$BMNR holders aren’t pissed because the stock is red.

They’re pissed because this was sold as the ETH treasury rocket…

and somehow it turned into “please approve more shares.”

Stock is around $14.

Down ~55% from the year open.

Down ~58% from the year high.

Down 90%+ from the 52-week high.

That is not “normal volatility.”

That is a trust problem.

And the Tom Lee incentive stuff makes it even messier.

His package includes 500,000 PSUs if BMNR gets to 4% of ETH supply…

then another 1,000,000 PSUs if it gets to 5%.

So yeah, when shareholders watch the stock get smoked while the company keeps chasing “Alchemy of 5%,” people are going to ask the obvious question:

Is BMNR actually building value per share?

Or are common holders just the fuel for the 5% victory lap?

Because nobody hates the ETH stack.

That’s the crazy part.

The market likes the ETH.

It just doesn’t trust the wrapper.

Every bullish headline now comes with the same ugly thought in the back of people’s minds:

How many more shares?

How much more dilution?

Who is this really being built for?

Tom Lee can kill the bear case fast.

Show ETH per share.

Show accretion.

Show discipline.

Stop making holders feel like the ATM.

Until then, the angry village has a point.

Maybe $BMNR is an ETH weapon.

Maybe it’s just a compensation plan wearing an ETH hoodie.

$BMNR $ETH $BTC $MSTR $COIN $BMNU $BMNP $SBET

After too many hours of research/DD to count, these are my Top 5 AI Stocks in the Top 5 AI Sectors to Invest in:

1. Neoclouds: The GPU & Compute landlords. Whoever owns the compute owns what every AI company on the earth needs to grow & succeed.

$NBIS - Nebius. Spun out of Yandex, rebuilt as a pure-play AI cloud. Microsoft and Meta committed billions in contracted backlog. The fastest growing neocloud on the board. My favorite pick as a long-term investment.

$CRWV - CoreWeave. The American-founded neocloud. SemiAnalysis rated this Neocloud in a class of it's own, which can not be understated. Deals with Anthropic, OpenAI, Meta, Perplexity, Google, Microsoft... the list goes on forever.

$HUT - Hut 8. Started as a bitcoin miner, pivoted hard into AI hosting and power infrastructure. Owns the power, not just the GPUs. They're landing deals left and right, definitely an underappreciated sleeper pick.

$APLD - Applied Digital. Same playbook. Former crypto miner now building purpose-designed AI data center campuses with long-term hyperscaler leases.

$CIFR - data center host for Anthropic's directly, purchased Google TPU v7 Ironwoods (400K units, ~$10B), backed by a 10-year, $3B+ Fluidstack hosting deal where Google guarantees $1.4B of lease obligations for a 5.4% equity stake. One of the only neocloud-adjacent names with real exposure to Google's silicon instead of pure Nvidia GPU rental.

2. Optical / Photonics:

Because every GPU is useless if it can't talk to the GPU next to it.

$CRDO - Credo. The connectivity layer inside every AI cluster. Active electrical cables and DSPs that scale with every rack hyperscalers deploy.

$LITE - Lumentum. Legacy telecom optics company that's become a core 800G/1.6T transceiver supplier for the AI buildout.

$ALAB - Astera Labs. Connectivity chips that solve the bottleneck between GPUs, memory, and storage. Pure-play AI infrastructure with almost no legacy drag.

$COHR - Coherent. Lasers, optical components, and transceivers spanning the entire photonics stack from datacom to industrial.

$MRVL - Marvell. Custom silicon and photonic fabric for hyperscalers. The company quietly inside more AI racks than people realize.

3. Memory:

The most cyclical, most violently mispriced sector in semis. HBM demand changed the entire setup.

$DRAM - DRAM ETF. One ticker, every important memory company on the planet, including South Korean companies like SK Hynix and Samsung Electronic, companies you CAN'T INVEST IN with most brokerages.

$SNDK - SanDisk. Spun off from Western Digital, now a pure-play NAND flash story riding the same supply tightness as everyone else in this sector.

$MU - Micron. One of three companies on Earth that makes HBM. The clearest direct line from AI buildout to memory revenue.

$WDC - Western Digital. Hard drive and enterprise storage demand riding the same data center capex wave as everything else on this list.

$STX - Seagate. The other half of the storage duopoly. Enterprise nearline drives are seeing the same supply crunch dynamics as memory.

4. Analog / Power Semis:

Unsexy. Necessary. Every data center, every EV, every robot needs power management silicon that doesn't get the AI premium yet:

$MXL - MaxLinear. Smaller-cap analog and mixed-signal play with infrastructure and data center exposure that's still flying under the radar.

$STM - STMicroelectronics. European chip giant spanning auto, industrial, and power semis. Way out of favor relative to its diversification.

$ON - ON Semiconductor. Power semis for EVs and industrial, now leaning harder into data center power delivery as a growth vector.

$VSH - Vishay. Passive components: resistors, capacitors, diodes. Boring until you realize literally everything electronic needs them.

$POWI - Power Integrations. High-voltage power conversion chips. Small cap, niche, and positioned for the power efficiency problem AI data centers haven't solved yet.

5. Physical AI / Robotics:

It's coming, soon, and the market is beginning to realize it.

$OUST - Ouster. Lidar for robotics, industrial, and autonomy. Consolidated the space after merging with Velodyne, now the survivor.

$VICR - Vicor. High-density power modules for robotics, AI servers, and defense. Power delivery at the component level, not the rack level.

$VPG - Vishay Precision Group. Precision sensors and strain gauges. The torque and force-sensing hardware that gives robots a sense of touch.

$AEVA - Aeva. 4D lidar with built-in velocity sensing. Smaller and earlier stage than the rest of this list, highest risk, highest ceiling.

$AMBA - Ambarella. Edge AI vision chips. Powers the cameras and perception systems inside cars, robots, and security infrastructure.

I believe a portfolio with these 25 names will severely outperform the market over the next few years. I have 7 figures throughout many of these names. These are all names I'm currently invested in, or plan on investing in in the near future.

None of this is financial advice.

1. Full Wall Street–Style Stock Analysis

Act like a senior Wall Street equity research analyst.

Analyze the stock: [TICKER].

Include:

• Business model and revenue streams

• Competitive advantages (moat)

• Industry trends

• Financial health (revenue growth, margins, debt)

• Key risks

• Valuation vs competitors

• Bull, bear, and base case scenarios

• 12–24 month outlook

Explain in simple terms but with professional insights.

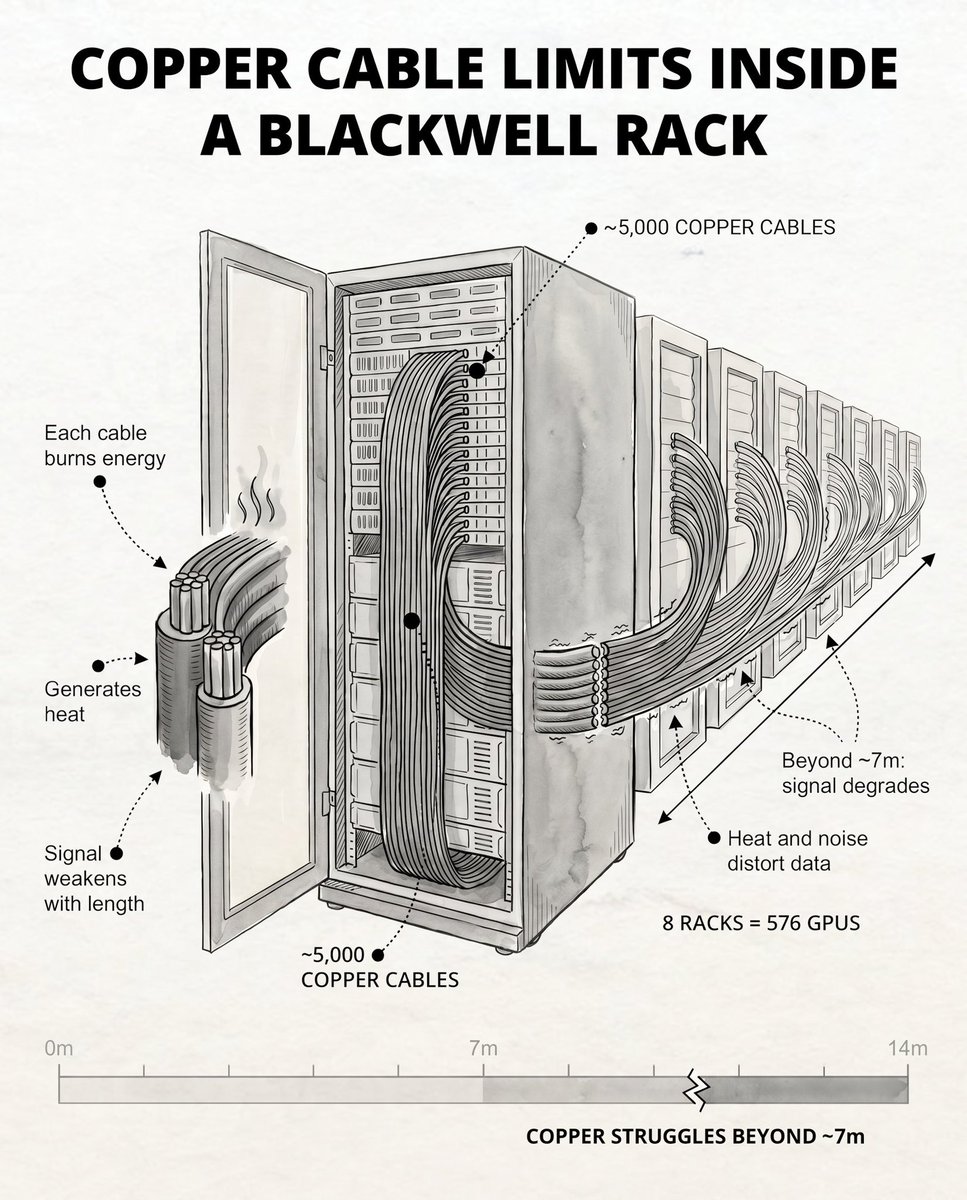

I received a lot of positive feedback on my photonics deep dive.

Here’s another visual from the article, illustrating a Blackwell GPU rack. Once copper reaches its limits, photonics take over.

Estimated 2030 TAM:

• Copper based: $8B → $34B

• Optics based: $3B → $120B

There is one stock that everyone needs to buy.

That is $SPCX on any substantial market pullback.

Buy at $150

Buy more at $100

& finally buy even more at $80

SpaceX will be a $800-$1,000 stock within 2-3 years.

Looking back, many will regret missing this obvious opportunity…

My Top 5 Interconnect stocks ranked:

1. $CRDO (Credo Technology)

The AEC copper pure-play with the best growth rate in the group, 274% YoY revenue growth last quarter. Hyperscalers are choosing copper wherever physics allows, and Credo owns that socket. But they’re not standing still: DustPhotonics ($750M) gives them silicon photonics, Hyperlume gives them microLED, and the optical DSP portfolio (Bluebird, Cardinal) is doubling revenue annually. Credo is building a full-stack interconnect company across all distance tiers. Smaller and higher-growth than Marvell.

2. $AAOI (Applied Optoelectronics)

A transceiver company riding the current 800G/1.6T wave, and riding it well. The capacity story is the bull case: AAOI is building toward 500,000 units/month of combined 800G and 1.6T transceivers by year-end. Raymond James models annualized EPS of $11-12 at that capacity level. The geopolitical angle is underappreciated, AAOI is positioning as the largest U.S.-based producer of AI-focused transceivers. The bear case: they don’t have a visible path into the CPO, microLED, or silicon photonics architectures that will define the next era, but their execution on the present cycle earns them a spot.

3. $MRVL (Marvell)

The most diversified interconnect play in the market. Optical DSP leader (70% interconnect revenue growth this year), CPO scale-up via the $5.5B Celestial AI acquisition (targeting $1B run rate by end of 2028 with Amazon Trainium 4), microLED through the Mojo Vision partnership, and copper connectivity for NVLink Fusion. Jensen Huang called it the next trillion-dollar company. The risk is valuation, 96x trailing P/E prices in a lot of execution.

4. Lumentum ($LITE)

The structural chokepoint. Only supplier shipping 200G-per-lane EMLs at volume, the component everyone needs for 1.6T transceivers. CPO is actually bullish for Lumentum because CPO switches still need external laser sources, and Lumentum just booked its largest CPO laser order ever (hundreds of millions, H1 2027 delivery). NVIDIA has pre-allocated laser capacity so aggressively that lead times stretch past 2027. The risk is concentration — Lumentum is a laser company, and if a competitor qualifies a second source at 200G, pricing power erodes.

5. $TSEM (Tower Semiconductor)

The picks-and-shovels play. Tower is the leading silicon photonics foundry, SiPh revenue grew 70% YoY, with $650M invested to triple capacity by mid-2026. Every CPO optical engine, every silicon photonics transceiver, and most photonic integrated circuits need a foundry, and Tower is where the industry is building. Less sexy than the chip designers, but foundries tend to win regardless of which architecture or end customer dominates. Lower volatility, lower ceiling, but the most technology-agnostic bet on the interconnect buildout.

Honorable mentions:

$ALAB (Astera Labs) would rank if it weren’t trading at a steeper premium with a narrower product focus (PCIe/CXL retimers and fabric switches). Worth watching if valuation pulls back.

$COHR (Coherent Corp) NVIDIA’s named silicon photonics collaborator for Spectrum-X. Coherent plays both sides, laser sources (where CPO is bullish) and transceivers (where CPO is bearish). The bear case is a messy transition where transceiver revenue drops before CPO revenue fills the gap.

Just as a recap, these were all my core European longs:

1. $SIVE

2. $LPK

3. $SOI

4. $RPI

5. $IQE

6. $ALRIB

7. $XFAB

Sivers: As you know by now, core laser chokepoint over next generation photonics, from 1.6T pluggables to CPO.

Embedded in many hyperscaler suppliers from Jabil to Ayar. Should go brrr 2027 but markets are forward looking, so ramps + qualifications should get priced in now.

LPK Laser - Glass core substrate "monopoly" with LIDE.

"More than 80% of major global players have selected our equipment for process validation, learning and scaling to mass production"

Soitec - Silicon photonics SoI substrate pure monopoly while coming out of legacy drag segments.

Raspberry Pi - Was my fun idea around Raspberry Pis being used for AI hardware deployments.

Previously this thing was mainly educational or hobby boards, but now used for edge/local AI. Just thought revenue increase would be extremely material and it played out well.

IQE - Critical epiwafer player for your Western photonics like Macom, Tower, Lumentum, and others.

Was kinda going under, but thought their latent capacity relative to Landmark was undervalued.

Also given how important it was, I thought that your downstream players + Govs wouldn't let it go under, so it was more of a moonshot idea earlier in the year.

Lot more derisked now, very important.

Riber - Kinda monopoly in the MBE space, exposure to Quantum / quantum dot + silicon photonics.

Found out from OSINT help from a friend latentvalue that Microsoft Quantum was buying their machines, so this was direct hyperscaler validation + kinda de-risked at current MCs.

XFab - SiC foundry backed by EU/US CHIPS Act with power semi upside. (152% Y/Y growth for their sic vertical).

Main growth was their silicon photonics foundry past 2027 that's getting evaled by nvidia. And that they're leading Europe's value chain efforts in photonics, kinda like an early tower semi.

We'll see how this plays out, thought power semi exposure + low P/B would derisk the company until they scale their photbunchonics efforts.

From my own personal thoughts:

Out of the maybe $SOI has already been re-rated the most? But I'm holding anyway.

$LPK and $ALRIB I think are still undervalued despite their monopolies.

$RPI is just kinda seeing how things go at this point, would be hilarious if they ended up like a mini nvidia for low end edge ai.

$IQE probably has a long way to go given new tower long term agreement, alongside macom. And if they convert latent capacity, I still think it has a chance of rerating like landmark.

$XFAB idk if im missing something or are markets missing something. you have nvidia as a direct eval of their silicon photonics foundry, and it's trading below replacement P/B. i think im right though.

$SIVE I see has the highest upside out of all of them given laser company ability to vertically integrate, acquire companies downstream to make their lasers more valuable, etc. Just like coherent/lumentum.

There's like 1-2 more random ones that aren't really material, but just in general.

These are the ones I've liked the most.

🇪🇺 EU TO DELIST TETHER'S $175B USDT FROM EXCHANGES

Binance, Coinbase, Kraken, and Crypto .com have removed $USDT for EU users after Tether chose not to comply with MiCA rules.

Meanwhile, $USDC has secured MiCA approval, making it the leading compliant stablecoin in the EU ahead of the July 1 deadline.

#Ethereum CME futures show that it's been heavily accumulated between $1500 and $2500, and it has a huge monthly CME gap above that won't fill until $2700.

For years, the issue with #Ethereum is that the majority of it is held by retail, and that institutions haven't had a chance to get their hands on it.

What's the best way to accumulate #Ethereum from retail besides having it chop sideways in a brutal range for 5 years and making even the biggest and loudest #Ethereum bulls capitulate?

I am not advocating you to reallocate assets you own that has momentum and sell all of your $MU $MRVL or $AMD for #Ethereum, because I don't know when #Ethereum will start running up and I don't think that the currently-hot momentum plays will exhaust their bull trend anytime soon.

But I do think there's a role of #Ethereum and related assets in the portfolio if you don't want to chase momentum, don't mind "opportunity costs", want the time to accumulate underappreciated assets that institutions are buying, don't mind the short term volatility, and are willing to see how things play out over the next 2 years.

THIS STILL LOOKS INSANE.

$ETH now has 12x more liquidity sitting to the upside than downside.

It seems like MMs and cartels are aiming for peak capitulation for Ethereum here.

🚨Everyone is still buying the chips. The bottleneck already moved.

A GPU that computes in nanoseconds and waits microseconds for data is a stranded asset. At 1.6T speeds, copper runs out of physics. The constraint on AI is no longer how fast you can think. It's how fast you can move what you thought.

Jensen has now said it twice in three months.

At GTC in March: "Is copper going to still be important? The answer is yes... Are you going to scale up optical? Yes. Are you going to scale out optical? Yes... We need a lot more capacity for copper. We need a lot more capacity for optics. We need a lot more capacity for CPO."

Last week at Computex, on Marvell's stage: "Optics where you must, copper where you can." Then he called Marvell the next trillion-dollar company and the optical complex repriced within days. The same keynote put a date on the handoff: 200G per lane is the last generation where copper is sufficient. After that, optics takes the rack.

Translation: not copper OR light. Copper now, light next, unprecedented amounts of both. 🔥

The chain is unavoidable: AI tokens are profitable → more GPUs → more bandwidth → copper hits its wall → photonics becomes the chokepoint.

And the smart money stopped debating. Follow the closed deals:

→ $NVDA has committed at least $6.5B to photonics in three months: $2B into Lumentum, $2B into Coherent, a $500M stake in Corning, and a piece of Ayar Labs' $500M round. Direct investments to secure its own light supply.

→ $MRVL paid $3.25B for Celestial AI, up to $5.5B with milestones, to build what its CEO calls a silicon photonics powerhouse.

→ $CRDO closed DustPhotonics two weeks ago. Ciena bought CPO startup Nubis for $270M.

North of $10B of strategic capital locked up one supply chain in under a year. Capital like that doesn't chase a theme. It secures a bottleneck.

LAYER 1: WAFER. Every laser starts as a crystal.

🟠 $AXTI: the InP substrate leader. The first chokepoint in the stack.

🟡 $IQE: compound-semi epiwafers feeding the laser makers. Speculative, but structurally upstream.

LAYER 2: LIGHT. Photons don't make themselves.

🟠 $LITE: revenue +90% YoY last quarter to $808M. EML shipments doubled and management says demand still exceeds supply across EMLs, pump lasers, and transceivers. NVIDIA just wired them $2B. OCS backlog past $400M plus a multi-hundred-million CPO order for 2027.

🟢 $SIVEF (Stockholm: SIVE): the external light source. CPO does not emit its own light. Every optical engine needs a continuous-wave InP laser feeding it, and that is the layer you cannot engineer around. ELS modules with POET hit production readiness end of this year. Disclosure: long.

🟣 $POET: the optical engine wildcard. Its Optical Interposer pairs with Sivers' lasers on external light sources for CPO, with a LITEON module deal stacked on top. Binary commercialization, real architecture.

LAYER 3: OPTICS AND MODULES. Where light meets the rack.

🟠 $COHR: the volume anchor in transceivers, holding NVIDIA's other $2B check.

🔵 $AAOI: Q1 revenue +51% to a record $151M, datacenter revenue more than doubled, $124M of 800G orders plus a $200M+ 1.6T order in hand. Scaling Texas capacity toward 500K+ units a month by year-end, targeting $1B+ revenue this year. Domestic supply while everyone fights over offshore. Disclosure: long.

🟠 $FN: the foundry of optics. When Fabrinet is building, the orders already exist.

THE INTERCONNECT: the layer the rack cannot route around.

🔵 $CRDO: just closed DustPhotonics. SerDes → DSP → silicon photonics → system integration, one company, 800G through 3.2T. Electrical AND optical, end to end. FY26 revenue tripled to $1.34B at 68% gross margin. The toll booth on both roads. Disclosure: long.

🟠 $MRVL: $3.25B for Celestial AI, and Jensen's trillion-dollar nod on the Computex stage.

🟠 $AVGO: switch silicon, optical DSPs, CPO engines. They define the socket.

🟠 $ANET: the AI spine. 100K-GPU clusters get stitched together in light.

LAYER 4: PACKAGING, FIBER, FOUNDRY. Where photons get industrialized.

🔵 $TSEM: the neutral silicon photonics foundry. Prints wafers for whoever wins.

🟣 $LPKF: glass-substrate packaging for glass-based CPO. Real technology, binary commercialization.

🟠 $GLW: AI racks demand several times the fiber density of legacy cloud, and NVIDIA just took a $500M stake. Corning sells density.

LAYER 5: TEST AND THE ANALOG UNDERLAYER. Complexity is a tax paid in validation.

🔵 $AEHR: silicon photonics test, ramping with the cycle. '

🔵 $VIAV: every 800G and 1.6T transceiver gets validated before it ships. The gate the market prices like an accessory.

🔵 $SMTC: the drivers and TIAs that fire the lasers. Sits directly under the LPO trade.

🔵 $MTSI: the high-speed analog behind 1.6T engines.

🟠 $CIEN: transport. Even long-haul is buying light.

💡The counter-thesis, because every map needs one. The honest debate on this stack is whether these are genuine bottleneck assets or cyclical optics suppliers enjoying peak demand at peak multiples. Lumentum's May print showed +90% growth with the stock up roughly 1,400% over the prior year at a triple-digit trailing multiple. That is a price for perfection. Most of these names live or die on a handful of hyperscaler capex lines, and one digestion quarter hits the whole stack at once. CPO timing has already slipped once. Architecture risk is real: LPO, CPO, and stretched copper are still fighting for the same sockets. The cycle is real. So is the gravity. 🔥

But the bears have to explain one thing: $NVDA, $MRVL, $CRDO, and $CIEN just spent over $10B securing this supply chain with their own balance sheets. The people with the best information are paying up for the layers.

The market owns the top of this stack. The asymmetry is at the edges: wafer, light, packaging, test.

Own the layers, not the logo.

Bookmark this for the weekend. Then tag the one investor you know who's still all compute and no interconnect. 👀

Ethereum is getting harder to buy.

Exchange reserves have dropped to their lowest level ever, while ETFs and long-term holders continue pulling ETH off the market. A major supply shift is happening behind the scenes.

➜ ETH on exchanges has fallen to just 14.5M ETH, an all-time low

➜ Over 6M ETH has been withdrawn from exchanges since late 2023

➜ Spot ETH ETFs are steadily accumulating supply

➜ Corporate treasuries are beginning to add ETH exposure

➜ More ETH is being moved into staking and long-term storage

➜ Less liquid supply can amplify price moves when demand increases

The biggest rallies often begin when supply dries up before the crowd notices.

Ethereum's supply is shrinking. The next question is whether demand is about to catch up.