.

For full details, visit: https://t.co/rDAFqiG85m

DID YOU LISTEN ANON?

Reuters: New Sivers x GFS strategic collaboration.

$SIVE has now announced its lasers will be integrated into reference designs built on Globalfoundries Silicon Photonics Platform.

For pluggable optical transcivers, CPO, and SiPH.

This is fundamentally the most groundbreaking news for Sivers in history.

As Broadcom, Nvidia, Marvell, AMD, and anyone who goes through GFS silicon photonics has Sivers embedded as a default laser route.

I personally think this news alone should easily 2x or 3x Sivers market cap over the medium term, given how fundamental this is to their revenue.

To have Sivers be the standard laser route for the many hyperscalers that use the world's leading photonics foundry.

Holy crap, this is the most bullish thing I’ve heard from $SIVE so far.

From earnings transcripts:

“We do not look at competitors when demand far outstrips supply” (literally anything they make gets bought)

Along with: “We see 60% gross margins in the future” (incredibly high)

“We have two technologies that can feed into these three supercycles that are currently going on.” (Holy revenue opportunities)

My high conviction CPO/photonics long is $SIVE for a reason.

$SIVE - PHOTONICS LASER SHORTAGE IN 2030 BY ALMOST 50%

$NVDA wants suppliers of InP lasers to increase capacity by 20x through 2030 to support AI cluster networking. They agreed to 12x. This clearly means a 40% shortage.

In such circumstances, how can one not be bullish for $SIVE? 😍 They make exactly these types of InP lasers for future 1.6T+ transceiver architectures & CPO programs.

They are a chokepoint for many supply chains mapped directly to hyperscalers and OEMs out there.

The thesis that it could be the next $LITE is by no means shallow. There is definitely more realness to it than ever before as we keep seeing huge signals coming our way, every few weeks.

For those wondering what $CANATU actually does and is, here's a rough breakdown.

Canatu is a Finnish deep-tech company, an Aalto University spin-off that's been quietly working on carbon nanotubes since 2004. That long, boring history is the whole reason almost nobody owns it. It spent most of its life in a lab. It's only now reaching the point where two decades of R&D and roughly €100M of investment start turning into real industrial revenue, around €20M last year, growing fast, almost all of it from semiconductors.

The simplest way to understand the business: the most advanced chips in the world, the ones in NVIDIA's AI accelerators and Apple devices, are made using EUV lithography machines, built only by ASML. Inside each of those machines sits a consumable part that protects the most expensive component, the photomask, from a single speck of dust ruining a wafer. As the machines get more powerful and run hotter, the current version of that part starts to fail. Canatu makes the technology for the next version, one built from carbon nanotubes that survives the heat and lets more light through. So without touching the chemistry: AI needs chips, chips need these machines, the machines need this part, and the old materials are hitting a wall. Canatu sits exactly on that wall.

What makes it a business rather than just a clever material is the model. Canatu doesn't manufacture and ship the part itself. It sells a reactor to a partner, sells the proprietary inputs only it can supply, and then collects a royalty on every single unit the partner produces. One sale becomes three revenue streams, and the best one, the royalty, recurs with almost no cost or manufacturing risk attached. The partner carries the factory, the capital, the geopolitics. Canatu owns the IP and clips a fee off everything that comes out. That's a capital-light, high-margin, recurring structure, and if volumes scale it becomes very valuable.

It's not theoretical. The model went live in October 2025 when a Korean partner, FST, took a commercial license, and FST is notable because Samsung holds a stake in it, so Canatu is effectively plugged into Samsung's supply chain without ever being a named supplier. Management has hinted at a second major Asian customer in qualification, widely suspected to be Taiwanese.

The moat is two things. First, the manufacturing process, they grow the nanotubes dry, in the gas phase, with no liquid handling and no transfer step, and it's that transfer step where competitors pick up defects and contamination. Second, the know-how is held as software-controlled trade secrets on top of 300-plus patents, so even handing someone the reactor doesn't hand them the recipe. There's also a geopolitical wall: the tech can't be sold to China, and the membranes only work on ASML machines China can't legally buy anyway.

Beyond semis there's optionality. An automotive arm (sensor and windshield heating, a confirmed DENSO partnership, plus next-gen solar cells targeting ~33% efficiency vs silicon's ~25%) and an early medical-diagnostics arm (a fingertip blood test aiming for lab-grade sepsis detection in minutes). Interesting, but the semiconductor story is the one that matters for the thesis.

Now the competitive picture, because it matters. Canatu isn't the only one working on this. Mitsui, the incumbent pellicle maker, is developing its own carbon-nanotube path with imec, specced for very high power. But the two aren't quite the same bet. Mitsui wants to be the supplier, it makes and sells finished pellicles. Canatu licenses the process so others can make them in-house and collects a royalty. So the way to think about Canatu is as the independent route into this, the option that lets a fab or partner build the capability themselves rather than depend on a single finished-goods vendor. In a supply chain this strategic, where no one wants a single point of failure on a critical consumable, having that independent alternative is exactly what the downstream players want, and the licensing model means even a modest share compounds over time.

A few things to keep honest before anyone gets carried away. The inflection got pushed from 2027 to 2030, so this is a multi-year hold, not a quick re-rate. The company still loses money as it builds capacity, normal for the stage but it demands patience. And the share count is the detail most holders miss: because of how it came public, warrants and earn-outs issue more shares as the price rises, so the realistic fully-diluted figure is closer to 44-46 million than the ~34 million your broker shows. If you're doing the math, use the bigger number.

And the most recent signal: a new CEO, Dr. Maximilian Slawinski, just took over from Soitec, a company whose entire competence is scaling advanced semiconductor materials from "we can make a little" to "we can make a lot." That's precisely the problem Canatu has to solve next. Right hire, right moment.

That's the rough shape of it. A pick-and-shovel sitting at a real bottleneck in the AI chip supply chain, with a smart capital-light model, genuine competition, a multi-year timeline, and a dilution structure worth understanding before you size anything.

DYOR, NFA.

Jason Chips technical bear case on $SIVE is sloppy.

1. Casts SIVE as a pure WDM-array bet. Their own datasheet lists 70mW & 100mW single DFBs for 800G/1.6T, not just arrays. Same dual-architecture spread as Lumentum.

2.The 65mW figure is a 2023 Ayar Labs array demo. Stale + cherry-picked.

3.“WDM = wrong architecture” is a timing call, not a truth. NVIDIA chose micro-ring modulators because they’re WDM-native (8–16λ/fiber). And Lumentum, your hero, demoed a 16λ UHP ELSFP at OFC 2026.

4.Lumentum UHP is 350mW@50C, not 100mW.

The technical bear case framing here is sloppy:

https://t.co/qYM5ArMtSB cast SIVE as a pure WDM-array bet. Their own datasheet lists 70mW & 100mW single DFBs for 800G/1.6T — not just arrays. Same dual-architecture spread as Lumentum.

2.The 65mW figure is a 2023 Ayar Labs array demo. Stale + cherry-picked.

3.“WDM = wrong architecture” is a timing call, not a truth. NVIDIA chose micro-ring modulators because they’re WDM-native (8–16λ/fiber). And Lumentum — your hero — demoed a 16λ UHP ELSFP at OFC 2026. The “winner” is building the architecture you call wrong.

4.Lumentum UHP is 350mW@50C, not 100mW. You understated your own strongest point.

Long $CANATU at ~€280M market cap.

My read: this is the pure-play enabler sitting at the EUV bottleneck, and the market hasn't priced it. $CANATU owns the only commercially available CNT reactor technology for high-power EUV pellicles, about the narrowest chokehold there is in the advanced-chip supply chain.

The setup is simple. Advanced logic fabs (TSMC, Intel, Samsung) are on track to print ~$800B of EUV-dependent AI chips by 2030. Canatu's CNT pellicles give 8-15% higher scanner productivity at 600W+, exactly the direction High-NA EUV is heading. Traditional pellicles don't survive the heat and transmission loss at that power.

What that edge is worth to the fabs:

8% = ~$64B/yr

11% = ~$88B/yr

15% = ~$120B/yr

Tens of billions in incremental wafers, more good die, capex avoided, every year. It dwarfs the €1.5B pellicle TAM itself. The productivity edge also justifies premium pricing on the pellicles (which expands the TAM), and Canatu sits one layer upstream with the reactor and IP. Even a conservative 20% value capture via royalties plus recurring consumables points to €400-950M revenue in a bull ramp.

The valuation doesn't add up for me. A company supplying the irreplaceable IP that lets the biggest foundries run their most expensive tools at full speed, trading at ~€280M while taking the high-margin recurring slice of a dominant share of an exploding market.

Two weeks ago they made a quiet but important move. Dr. Maximilian Slawinski came over from $SOI (Soitec) as CEO on May 11. Not a placeholder hire. Soitec is the playbook for scaling engineered semiconductor materials, exactly the skill set Canatu needs moving from reactor deliveries and SATs into full commercial qualification, volume ramp, and the royalty inflection. If you've been watching the $SOI materials story, this is the same DNA pointed at the EUV pellicle chokehold.

On guidance: official 2030 target is €100-150M revenue at 25-30% EBIT. The chokehold math says there's clear upside if CNT adoption and pricing run even moderately ahead of that. A bull ramp gets you toward €500M+ revenue by 2034 at 40%+ margins on the recurring model. Fortress balance sheet (~€92M cash) and gross margins already at 72.5% on the licensing mix.

Risks, because they're real: execution, as always EUV scanner ramp delays (the 2027 targets already slipped to 2030) dilution to fund the production scale-up broader semi cycle slowdown

I genuinely don't get how pre-revenue or far less differentiated names carry multi-billion valuations while $CANATU, the actual enabler at the narrowest point of the EUV/AI chip bottleneck, sits at ~€280M. My guess is it's still largely undiscovered by institutions because it's a Finnish micro-cap on OMX Nordic. I think that shifts as the 600W+/High-NA ramp accelerates and the recurring royalties start landing, especially if CNT becomes the default pellicle for next-gen AI chips.

If advanced EUV stays the gating factor for AI compute, $CANATU, with its patented Dry Deposition process and the only commercial CNT reactor solution, has room for a real rerate.

Position is my own. DYOR, NFA.

TLDR: EUV pellicles are the current bottleneck as AI wafer demand runs hot. The 8-15% productivity edge $CANATU delivers is worth 64-120B a year to the fabs, which makes a ~€280M market cap look absurd for the enabler sitting at the chokehold. New CEO came straight from $SOI (Soitec), the materials-scaling playbook, now pointed at the pellicle bottleneck. I'm long because I think they're a primary beneficiary of the EUV scaling the market is still asleep on.

$JBL literally announced in their fireside chat…

Mass production of their 1.6T LRO with excessive demand in 3-10 months.

$SIVE is likely sole source laser supplier for this specific optical transceiver.

Ayar raised $500M for volume ramp recently, and $SIVE is the primary / sole source laser supplier.

2025 annual report, $SIVE signaled start of volume ramp with both (likely) $AEVA and $POET.

This is how you do supply chain mapping on qualification cycles.

Anything they make, Sivers makes revenue off lasers.

If you ask AI they will keep confidently citing 2024 revenue numbers without knowing volume hints.

Which is why I keep seeing these false claims like this over and over, despite Sivers being on the precipice of mass production for 2027.

For people trying to do valuation analysis on $SIVE.

Ayar, Celestial, Lightmatter, Lightelligence are probably valued probably ~$4B-15B+ today.

Sivers is ~$2.6B MC and they're likely upstream laser for them all.

I'm not even including Poet, TFLN links like Hyperlight/Lightium, or pluggables like Jabil + other undisclosed players in valuation analysis.

Or their other segments like CHIPS Act contracts or Apple/Nokia relationships.

Or humanoid/physical AI segments with Aeva + others.

Retail aren't as familiar with private markets...

But these companies are all considered the frontier CPO players, and are growing valuations/scaling rapidly.

So, I'd expect $SIVE to command similar if not higher valuations given laser chokepoint premiums. Especially after they pull off M&A to TAM expand revenue.

New Blackrock/Vanguard/MSCI/NASDAQ inflow next month helps close that gap over time.

But NASDAQ listing is probably what gives Sivers a premium.

I’m not selling a single share of $SIVE.

I personally think it’s a once-a-generation long given how many hyperscaler suppliers they’re already in.

Coupled with GS extreme TAM expansion projections for both pluggables and CPO in the next 2 years.

If you didn’t read the $JBL fireside transcript by now validating demand/timeline.

Or the fact Ayar removed Lumentum and Macom from their website as laser suppliers validating moat.

Or literal CHIPS ACT funding validating technological importance.

Or that management is literally doing everything right in my view, with NASDAQ listing into M&A focus, validating forward growth vision.

Upside is just way too compelling at current valuations.

Institutions have barely entered yet as well… and we’re about to see tens of millions of passive, long term new inflow next month from Nasdaq, Blackrock, MSCI indexes.

Photonics is nuanced and using ChatGPT/Gemini makes you miss all of it:

1. $SIVE is actually a chokepoint and partially a bottleneck.

The reason it's a chokepoint is leading CPO/optical hyperscaler players go through Sivers, likely:

Ayar. Celestial. Lightmatter. Lightelligence. Poet.

If you take out Sivers, you literally can't make some of their products + delay their roadmap by years.

As many are sole/primary source but are heading the direction on multi-source.

As for the bottleneck argument: Win Semi is the bottleneck for scaling laser production.

But... the nuance is when you have capacity allocated for the next few years.

You become part of the bottleneck itself if players fight you for allocation of finished lasers.

That's the nuance people miss with capacity allocation dynamics.

It's like saying $SNDK is not part of the NAND bottleneck when Kioxia makes all of it.

But when Sandisk has the ultimate control of output supply, they become the bottleneck + have all the pricing power.

Sivers controls output supply of CW lasers given allocations, and as seen with $LITE earnings, CW laser is currently bottlenecked as everyone seems to be stuck producing EMLs.

2. Like how LLMs always uses em-dashes.

You can tell when people use AI when they always use the same "CW is a dumb interchangeable laser" argument or compare "power" specs after conflating different architectures.

That's why your "analysts" using AI will get this wrong over and over.

There's CW lasers... and then there's a specific architectural design that Sivers achieves with DFB lasers.

If you compare power specs with $LITE vs. Sivers, Lumentum wins in isolation. But they're completely different laser architectures.

All the leading CPO players like Ayar, chose $SIVE for an architectural reason for high power, low thermal, laser arrays. $JBL 1.6T LRO also made one of the most dramatic moats cited by their fireside chat, using Sivers lasers.

If you think CW lasers are interchangeable with Sumitomo/Furukawa, and others. And can be plug-and-play... i don't know what to tell you?

Again: $SIVE makes architecturally unique CW lasers for leading CPO players.

3. I'm not sure how many times I need to say this:

$SIVE for 2024-2025 has been going through development contracts. People using TTM revenue or former P/S metrics are using completely the wrong metrics, when there's volume ramp in 2027.

It's the same with $AAOI which volume ramps in H1 2027.

$AEHR which volume ramps after qualification.

$LPK that volume ramps after qualification.

This is just missing qualification cycles in semiconductors and how to model financials currently.

As for the $LITE comparisons (which was also my long last year):

$LITE literally started off selling laser dies before acquisition of Cloud Lite and other downstream optical engine components.

This is where $SIVE is at today with starting off in the laser chokepoint for CPO:

People are modeling laser revenue off very isolated TAM projections. Meanwhile Sivers is targeting M&A to expand revenue for TAM projections.

This is not a simple component FAU + ramp valuation modeling over with a Taiwanese company.

Since Laser companies like $LITE, $COHR are known to downstream expand to make their lasers more valuable, then vertically integrate (fabs, assembly) afterward.

Again, Sivers worked with Ayar and these types of companies before they all became billion dollar companies. I have high conviction knowing they know what to acquire down the ELS/optical engine stack + pluggable transceiver for TAM expansion.

It's just annoying when I get people who don't understand the nuances backseat commenting wrong things about my longs.

I got the same thing about $AXTI is not a bottleneck! InP isn't needed! China! back at $14.

Now it's $140

I got the same thing about $AAOI "is going down 50%!" back at $65. or "AOI management is shady at $30".

Now it's $170

I got the "there's nothing new with $SOI" back at $45.

Now it's $170.

I think I'm one of the few who actually understands the nuances with photonics, since I did call out $LITE, $TSEM, Innolight, $AXTI, $AAOI, $SOI, that outperformed both photonics markets and overall markets over the past year.

And now I'm long on $SIVE.

For $SIVE to become the next $80B+ $LITE.

Sivers is the current laser kingmaker of the optical transition to CPO and 1.6T.

They basically supply lasers to the leading players in the CPO space.

From likely $MRVL Celestial, Lightmatter, Lightelligence, $POET, and others for CPO. before they got big.

And now with large players like $JBL for 1.6T LRO + more test/qualifications underway for pluggables.

They've finally solved the Catch22 problem, and have the attention of the market to pull off foundational CPO related IP acquisitions downstream on NASDAQ listing (or now with equity).

And expand revenue as much as possible from the laser source into:

-> Optical Engine/ELS value.

-> Optical Transceiver IP

Just like $LITE did to drive their valuations from $2B -> $80B in 2 years.

But instead of EML + pluggables, Sivers is doing this for the CPO supercycle, the fastest TAM expansion in history for photonics.

I'm following the story for them to pull this off this David vs. Goliath shift catching up to $LITE.

More than I care about little MC % returns that's happening currently.