As Chair of C21, I am proud of the transaction we announced today with Vireo.

In this market, I believe the right objective was not to wait for a “massive premium” exit that may or may not come. It was to skate to where the puck is going.

The cannabis industry is entering a phase where scale, access to capital, operational depth and public-market relevance will matter more than ever. Vireo brings those attributes, along with a rapidly growing platform, strong Nevada presence, and a leadership team we have real confidence in.

For C21 shareholders, this is not an exit — it is continued ownership in a larger company that we believe is best positioned for the next phase of the industry. We negotiated what we consider a very fair share of the combined equity, especially when measured against the operating contribution C21 brings in revenue, EBITDA, retail strength and Nevada market position.

I have always believed C21’s assets deserved to be part of a platform capable of attracting the premium multiple that quality, scale and growth should command as the industry unlocks.

That is what this transaction is about.

Proud of our team, grateful to our shareholders, and excited for what comes next with Vireo.

$CXXI $CXXIF $VREO $VREOF $MSOS

Thanks Noah! Very excited about this deal. This sector is far from playing out. We are now positioned with the required scale and profitability, and a good share of combination. Vireo is not fully understood but is a fantastic story that we are proud to be a part of. It’s all about the numbers!

@ErichP You are the only guy I know who cheers for a derivative. Time to turn the lens to the fundamentals. Just maybe the liquidation of $TOKE is a relevant fact impacting market prices. Indiscriminate selling.

OPTIONS IMPACT VISUALIZED

Let’s put some numbers to the concept. Here is the rebalance impact at various MSOS levels based on current Jan 16 open interest. The assumption here is that options are “delta hedged” and that those deltas will be zero or one at expiry depending on the then MSOS level.

In simpler terms, market makers will be required to buy a significant number of shares should MSOS rally. Conversely, a MSOS sell-off will be met with market maker share liquidations as we witnessed on Dec 18th. (not the only force we saw impacting the 18th)

The gun is loaded!

Nice work. Keep peeling the onion! In this piece I feel you underplayed an important component that you raised in an earlier post. Silencing social media goes well beyond closing the channel for investors. It turns off the oxygen for social/sentiment based algos to play and forces them to the sidelines. That is not a small impact.

Great data mining! Short Exempt rule is there to offer supply when there is none. Who needs it in a freefall? The market was forced into heavy sell programs thru the crash. That means Market Makers would (should) be a buyer of MSOS and a seller of underlyings. Again, in that environment, who needs short exempt unless it is being used as a weapon?

@misssmisato This Google snippet seems to support your thesis. It is just one platform but don't know how to pull broader data... https://t.co/u5JqWiOL5C

@misssmisato Interesting. I assume the perpetrator's algos are set up to ignore the silence (or watch for it to end)? Does muting thru a DDOS style attack leave footprints that are still visible?

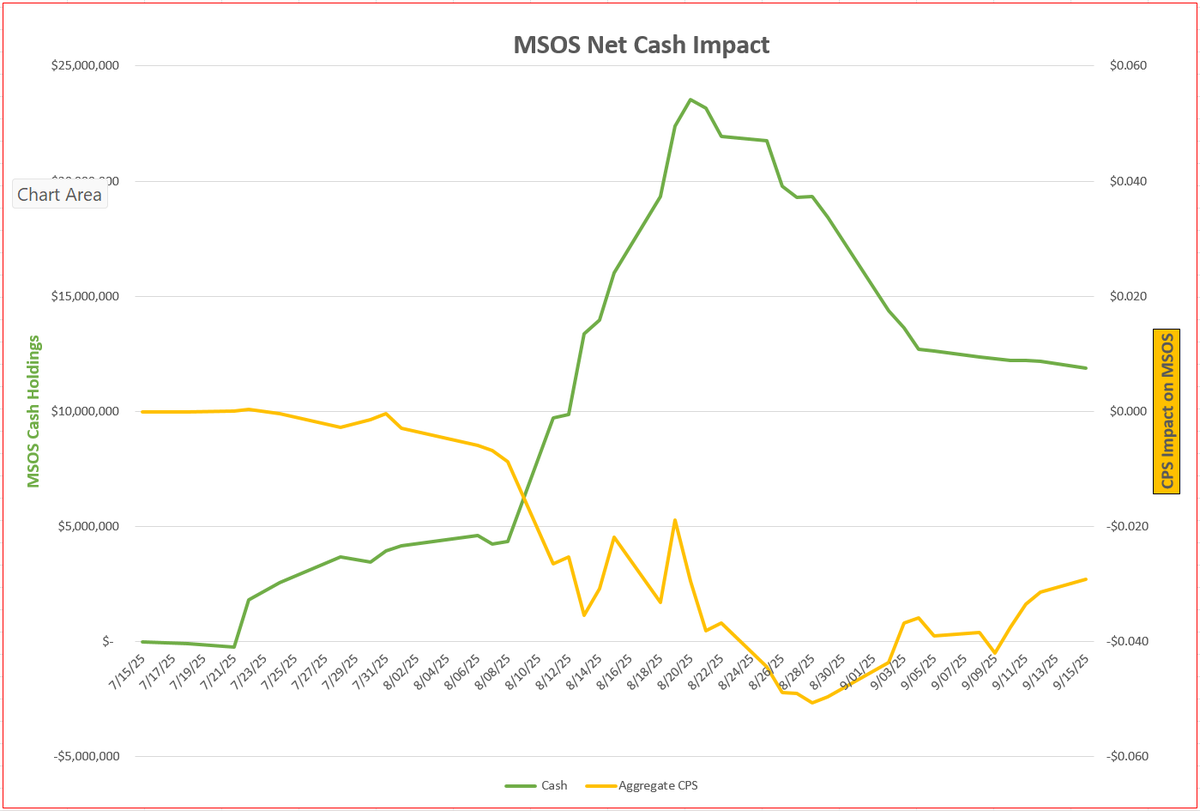

Dank, not sure you are asking the right guys but that never stops me from having a view. I went back and pulled $MSOS cash position over the last 2 months which aligns with the last time the ETF was cash flat. As the chart shows, cash flooded in on Trump rescheduling rumors faster than it was deployed. Over the last month, about half of the excess cash has been deployed. At the end of the day, cash is just the 20th name in @InvestinginCan1’s discretionary portfolio. Obviously, there are a range of views on the portfolio’s construct.

Looking at the effect of holding cash on $MSOS shareholders, the maximum impact was 5.1 cents which has now recovered to 2.9 cents. This of course assumes that the ~$23M of cash could have been deployed with no market impact. But I think this mechanical assessment misses the real effect of cash holdings.

One thing we do know is that, in our current custody confined world, $MSOS remains the most significant buyer in the sector. Just like you know that Dan holds cash, so do the predatory algos. The average price movement in the portfolio over the last two months is +60%. Having a cash buffer likely holds those algos at bay rather than giving them a free reign to force further retracement and mark prices lower in an otherwise bidless world.

Bottom line – I am not saying it is a good or bad thing, but I do believe if it had all been spent at the highs, we would now be lower – all at the whims of the predatory algos that play in our (and every) sector.

Dan, I will give you my cut on @HammanShares message and how we should interpret it. Today $MSOS traded with solid buy programs throughout the day. This means that a number of the roughly dozen AP’s on this ETF would have been buying underlying names and selling $MSOS (and clipping a few cents along the way). While $MSOS can have no direct “in kind” creation mechanism, AdvisorShares has facilitated an arrangement such that AP’s can sell their shares to swap providers, swap providers enter into additional swaps with $MSOS, and $MSOS creates ETF units for the AP covering their short. This 3-legged transaction is a defacto in kind creation and has been good for markets as there is no price impact from the AP unwind.

AP’s however are not obliged to participate in this mechanism. They can simply do a cash subscription with the ETF to cover their short $MSOS position and sell out their hedge portfolio of underlyings into the close. This is what used to cause the big end of day sell offs on big rally days that everyone used to (and obviously still do) scream about. AP’s actually make additional profits from an aggressive sell-off into the close.

I interpreted Noah’s comment to say we have naked cash subscriptions inbound which means those AP’s will be market sellers into the close. That is exactly what we saw. I think people are confusing cause and effect. I appreciate knowing when EOD market selling is coming. At least people can position to absorb it. Frankly, I wish there was a formal mechanism to be more aware of these flows rather than just getting pummeled in the last 5 minutes.

Hope this helps...

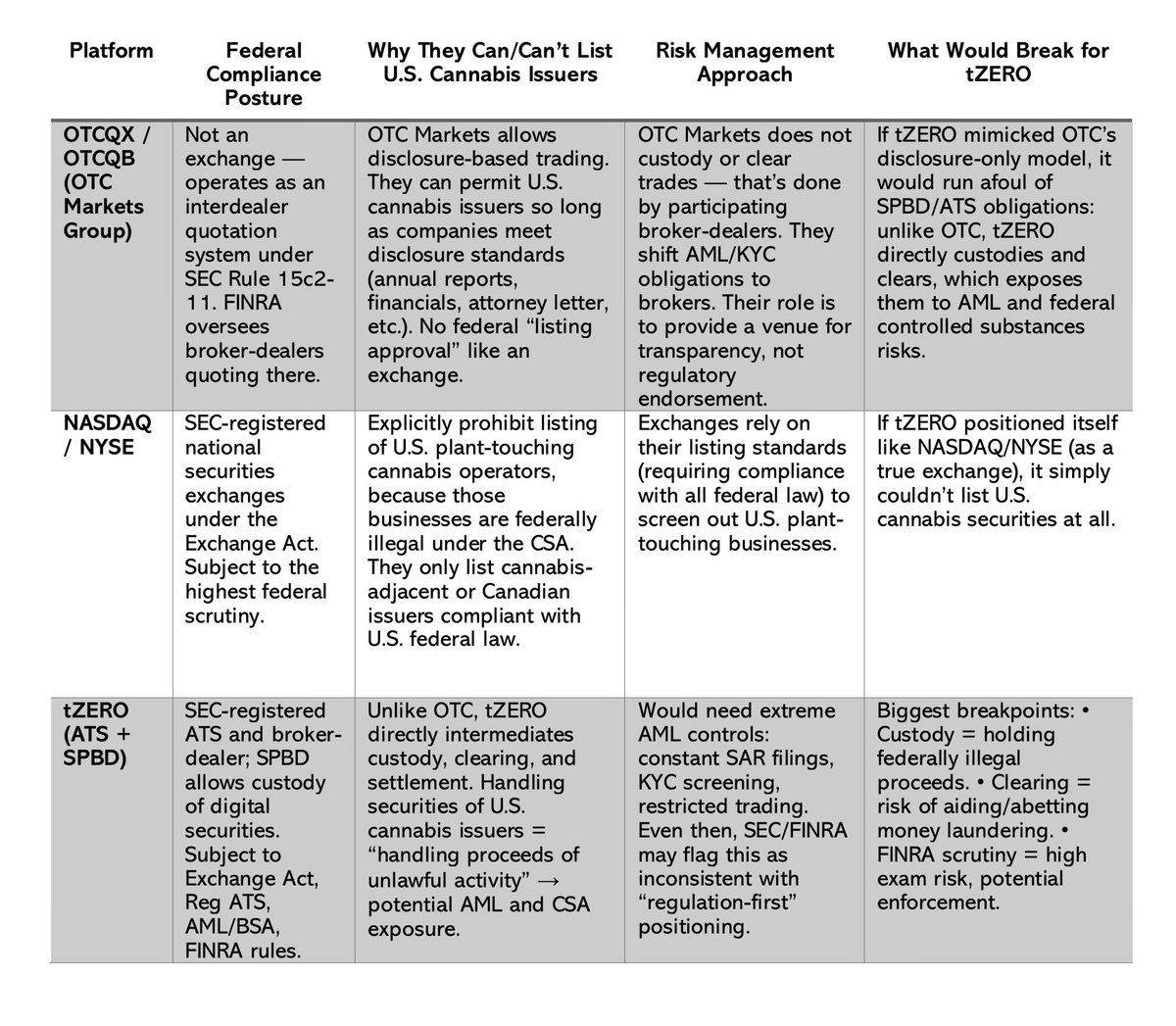

I was posed an interesting question around potential alternative solutions to the cannabis custody crisis (@tZERO). Unfortunately as you can see below, there is no easy way out without reform. I was reminded of things that I think we take for granted in how our sector functions in US public markets…

@tZERO@marcuslemonis@AlderLaneEggs@todd_harrison@bmacd36@tZERO Gents, if only there were a platform to be the base layer for the impending growth of the next great American growth industry - cannabis healthcare? Or would it be same issues as currently exist, (compliance!)? Cheers J

The cannabis sector’s echo chamber seems slow to learn. As a $GTBIF shareholder, I invested based on its strong fundamentals. But fundamentals alone don’t drive price action - especially when key players thwart liquidity inflows into the name. Fact: Since June, $MSOS has boosted its $GTBIF position by 14% (+2.5M shares, with over half since Aug 1), compared to $CURLF (+26%) and $TCNNF (+21%). These inflows have directly impacted performance: $CURLF surged 200%, $TCNNF gained 75%, while $GTBIF lagged at +37%. As a result, $GTBIF’s weight in $MSOS has dropped by a third, meaning market makers need 33% less $GTBIF to hedge ETF flows, eroding its historical edge.

Conspiracy theories about $GTBIF being suppressed don’t hold up. Why cap the company with the strongest fundamentals at +37% while the next 11 names in the sector average 95% gains - including $PLNH and $GLASF, despite their recent struggles? Fundamentals matter, but positive price action requires more buyers than sellers - every time. If management thinks $MSOS is a “bad” investor, it’s their job to attract others. In a sector with limited liquidity and compromised custody, that’s easier said than done. Good luck.

Ben, you are now worried that $MSOS can't buy more $GTBIF? I thought you didn't want that. Maybe you've seen the light! Anything could be true but I doubt this is. If it was, $MSOS would trade more like a closed end fund and not track its underlying assets within a penny or two. We aren't seeing this. Time will tell.

The three lead names within $MSOS traded rank with $TCNNF becoming the top holding at 23.6%, $CURLF remaining in second at 23.0% and $GTBIF dropping to third at 22.9%. Below is the updated scorecard.

Whether you believe in correlation or causation, today we saw $MSOS pour $3.0M into $TCNNF which in turn rallied 20%, $2.7M into $CURLF which rallied 13%, and $0.3M into $GTBIF which managed a +10% performance. This compares to a relative value shift between #1 & #3 holdings of $18M as price was again the primary driver of rank. These names maintained in aggregate, 70% of the $MSOS portfolio.

The recent shifts in $MSOS weightings are worth a closer look. On August 1, $GTBIF dominated with a 30.5% weighting, leading second-place $TCNNF by over 9 points. Just seven trading days later, the picture is quite different. $GTBIF's weighting has plunged by 22% to 23.8%, while $CURLF’s weighting has rocketed by 25% from its third-place spot of 18.2% to 22.8%. $TCNNF remained relatively flat – up slightly to a 22% weight. Overall, these three heavyweights now represent 69% of $MSOS down from 70% on Aug 1st.

This has been mostly driven by price action. $GTBIF experienced a 21% price gain as MSOS’ share position in $GTBIF grew by 7.1%. $CURLF's price performance had a massive 92% rally over the same period alongside an 8.7% increase in $MSOS holdings in the name. $TCNNF held its weighting with a 60% price gain and a 8.5% share holding increase by $MSOS.

It shows that its not just your horse's speed but the entire field's pace that determines the winner.

As to why, rescheduling could have an amplified impact on $CURLF's leveraged balance sheet, or custody restrictions (hitting $GTBIF and $TCNNF but not $CURLF) might be fueling the $CURA buying spree.

It's still early in the race but definitely a fun one to watch.

The recent shifts in $MSOS weightings are worth a closer look. On August 1, $GTBIF dominated with a 30.5% weighting, leading second-place $TCNNF by over 9 points. Just seven trading days later, the picture is quite different. $GTBIF's weighting has plunged by 22% to 23.8%, while $CURLF’s weighting has rocketed by 25% from its third-place spot of 18.2% to 22.8%. $TCNNF remained relatively flat – up slightly to a 22% weight. Overall, these three heavyweights now represent 69% of $MSOS down from 70% on Aug 1st.

This has been mostly driven by price action. $GTBIF experienced a 21% price gain as MSOS’ share position in $GTBIF grew by 7.1%. $CURLF's price performance had a massive 92% rally over the same period alongside an 8.7% increase in $MSOS holdings in the name. $TCNNF held its weighting with a 60% price gain and a 8.5% share holding increase by $MSOS.

It shows that its not just your horse's speed but the entire field's pace that determines the winner.

As to why, rescheduling could have an amplified impact on $CURLF's leveraged balance sheet, or custody restrictions (hitting $GTBIF and $TCNNF but not $CURLF) might be fueling the $CURA buying spree.

It's still early in the race but definitely a fun one to watch.

No real way to know but here are my thoughts. Nothing to do with exchange - that is just the utility. Sometimes we see big tick downs across multiple names in the ETF when someone is liquidating against a cash sub - maybe here as GTI, TRUL & VRNO also got tagged a bit on the close. Also can be algo wanting a level, or just a random print. Tape shows the race of the 15:59:59 100 lots with a print at both 1.32 & 1.43. Looks like a missed high sale. Based on the last 10 seconds, 1.32 looks like the fairer price. You choose.

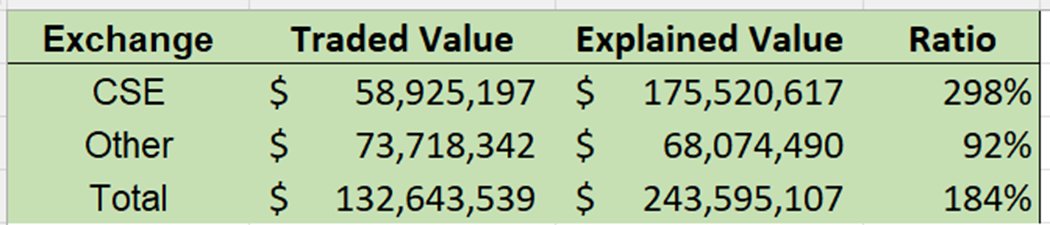

Today highlighted the impact of custody challenges in the U.S. cannabis sector. Within the MSOS ETF, three companies - $CURLF, $TSNDF, and $VFF – have been able to structure to avoid custody issues, which has also enabled their listing on the TSX or Nasdaq. Their trading performance today starkly contrasted with the rest of the sector. These three names recorded a combined trading value of $74M, compared to $59M for the 14 $MSOS constituents still facing custody restrictions (based on the highest volume exchange). The disparity is even clearer when comparing MSOS's "Explained Value”. CSE-listed stocks showed three times the notional value within trades of MSOS compared to their direct trading volume, while MSOS trades reflected just 92% of the direct volume for the three custody-compliant names. This isn’t about “bucket shop exchanges” - it’s about the ability to custody and trade. You can’t trade what you can’t hold. Rescheduling cannabis and implementing SAFE banking will level the custody playing field, unlocking broader trading opportunities in all names.

@HenryLuMencken Almost at 6M volume on TSX. This is the much-delayed benefit of what $CURLF & $TSNDF did when they uplisted. TSX custody didn't really matter much during a falling knife environment but it matters now when interest comes back to the space on such big, gamechanging headlines.