'The reliance of high valuation multiples on expanding profit margins is probably one of the most underappreciated risks in the market right now.' https://t.co/KUeEq73Oxi by @billhester

@mjmauboussin quotes about 20 research papers every podcast. But, amazingly, no matter how many shows I listen to with him as a guest, it's almost always a different set of 20 papers. This conversation is a good review of his work...

"The bottom line I always say to my students, you’re a business person, so forget about formulas. ... Whatever the cost of capital you come up with should make business sense. And of course you want to have it tied to principles and finance"

@mjmauboussin on the cost of capital

ICYMI: New white paper, Strategic Allocation. Excited about the new methods presented here. Jointly evaluates stock valuations and bond yields, adds market internals for risk-management (critical in recent years). Just in time, given the bubble in passive.

https://t.co/fNf2QWtKgt

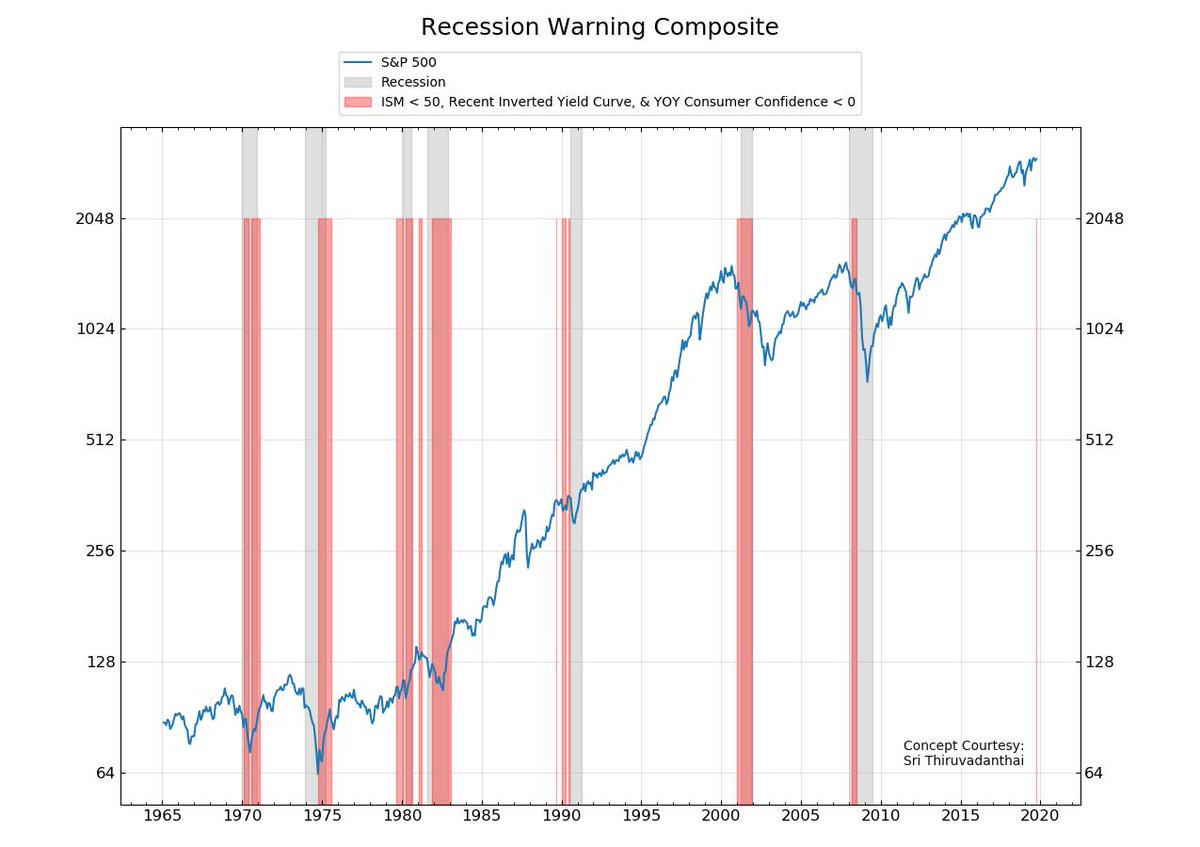

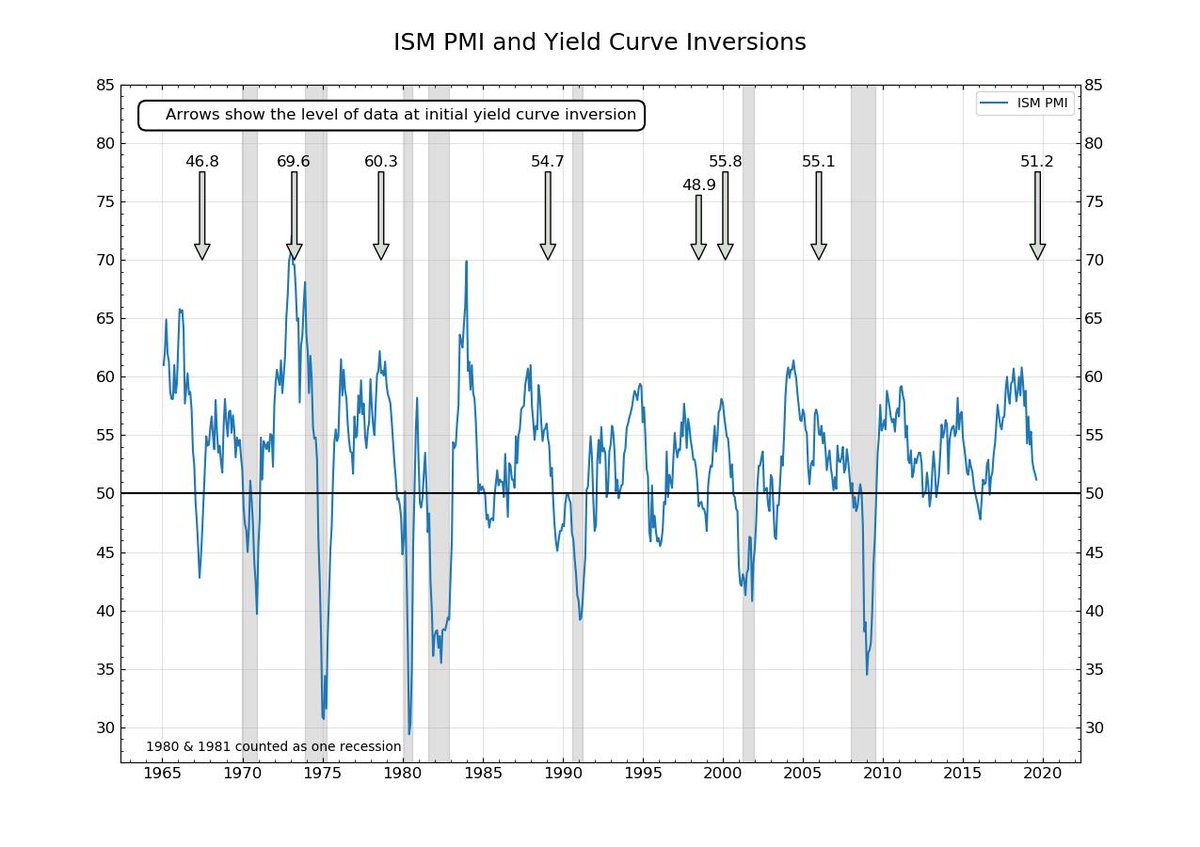

After the last few weeks it's hard not to think of 2000. Overvalued market, yield curve inverts in Feb, market tops in March, multiple attempts at overhead resistance, two breaks of that resistance, and slow data but not yet 'recessionary'.

Marty Zweig had a temporary employment series that reached back to the 1970's. If his series dropped 2% YOY it signaled recession. It worked in 2001 and 2008. It's one of the first numbers I look at on jobs day. For his recession model, see: https://t.co/NJzdnDfX5e

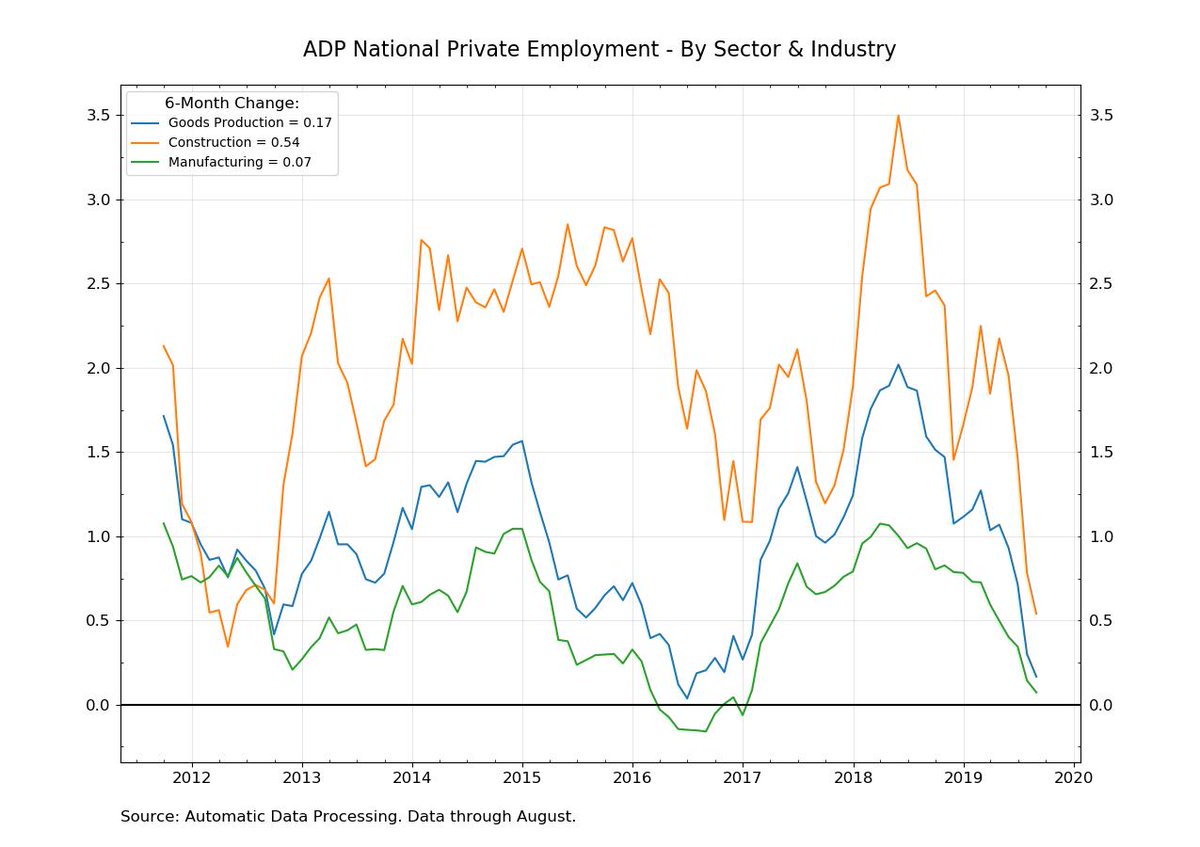

Will be interesting to see if manufacturing jobs come in positive tomorrow as expected. Here are the changes in the August regional Fed surveys on employment. Philly:-26, Dallas:-10, Richmond:-3, KC:-1. Empire up, but it was down 22 over the prior 3 months.

None of this data suggests that the economy is in recession, or that we will not be able to avoid one. But it does suggest that if the economy goes into recession, bond traders will have been late in inverting the curve.

A problem with the advice that there is no need to panic until 18 months after a yield curve inversion is that the US economy has much less momentum this time around.