Germany. May 1st saw day-ahead prices hit -€499.99/MWh at midday, then spike in the evening. A single battery captured its best 2026 return that day. This pattern will be normal by 2030 unless flexibility builds out substantially.

MISO's fast-track ERAS program selected 3.7 GW in Cycle 4. Natural gas takes 83% of capacity, up from 73% in Cycle 3. Battery storage fell from 27% to 6% as a single 230 MW project. The Cycle 3 storage surge looks like a procurement wave, not a structural shift.

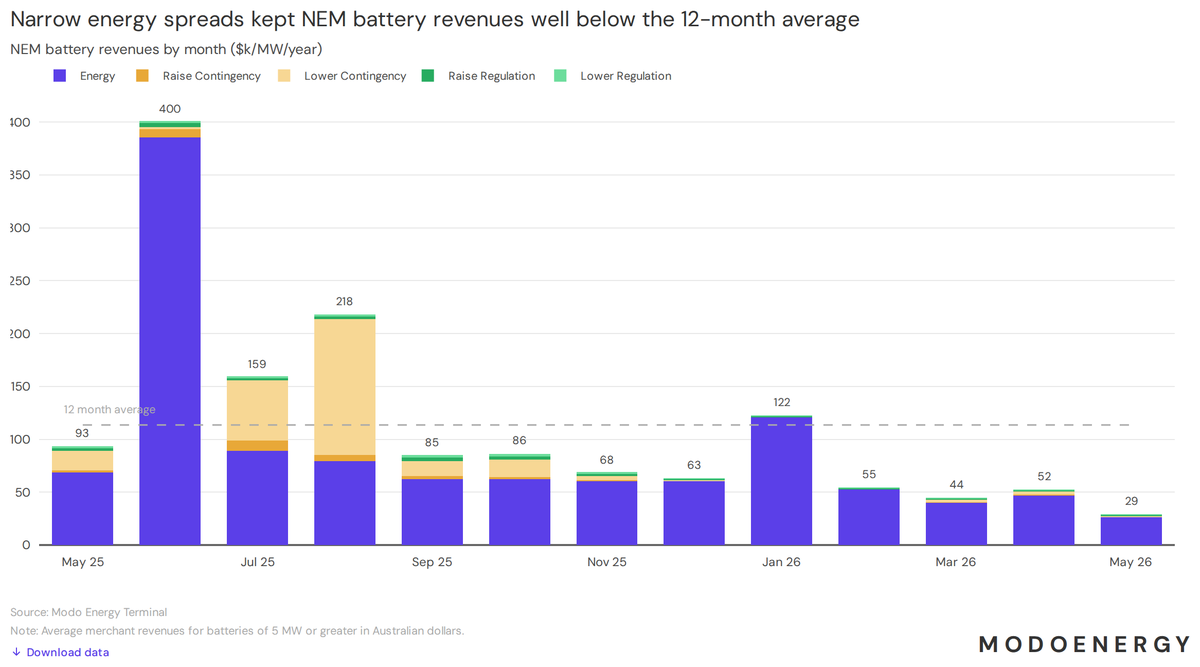

NEM battery revenues fell to $29k/MW/year in May 2026, the lowest since tracking began in 2022. Home battery additions now exceed grid-scale buildout, flattening midday prices and compressing arbitrage spreads across all mainland states.

SPP batteries earned $12.20/kW-month in May 2026, with Regulation providing 69% of revenues at $12.8/kW. The RTO values this service because wind dominance forces reliance on flexible gas, coal and hydro to balance. Ancillary Services remain unsaturated.

MISO coal emergency orders have cost consumers $400 million since March 2026, yet NERC's reliability assessment finds no operational issues ahead. The reserve margin clears without them. Replacement capacity in the queue already exceeds the preserved coal units.

🎧 Transmission: NESO expanded from running the grid to planning Britain's whole energy system across electricity, gas and hydrogen. They've cut the connections queue from 800 GW down to a deliverable pipeline.

https://t.co/Ok9aZNH3pN

South Australia FERM Tender 1: all six winners are battery projects totalling 517 MW / 4.1 GWh. No gas, no pumped hydro. Five developers, clustered around Adelaide and mid-north where network strength peaks. Neoen holds the largest footprint at 150 MW.

Battery returns track daily price spreads, not average price levels. ERCOT collapsed from $191k to $28k per MW-year, CAISO fell to $38k. Meanwhile GB, Germany, and Australia held steady or recovered. Same global energy transition, radically different battery economics by market.

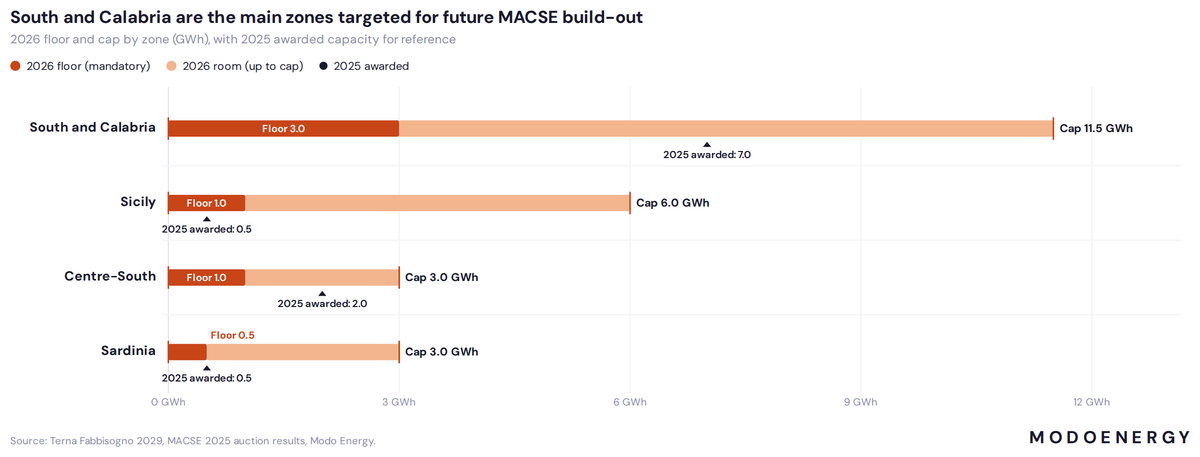

Italy's 2026 MACSE auction targets 16 GWh, up from 10 GWh in 2025. South and Calabria cleared its 7 GWh 2025 cap and gets 11.5 GWh next round. Sicily's mandatory floor doubles to 1 GWh. Auction format unchanged. Reserve premium still pending from ARERA.