Decided to gradually build back a position in $MCB.TO Tech/product leadership seems intact. Demand for its smarTR products pushed to the right. Q2 will be ugly but BS is strong and now there is better visibility for a Q3-Q4 recovery.

$PEW

Playing around with some logistics hypotheticals. More so an illustration to chew on.

Side note: the ~11mm of warrants have an $11.50 strike price. I just used basic shares. Matters more in these outlier cases.

Disclaimer: I own shares. NFA. DYODD.

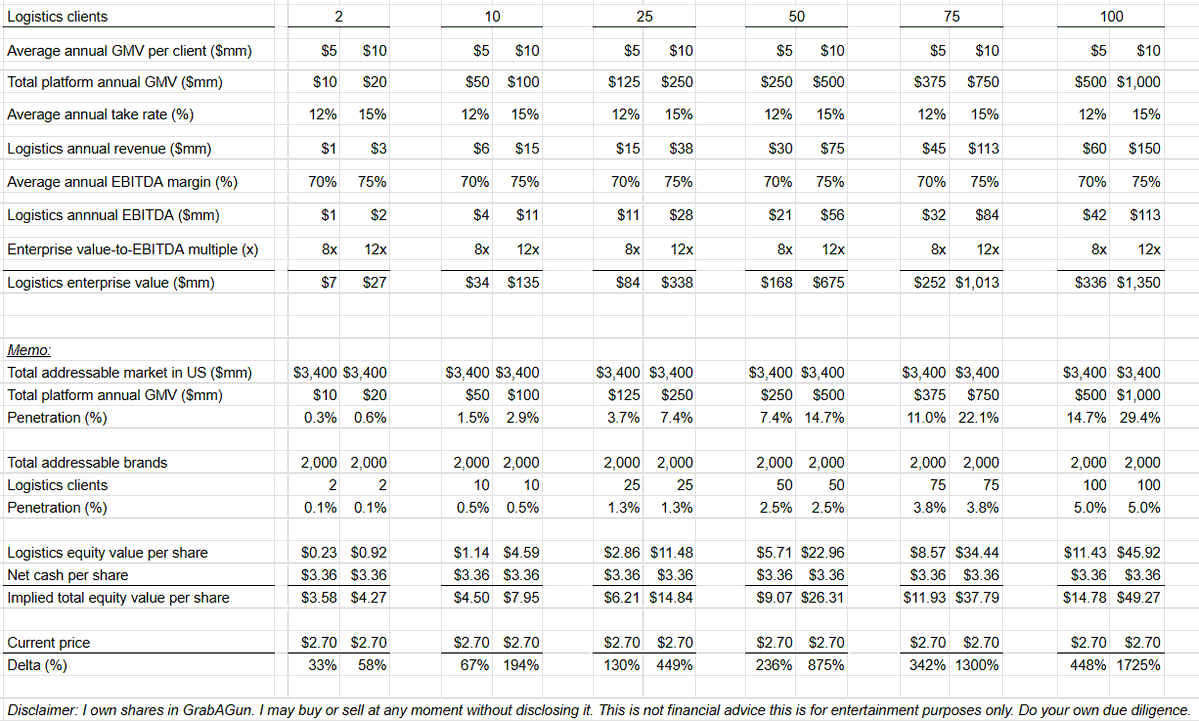

$PEW

Playing around with some logistics hypotheticals. More so an illustration to chew on.

Side note: the ~11mm of warrants have an $11.50 strike price. I just used basic shares. Matters more in these outlier cases.

Disclaimer: I own shares. NFA. DYODD.

My chain on AF’s incentives for $NMM future back in ‘22 aged well. She continues to buy & owns >20% (incl GP) & NAV is >$5 b. Tanker fleet now among youngest. Containers booked (great composition). Dry bulk spot now likely termed out since rates finally soaring. Last step: big NMM distributions to trade ~NAV. Stock CHEAPEST in shipping.

Started a small pos in $PEW following this pitch (highly recommended), hearing the Q1 conf call and doing some DD. I really liked the CEO's commentary about M&A. It seems there are many ways to win here with a very limited downside.

$PEW printed Q1 26 results:

_Revenue $26.0M (vs consensus $24.5M), +11% YoY, ahead of 2% industry growth

_Gross profit $2.8M, +23% YoY

_Adj. EBITDA -$2.0M (vs consensus -$2.4M)

_Adj. EPS -$0.06 (vs -$0.08)

_Bought back $2.4M of stock

Normal quarter but what gets very exciting is the commentary. I'd highly encourage listening to the call.

I want to highlight two big things.

1 - Massive optionality developing in the legalization of direct shipments of firearms to consumers' homes.

Quote from the Q1 26 call:

"The ATF has proposed new regulations that would allow certain firearm transfers to occur remotely, with federal background check requirements still met through secure identity verification. If finalized, lawful consumers could complete the full compliance process remotely. That includes direct to home firearm delivery within an approved framework.

This could be the most significant change to firearms retail distribution in decades. Importantly, the infrastructure required to operate in this environment is complex. As currently proposed, the new regulations require remote identity verification, meeting federal standards, seamless integration, advanced compliance systems, secure record keeping, and the operational ability to execute all of it accurately at scale. Grab a gun is uniquely positioned for this opportunity.

For more than 15 years, we have built the Digital Infrastructure and Compliance Foundation required to support highly regulated online firearm transactions. Few companies are positioned to adapt this quickly if the rules change, regardless of regulatory outcome."

This could both skyrocket the penetration of e-commerce platforms like GrabAGun, but also be a MASSIVE tailwind for PEW Logistics, since the main pushback would be that you still need the buy in of dealers to take delivery of weapons. If that's no longer the case, the odds of PEW Logistics being the back-end infrastructure of all the gun manufacturers going DTC go wayyy up.

2 - Solid commentary that gives me better comfort they won't blow the cash:

" We're not in the business of overpaying to hit arbitrary growth targets.

The strength of our balance sheet gives the luxury of patience. We can wait for the right assets at the right price, rather than chasing deals that don't make strategic or financial sense."

I want to remind people you're paying less than $0 for the business, and also that -$2M of EBITDA isnt actually cash burn, EBITDA excludes the large amount of interest they earn on their cash.

$PEW printed Q1 26 results:

_Revenue $26.0M (vs consensus $24.5M), +11% YoY, ahead of 2% industry growth

_Gross profit $2.8M, +23% YoY

_Adj. EBITDA -$2.0M (vs consensus -$2.4M)

_Adj. EPS -$0.06 (vs -$0.08)

_Bought back $2.4M of stock

Normal quarter but what gets very exciting is the commentary. I'd highly encourage listening to the call.

I want to highlight two big things.

1 - Massive optionality developing in the legalization of direct shipments of firearms to consumers' homes.

Quote from the Q1 26 call:

"The ATF has proposed new regulations that would allow certain firearm transfers to occur remotely, with federal background check requirements still met through secure identity verification. If finalized, lawful consumers could complete the full compliance process remotely. That includes direct to home firearm delivery within an approved framework.

This could be the most significant change to firearms retail distribution in decades. Importantly, the infrastructure required to operate in this environment is complex. As currently proposed, the new regulations require remote identity verification, meeting federal standards, seamless integration, advanced compliance systems, secure record keeping, and the operational ability to execute all of it accurately at scale. Grab a gun is uniquely positioned for this opportunity.

For more than 15 years, we have built the Digital Infrastructure and Compliance Foundation required to support highly regulated online firearm transactions. Few companies are positioned to adapt this quickly if the rules change, regardless of regulatory outcome."

This could both skyrocket the penetration of e-commerce platforms like GrabAGun, but also be a MASSIVE tailwind for PEW Logistics, since the main pushback would be that you still need the buy in of dealers to take delivery of weapons. If that's no longer the case, the odds of PEW Logistics being the back-end infrastructure of all the gun manufacturers going DTC go wayyy up.

2 - Solid commentary that gives me better comfort they won't blow the cash:

" We're not in the business of overpaying to hit arbitrary growth targets.

The strength of our balance sheet gives the luxury of patience. We can wait for the right assets at the right price, rather than chasing deals that don't make strategic or financial sense."

I want to remind people you're paying less than $0 for the business, and also that -$2M of EBITDA isnt actually cash burn, EBITDA excludes the large amount of interest they earn on their cash.

Agree on almost everything said here. I have a position myself. Very compelling but can't get off my mind we are over estimating mgmt capacity on this one. Q1 call exposed how bad mgmt comm is...plenty of ways to realize value, just not sure if they have the ability to execute.

(1/12) 🆕 investment thesis on a great opportunity I found in the Nordics. Long with a mid-sized position at Meridion. Let’s fly to Finland ⏩

Oriola $ORIOLA.HE is the leading provider of pharmaceutical distribution and wholesale services in Sweden and Finland. Market cap of ~€170M on the Helsinki stock exchange.

It operates in a regulated duopoly with >40% market share in both countries.

Out of this one. CMD was a shit show IMO. Oriola is extremely cheap but as said: I overstated mgmt ability to execute. Could be a M&A target tbh but Im keeping on the sidelines for now.

Agree on almost everything said here. I have a position myself. Very compelling but can't get off my mind we are over estimating mgmt capacity on this one. Q1 call exposed how bad mgmt comm is...plenty of ways to realize value, just not sure if they have the ability to execute.

@MorenoValue Y esto sin meternos en sin podrán cobrar los receivables del BS o no. Hay que ver como evoluciona la situación. Cuando el mgmt (que es excelente) han decidido poner medidas de precaución (cortar div y costes) para preservar cash...la cosa no pinta bien.

@MorenoValue El backlog son 25,8 MM CAD, en caso de que puedan convertirlo en revenue (cosa que dudo mucho), el crecimiento de ese revenue se verá afectado por el diferimiento de los rig allocations por parte de ADNOC y, más tarde, ARAMCO.

$CRON just impressive results with no contribution from CanAdelaar acq yet. Massive inflection in the P&L. Increased buyback pace and approved a new program 50 MM USD for this year.

Added to $CRON and $MRX yesterday with the sell off. Both companies are on track to have a very good 2026. Both cheap, especially Cronos. Lets see if the market wakes up about the CanAdelaar acq and the GrowCo expansion. Both drivers should impulse the P&L this year.

$CRON Pivotal morning for the equity story on these results. None of this is should be surprising but very few actually trade this for its fundamentals, so the market is going to have to catch up:

- 40% top line growth to $45m due to intl growth and the long telegraphed GrowCo expansion, on 42% gross margins;

- EBTIDA +122% to $5m; net income +100%.

- Buyback pace accelerated significantly to $17m in the quarter. Major earnings inflection accompanied by a shrinking of the equity.

- Share gains in major category, incl now #1 in vapes.

- EV ~$180m (1x sales) on a 40% revenue growth rate, inflecting profits, and a margin accretive acquisition coming online this summer that will more than double EBITDA.

Incredible.

@roojoo3 Price action doesn't make any sense...especially after hearing Ian Lowitt comments about April and Q2 performance. This would mean another Q with +35%/+40% YoY rev growth which is impressive considering prior year's Q2 included Liberation Day vol...