If I’m a smaller miner like $SLNH $BDGE looking to convert my existing capacity to HPC Cerebras feels like a company you have to be targeting aggressively. $DGXX and $WYFI already on board and are in a strong position to be able to have Cerebras take incremental capacity.

1/ Some Simple Economics of AGI—🔥🧵

Right now, there is a low-grade panic running through the economy. Everyone is asking the same anxious question: what exactly is AI going to automate, and what will be left for us?

People don’t understand. There isn’t enough high quality infrastructure to run the Blackwells now. The largest companies have chips in warehouses because there is nowhere to plug them in. Launching Vera Rubin makes the infra shortage worse. AI data centers are wildly undervalued.

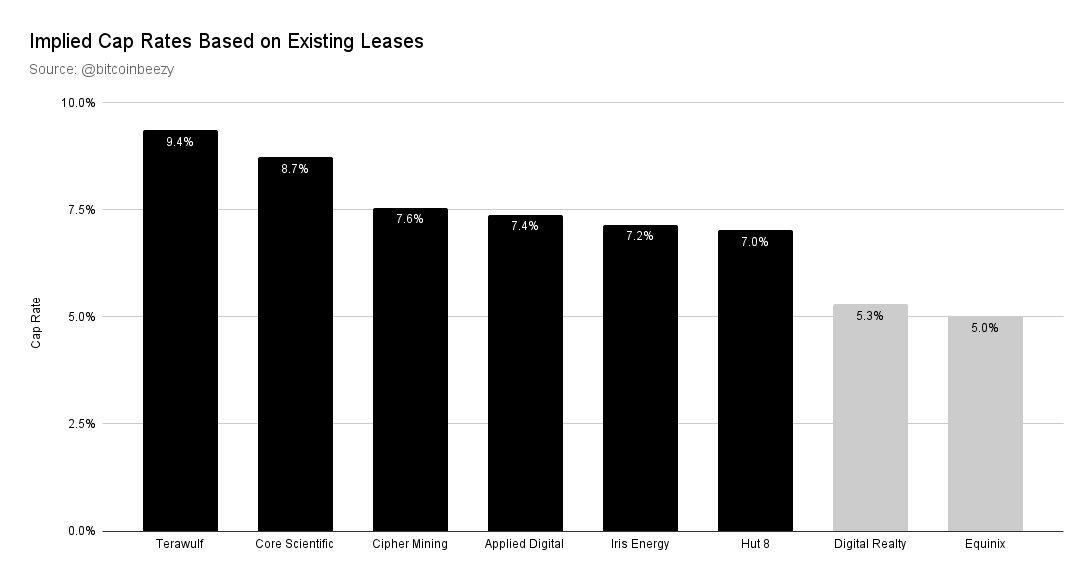

Bullish for $CORZ since they have single tenant risk currently with $CRWV. Core Scientific is currently trading at just under a 9% implied cap rate on its existing leases with Coreweave.

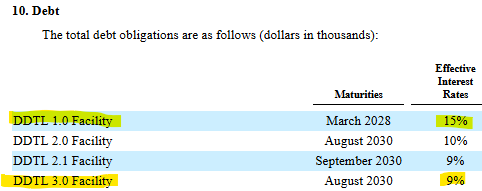

CoreWeave's $CRWV Delayed Draw Term Loan ("DDTL") facilities say much more about $CRWV's credit profile than any movement in the illiquid credit default swaps (CDS) tied to their debt.

In July 2023, $CRWV issued their "DDTL 1.0", which carries a stated interest rate of SOFR + 9.62% (resulting in an effective interest rate of 15% as of 9/30/25).

In July 2025, $CRWV issued their "DDTL 3.0", which carries a stated interest rate of SOFR + 3.00% (resulting in an effective interest rate of 9% as of 9/30/25).

The DDTL 3.0 facility is specifically ear-marked to fund CapEx related to CoreWeave's contract with OpenAI - its "riskiest" contract, given nearly all of CoreWeave's other revenue is derived from investment-grade counterparties ($MSFT $GOOG $META $NVDA $IBM etc.).

So in the span of just 2 years, CoreWeave's lenders were willing to provide it with additional capital at a ~600 bps lower spread... which obviously implies a significant reduction in $CRWV's cost of capital... and a significant improvement in $CRWV's deemed creditworthiness.

This signal from CoreWeave's actual lenders, who are:

- Committing billions of dollars to fund its "riskiest" customer contracts

- Accepting ever-declining spreads on their loans

- Agreeing to covenant amendments to accommodate the delay in one of $CRWV's data centers

tells a very different story with respect to the market view's on $CRWV's credit profile than the noise coming from some small trading volumes in illiquid CDS instruments.

Strong price performance for the bitcoin miners transitioning their power capacity to HPC over the past few trading days, but there is still deep value in my opinion.

All of the companies still trade at a 7% implied cap rate or higher just on existing leases as opposed to your traditional datacenter companies $DLR and $EQIX.

I’d expect fair value to be close to a 6% cap rate and you still have the potential of additional leases to be signed at sites within each companies pipeline. I like the entire basket of bitcoin miners even after the recent run-up $IREN, $WULF, $HUT, $CIFR, $CORZ, $APLD

$WULF currently trades at a 10.3% cap rate. If you value take the annual NOI of its current leases divide it by 6% cap rate subtract debt and any unfunded capex and then add back cash and divide by shares outstanding you get an implied share price of ~$24.

You don’t need to look at charts and TA, this is fundamental value. Cap rate compression will come as time and execution risk of on time delivery burns off.

Happy New Years all Bitfarmers!

I'm pleased to announce the strategic sale of our Paso Pe site and decisive rebalancing of our energy portfolio to 100% North American. This transaction brings forward an estimated two to three years of anticipated free cash flows from operations to be reinvested into our North American HPC/AI energy infrastructure in 2026, where we believe we will be able to generate much stronger returns on our invested capital with HPC/AI. The sale of Paso Pe is the culmination of a series of transactions to completely exit Latam, and refocus the company, its management team and capital on 100% North American power and infrastructure for HPC/AI.

$bitf

https://t.co/wOzWKM4wzP

Everyone hyping privacy coins as a major theme for 2026. It’s a nice convenient narrative, but “privacy” isn’t some monopolistic moat only Zcash and Monero have. Privacy exists on a spectrum and can be achieved in a number ways especially on other L1 blockchains with significantly more adoption and usage.

Bitcoin could even add a ZK opcode at some point in the future and several teams are already working on ZK rollups on Bitcoin.

Privacy coins probably go higher, but this a greater fool trade.

Still incredibly bullish on bitcoin miners converting MWs to HPC/AI. Miners that have already signed HPC leases, $CIFR, $HUT, $WULF, $CORZ, $IREN trade at an implied cap rate of around 8.5-11% as compared to gold standard datacenter reits $DLR and $EQIX which trade at a 4.5-5% cap rate.

I’m super bullish on cap rate compression between the miners and these datacenter reits. It’s really a matter of time weighted risk, vs asset quality risk.

The spread exist because of fears of the miners being able to deliver completed projects on time and being able to fund construction without dilution. Once the projects are delivered and revenue starts these risks go virtually to 0 which should close the discount.

On forward leases they should be valued at a more normalized cap rate closer to 5-6%. As the miners will have proved that they can deliver for the hyperscalers.