First two TEF-financed Texas gas plants have reached or are approaching commercial ops in ERCOT as of April. Calpine Pin Oak Creek (460 MW) got full commercial ops approval; NRG TH Wharton (456 MW) is sync'd.

~900 MW online, 5.8 GW in DD, while 6.7 GW has exited the program.

Took a look at BESS state-of-charge and how it related to prices for energy in ERCOT during Storm Fern.

Awesome to have this data now following Real-Time Co-Optimization!

While it's true that it is easier to build new generation in Texas, this oversimplifies what's actually happened.

Much of Texas produces capacity factors for both wind and solar generation that are well-above the normal for most of the country and go a long way to giving those projects a better chance of penciling.

And it's not as simple as just 'less red tape'. It's not necessarily about more or less permitting, it's about the cost of interconnection and the time it takes to determine that.

There are plenty of reliability studies new generators in ERCOT go through, they just aren't required to bear the brunt of transmission upgrades that the study process determines are necessary to accommodate the new projects.

That's the 'connect and manage' framework everyone talks about. The developer takes on the risk that if they develop in a location where their exported power causes tons of transmission congestion, they'll get curtailed and/or receive a low wholesale price.

It's not necessarily about less red tape, it's about faster studies that shift the risks/costs associated with development from the development stage to the operations stage.

And p.s., the numbers in the original chart are also a bit optimistic. Developers have been flocking to Texas in recent years, and it's true it has become the leader in utility-scale wind, solar, and storage in the US, but ERCOT's site itself shows that it hasn't been quite as fast as John's chart indicates.

Everyone who cares about climate should understand this. Texas, with no pro-climate policies, has blown passed California in clean energy. In large part because Texas has less red tape and makes it easier to build.

@PoW_Blockspace@edcporter Well, there isn't a fixed amount of curtailment happening at all times. Curtailment is variable as network topology changes and wind/solar gen increases and decreases. Scarcity pricing can occur on the same system as substantial amounts of curtailment. Just look at ERCOT in 2023

The general heuristic is that if rates are increasing due to *T&D charges* then it’s probably not data centers, and likely due to lack of load growth in general.

The problem is that going forward it’s very likely that data center load growth will put pressure on *energy prices* (especially if new generation isn’t sited to benefit all consumers).

Obviously consumers won’t know the technical difference in what causes future bill increases, so saying data centers aren’t at fault today (even though technically true), will look bad in retrospect

The biggest error in current wholesale power development is the pursuit of 100% islanded campuses (without any grid connection) to serve AI infrastructure growth

The second biggest error is the pursuit of co-located modular aeroderivative and RICE thermal generation as a speed to power solution instead of financing execution of grid-connected combine cycle frame turbines

Both of these existing behaviors leave the new load customers, and all other grid participants, worse off from a cost and reliability perspective compared to the optimal alternative

Both of these behaviors are a result of procedural inefficiency in our interconnection processes which have the potential to be addressed in 2026

By giving developers more decision-making and risk taking capacity in the interconnection process, solving speed to market can be complimentary to minimizing cost and maximizing reliability instead of being at odds - and thus more sustainable for the entire ecosystem

By correcting individual developer incentives, our wholesale grid can become more nimble, resilient and cost effective for all consumers as it expands rather than becoming increasingly frail from balkanization

Running analysis on reduced volatility in ERCOT and what could bring it back (hint: thermal retirements play a role).

The declining capacity factors for coal and CCs over the last couple of years - the result of lower ATC prices - are stark.

Clock's ticking for older coal gen.

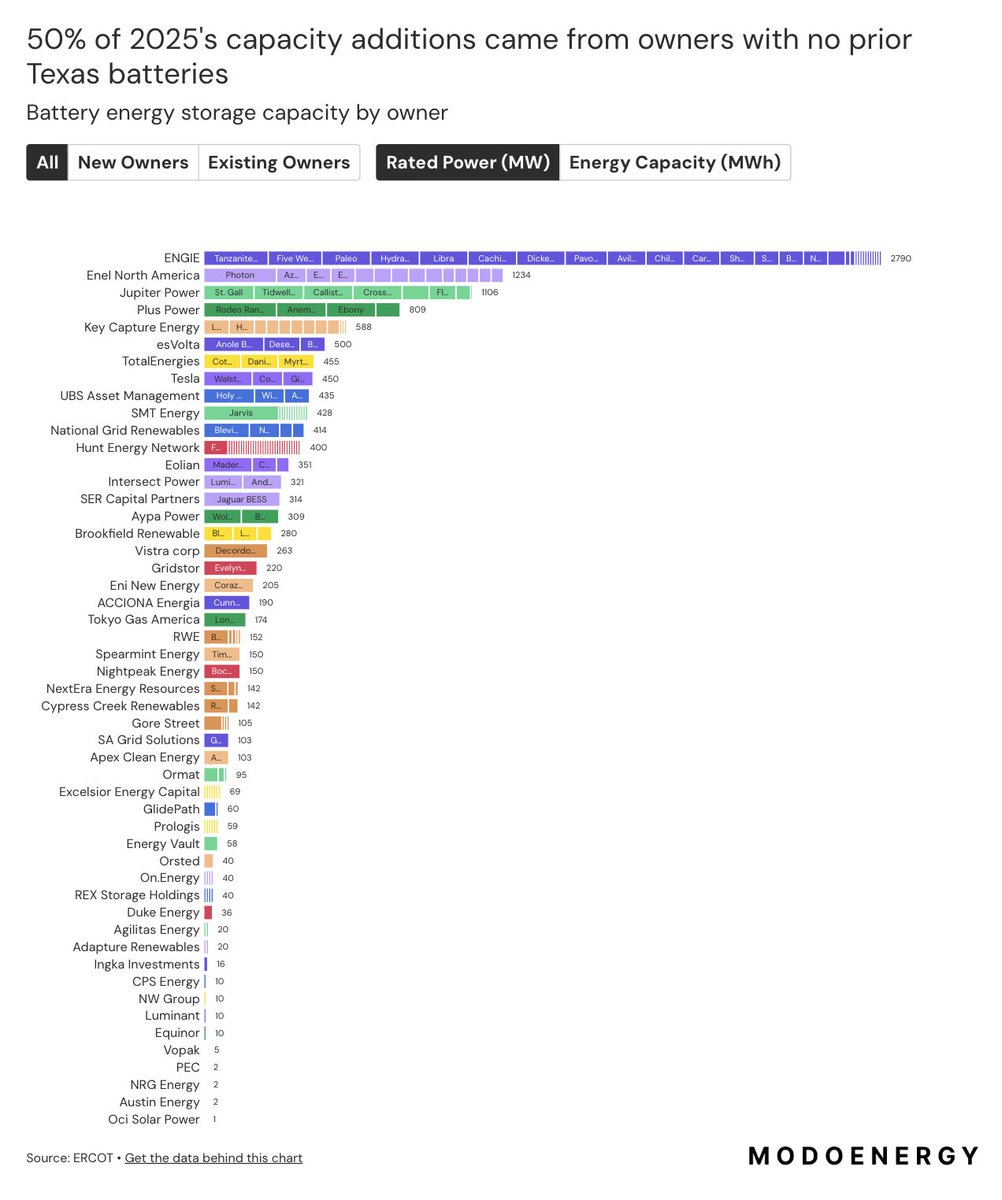

50% of the BESS capacity that began operating in ERCOT in 2025 was built by companies entering the Texas battery market for the first time

New entrants include:

esVolta: 500 MW

TotalEnergies: 455 MW

Intersect Power: 321 MW

SER Capital Partners: 314 MW

Brookfield Renewables: 280 MW

GridStor: 220 MW

Eni New Energy: 205 MW

Tokyo Gas America: 174 MW

...and more - totalling 3 GW

Download the data here:

https://t.co/ysBWLlZXju

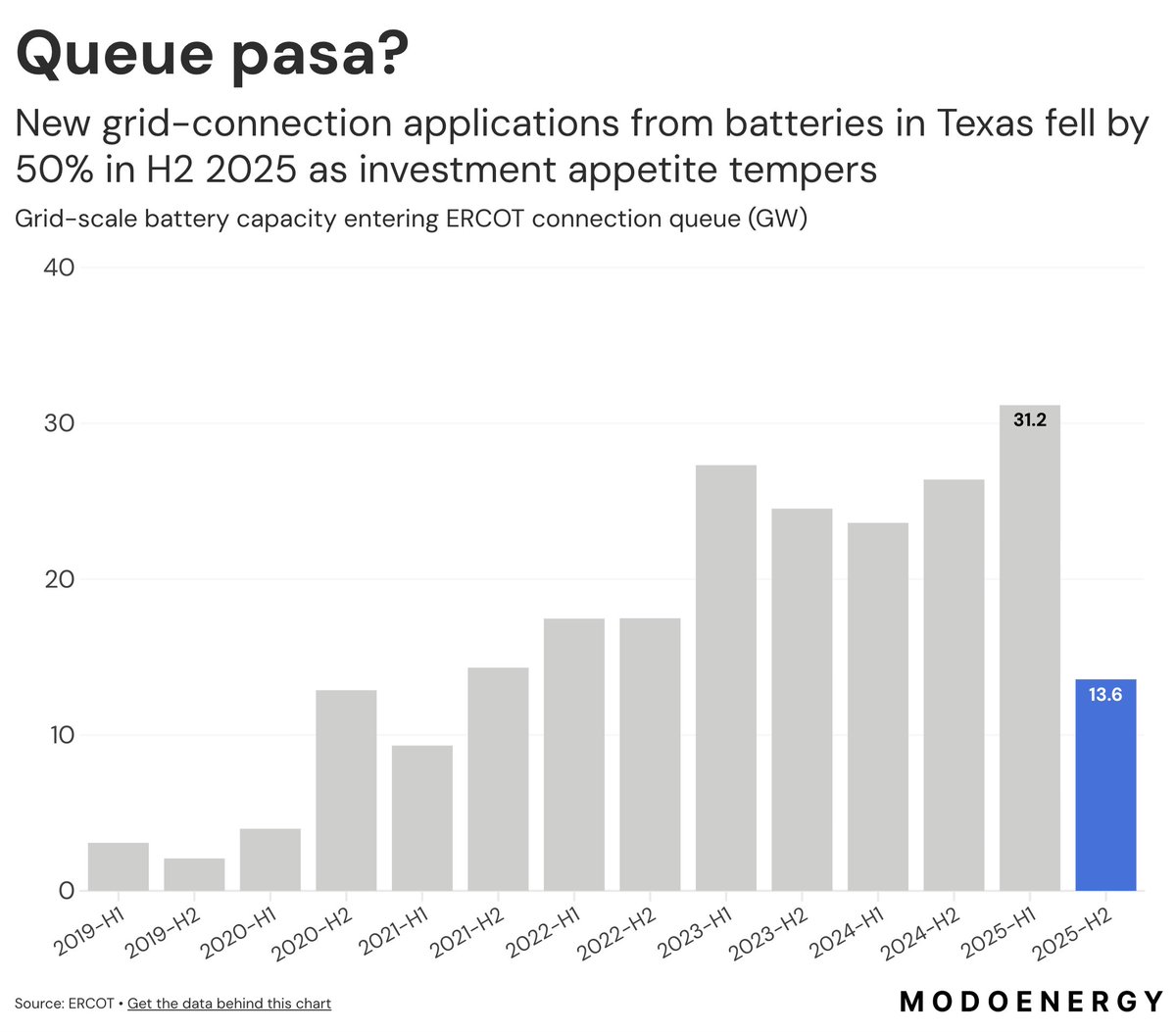

NEW DATA shows grid-connection applications for batteries in Texas fell to 13.6 GW in H2 2025 - a 50% drop compared to six months prior

We're likely seeing the upper-end of the S-curve for ERCOT's growth in battery capacity

Battery revenues saturated at $30/kW in 2025 after a mild weather year, leading developers to temper expectations

Now, if these projects are successful, they'll take four years to begin operating based on current queue progression rates

Investors backing projects today are betting on the 2030s, expecting...

1. large load growth

2. and generator retirements

...to boost revenues back towards the $100/kW range

The degree to which folks on this platform litigate their energy resource preferences by cherry-picking the grid mix in specific moments and places is a bit maddening. The power grid is a system, with various resources playing different roles at different times. Our job is to engineer a better system over time. That will take many resources doing different things at different times and places. This kind of thing doesn't help.

Definitely a lot to learn in the face of optimization during Winter Storm scarcity, especially taking RTC into account and managing the risk of taking on DA AS commitments.

Think we’ve seen this learning curve move pretty quickly in the past though as more batteries enter the market and as there are more events to learn from.

Emptying the clip on Monday AM is a big piece of what kept RT prices low. Many of them likely got paid via the DA prices.

That being said, there’s more that could have been done on Sunday evening, for instance, assuming their relative lack of participation wasn’t a collateral issue.

Long story short, most batteries basically just wanted to avoid two things: discharging early and missing the highest possible price peak (if a substantial peak occurred in RT), and not having enough charge to capitalize on the tightest hours of the weekend on Monday morning.

Saturday was a pretty low rev opportunity day relative to what BESS were anticipating Sunday and in particular, so I think they were trying to guarantee going into Sunday with high SoC.

On Sunday, it was an even more extreme version of that.

There would have been some operators who were just happy to collect the DART spread on whatever DA awards they had in Energy or AS since DA was generally well ahead of RT.

Some of that would also have been motivated by a fear of discharging into the Sunday evening peak, running out of SOC and seeing the price go through the roof and being unable to capture it.

The realization of that fear would have been made even worse if they were unable to charge back up for Monday morning because prices remained elevated overnight.

Being willing to charge at much-higher-than-usual prices unlocks more of a willingness to charge on days like these, I think.

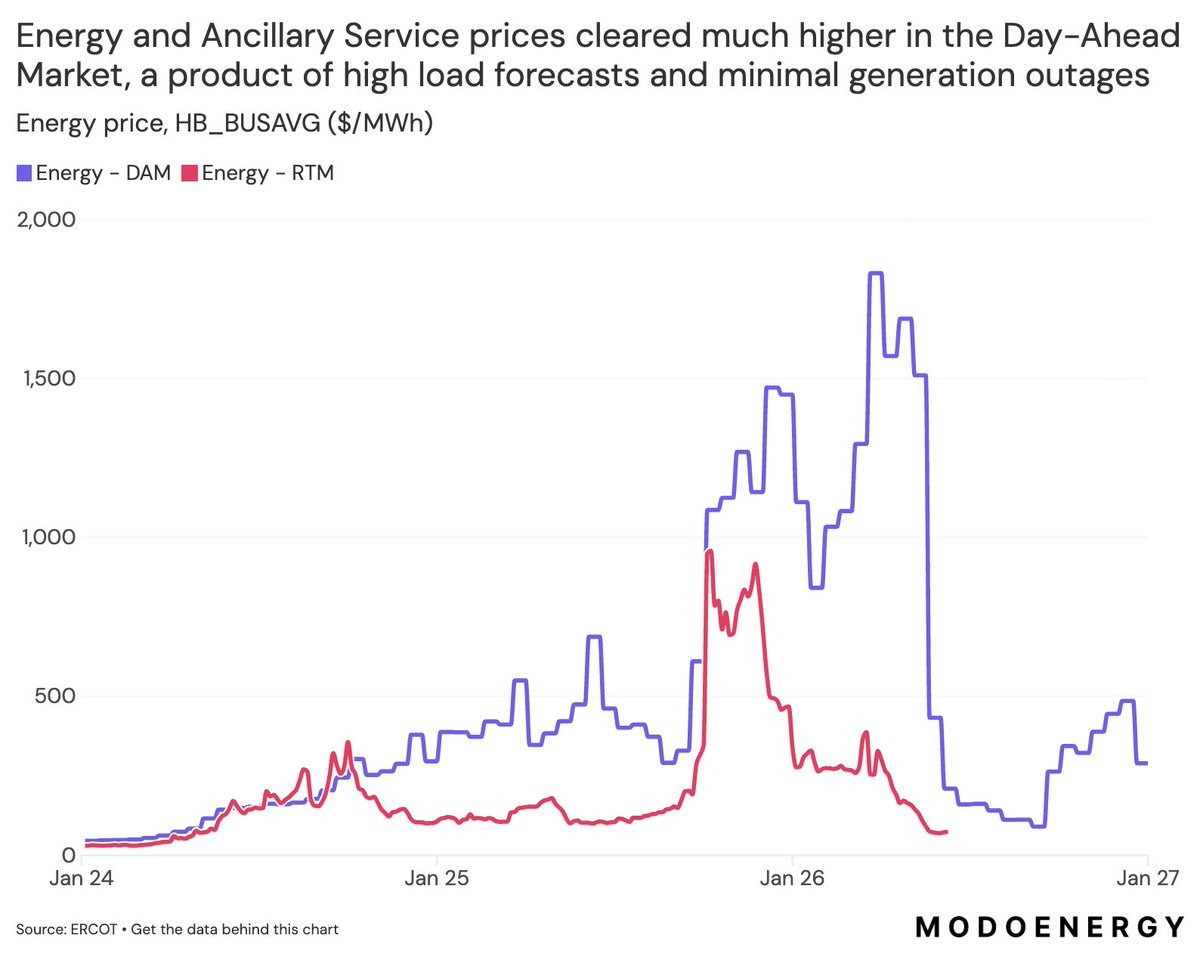

Day-Ahead prices exceeded Real-Time throughout the peak of Winter Storm Fern in ERCOT.

Why?

-Peak Load forecast: 86 GW. Actual: 75 GW.

-Thermal gen. outages <10 GW.

-Renewable production in line with ~8 GW expectations at peak.

The market priced in scarcity that didn't fully materialize, and the most sophisticated BESS operators would have reacted accordingly.

Here's what happened 🧵