Also known as simipanda. 3D Media Developer. Cryptocurrency and Stocks enthusiast. AI is the future, long TECH! I make my own indicators and trading tools🔨

@daniel_koss Been in crypto/btc since 2017, sold a bit late last year (+proxy stocks like MSTR, COIN) to ride the AI narrative. I think it's much much bigger than BTC/sound money and it made sense to rotate out as opportunity costs...

$LPK.DE / LPKF, SDAX 신규 편입 확정

LPKF가 독일 SDAX 지수에 새로 편입됨.

효력 발생일은 2026년 6월 22일.

SDAX는 쉽게 말하면 독일 증시의 소형주 대표 지수임.

독일 DAX가 대형주,

MDAX가 중형주,

SDAX가 그 아래 소형주를 대표하는 지수라고 보면 됨.

즉 LPKF가 독일 소형주 시장에서 공식적으로 더 눈에 띄는 위치로 올라간 것임.

중요한 점은 이 뉴스가 LIDE, TGV, glass substrate, advanced packaging 장비의 대형 양산 수주를 의미하는 것은 아니라는 점임.

기술 thesis가 직접 검증된 뉴스는 아님.

하지만 수급 측면에서는 긍정적임.

SDAX에 들어가면 지수를 추종하는 ETF, 벤치마크 펀드, 독일 기관투자자들의 관찰 대상에 들어갈 가능성이 커짐.

쉽게 말하면 회사가 갑자기 더 좋은 회사가 됐다는 뜻은 아니지만, 투자자들에게 더 잘 보이는 진열대에 올라간 것에 가까움.

그래서 이번 뉴스는 펀더멘털 호재라기보다는 수급·인지도 개선 이벤트로 보는 게 맞음.

정리하면,

펀더멘털 기준: 중립

수급 기준: 약한 긍정

인지도 기준: 긍정

장기 thesis 기준: 아직 핵심 검증은 아님

LPKF의 진짜 핵심은 여전히 SDAX 편입이 아니라 실제 주문임.

앞으로 봐야 할 것은 advanced packaging production system order, high-volume glass substrate / TGV / LIDE 채택, 고객명 공개, order intake 개선, margin recovery임.

SDAX 편입은 좋은 보조 재료지만, 장기 상승 논리는 결국 “지수 편입”이 아니라 “양산 주문”으로 증명돼야 함.

개인 기록 / 투자 조언 아님.

@TheFinanceCat@ParadisLabs But if glass hits market in 2028 earliest, means manufacturing tools $LPK provide needs to hit deliveries soon - in H2 2026 to 2027, for clients to set up their factories next year for the substrate ramp.

@softmaxedx Health is wealth, your portfolio value wont matter if you're bed ridden or in the grave. Healthy eating, exercise and mental well being is a perfect cocktail 🍹

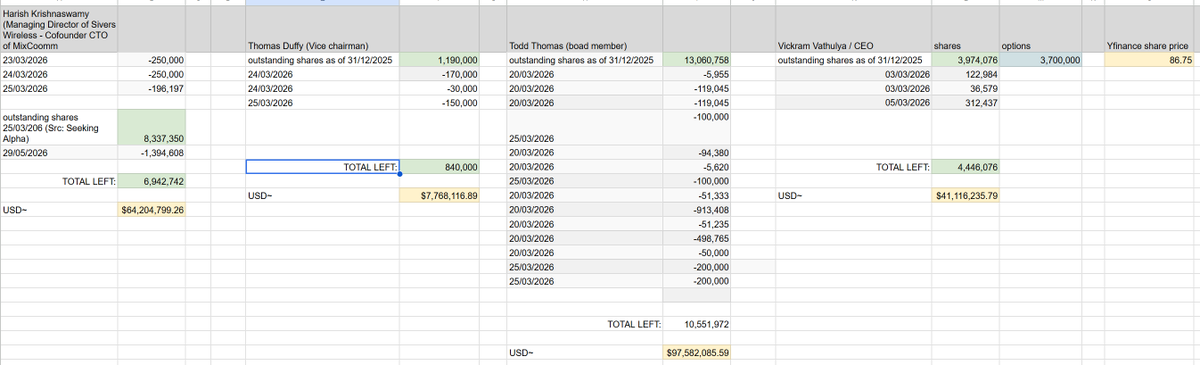

Seeing a lot of worry about $SIVE insider sells, so here's a sheet with what data I could find from official filings from 2026 and Annual Report latest board balance. Not worried, LITE, NBIS, AXTI, AAOI, SOI all have sellers last few weeks, I'm more interested in buys.

@aleabitoreddit Ive sold all my BTC/MSTR proxy related positions last year. I think AI stocks can run higher than BTC, what do you think Serenity, for smaller accounts is it still worth a re-entry or just keep focusing on CPO?

@KRLundgren@OberynJaksho@NingiResearch apologies if Im incorrect,I thought he had a few mill outstanding. Need a Google sheet to add all past sales.

https://t.co/ndFDYmL6Bq

@tiy23_@OberynJaksho@NingiResearch https://t.co/ClxsIoWTRB.sesorey

/Publiceringsklient/en-GB/Search/Search?SearchFunctionType=Insyn&Utgivare=Sivers%20Semiconductors%20AB

You can see the filings. I've not tracked the totals so apologies if Im incorrect,I thought he had a few mill outstanding. Need a

Google sheet

@OberynJaksho@NingiResearch No he still has tons more. Hes dumped shares before the big pop too and there was bad press back than about it also. Its all in the filings. No big deal, LITE execs also dumped tons recently, its just part of the game and we never know what personal reasons they have

An industry report from SEMI and Global Net Corp has been released, projecting Glass Substrate market to be $13B opportunity by 2040, at 67.2% CAGR. We are a bit too early for this sector rotation but its projected market is way bigger than current Pluggables, lasers and CPO

J'ai publié tout à l'heure l'analyse complète du Chips Act 2.0. J'ai essayé également de traduire les mesures réglementaires en un score.

L'objectif : identifier quelles sociétés cotées européennes ont le plus d'alpha face à ce nouveau cadre réglementaire.

Le score est construit sur 6 critères directement tirés du texte de loi et pondérés selon leur impact sur les flux de commandes :

A. Demand-side (25%) : exposition aux mécanismes de création de demande (Demand Forum, Grand Challenges, procurement public souverain). C'est le pivot central du Chips Act 2.0.

B. CADA / AI Gigafactories (20%) : capacité à fournir le hardware des datacenters souverains et des AIGF (200 Mds EUR d'investissements, triplement de la capacité datacenter EU).

C. FOAK / Strategic Project (20%) : éligibilité au statut First-Of-A-Kind élargi à toute la chaîne de valeur (permitting accéléré à 12 mois, guichet unique).

D. IPCEI AST (15%) : positionnement sur les technologies couvertes par le 3e IPCEI semi-conducteurs (AI chips, photonique, packaging avancé, EDA).

E. Region of Excellence (10%) : ancrage physique dans les clusters semi EU labellisés (Dresde, Grenoble, Eindhoven, Leuven, Catane, Villach).

F. Photonique / Quantum (10%) : exposition aux deux ajouts structurels du Chips Act 2.0 (PIC comme 6e composante, pont vers le Quantum Act).

Chaque société est notée de 0 à 3 sur chaque critère. Score pondéré sur 18 points maximum.

le Top 20 est en image

Ce qui en ressort : les large caps (ASML, Infineon, STM) scorent haut grâce à l'infrastructure et aux clusters. Mais l'alpha asymétrique est dans les small/mid caps exposées simultanément au demand-side ET au CADA. Le marché price déjà les premières. Pas encore les secondes.

Je vous invite à consulter l'article si le détail vous intéresse.

⚠️ Analyse basée sur des documents réglementaires publics. Aucune recommandation d'achat ou de vente. Vous êtes seul maître à bord de vos investissements.

@supertrotskiii@lkcttn there was an "analyst" upgrade for IQE price to 60p recently, small but some seem to be waking up to the narrative. Also Artisan Partners shares went from 10.60 to 13.10% hold now. (filed on RNS today from 2d ago, probs from dilution offering?)

$IQE has released their 2025 annual report. It's a long read, and I'm at work, but will digest this over coming days.

Read it here yourself and share any cool bits of info:

https://t.co/KF7OyKXsMJ

#epiwafers

@aleabitoreddit I worry about our kids futures, so Im doing everything I can to secure my family and their future family...anyone who sleeps through AI investment will feel it for generations to come. I keep telling people about this but often get dismissed that it's a bubble doomed to fail 🙃

$Ayar Labs joins $NVDA NVLink fusion ecosystem to integrate their CPOs into AI datacentres. I know we have known this link for a while but its official https://t.co/yFUYUblJbz

Hej Sven synd att du inte fårr svar. Skall försöka summera några saker som jag ser som helt nytt.

1. Sivers is being integrated directly into GF's SCALE platform. GF only introduced SCALE publicly about a month ago. Until now, GF had announced the platform itself, but not a laser partner embedded into that ecosystem. The release states that Sivers' laser arrays will be available in GF's SCALE™ (Silicon Photonics Co-packaged Advanced Light Engine) platform and reference designs. Being picked as GF reference design vs Lumentum/SmartPhontics is strong statement and validation of Sivers as Laser supplier into the AI ecosystem. That means Sivers is no longer just supplying components into the market generally; it is becoming part of GF's preferred silicon photonics architecture.

2. Expansion beyond CPO into LPO and broader optical connectivity like Pluggables with a large TAM that is closer to ramp (1.6T. Pluggables). Earlier Sivers announcements focused heavily on External Light Sources (ELS) for CPO deployments. This release explicitly says the collaboration supports: a) Co-Packaged Optics (CPO) b) Linear Pluggable Optics (LPO), c) Other emerging datacenter interconnect architectures. This broadens the addressable market materially beyond the ELS/CPO discussed previously.

3. The first full foundry-level endorsement of Sivers' laser technology. All other communications with GF had been in group of companies or partnerships with Ayar Labs, or Wireless. Now adding foundry-level endorsement to previous announcements, with system and module partners such as O-Net, Enablence and Jabil. This is different because GF is one of the world's leading silicon photonics foundries. Having GF publicly state that it is pairing Sivers laser arrays with its silicon photonics and SCALE platforms is a stronger ecosystem validation than a group of partners on list or module-level partnership.

4. A big signal that Sivers is positioning for hyperscaler qualification for Pluggables via GF like they done for Jabil. If GF succeeds in becoming one of the major SiPh platforms for 1.6T or 3.2T Pluggables, then Sivers potentially gains visibility to: NVIDIA ecosystem suppliers, Broadcom ecosystem suppliers, AMD ecosystem suppliers, hyperscaler custom-AI programs.