I really enjoyed talking to @benjaminfelix and @MarkMcGrathCFP about financial planning using the lifecycle model of economics vs SWR.

I’ve listened to the podcast for years and it was a privilege to be on the other side discussing a topic that’s close to my heart!

HOW TO ABANDON THE PRESENT VALUE FORMULA IN POLITE COMPANY

While retail investors are free to completely abandon the present value formula whenever they so desire, professional sell-side research analysts do not have such freedom. The professional standards force those analysts to follow a set of complex rules and social conventions resembling a tea ceremony to do so.

The research analyst has a target price that has to be about 15% above the current price. Then he must construct a set of cash flow forecasts, long-term growth forecasts, and discount rates that mechanically justify that target price.

In a bubble, the price is unjustifiable, which means that those forecasts must also be unjustifiable, but they must appear on the surface to be as justifiable as possible. Furthermore, the near-term cash flow forecasts must actually be relatively accurate because the reality of those near-term cash flows will, by definition, be revealed in the near term.

The two main ways analysts can tune their present value formula to justify the unjustifiable target prices are (1) pushing out the earnings in the multiple and (2) increasing the long-term growth rate. The first method simply says that the front page of the report will not compute multiples based on year 2026 or 2027 earnings, but year 2030 or even year 2040 earnings. This is relatively safe, as both the analyst and the institutional investor listening to the analyst are likely pursuing other career paths by 2040, when those 2040 earnings fall short of the forecasts.

The second method is just to increase the terminal value and terminal multiple after the explicit forecast horizon by increasing the long-term growth rate forecast. Owen Lamont has recently written about this, but the observation that the analyst long-term forecasts become unrealistic in a bubble is almost as old as the field of security analysis itself as each analyst covering each stock has to stretch the long-term growth forecast higher and higher.

Although some stocks may meet these high long-term growth forecasts, at some point of the bubble they will aggregate for the whole market to a level that is almost certainly impossible for even the godliest Machine God to produce. This observation is also not original but has been made, among other people, by Cliff Asness in his “Bubble Logic” piece.

A good proxy for Step 4 of the bubble is to compute the difference between aggregated individual stock analyst long-term growth forecasts and macroeconomic analysts’ long-term GDP growth forecasts. (This may be the sole case in which macroeconomic analysts’ forecasts of anything have any utility.) When the bottom-up LTG aggregated across stocks is unusually high compared to the long-term GDP growth forecast, that is evidence of the professional investors taking the fourth step and abandoning the discipline of the present value formula in a polite way.

Season 1 finale of Econ To Go is live. I joined Neale Mahoney, Director of the Stanford Institute for Economic Policy Research, for a conversation on financial literacy, why it matters, and what we can do about it. https://t.co/AjZF4RibVf

What I have in mind on stock returns contaminating earnings is best illustrated by Intel in the late 1990s and early 2000. Every time they were about to miss earnings expectations that were running away, they simply realized some gains from their huge venture capital portfolio. Those gain realizations transactions were easy to execute in 1999, but impossible to execute in 2022 because the market had crashed. That's the most blatant way in which stock market gains made it into earnings.

THE LIFE CYCLE OF A BUBBLE

1. A genuine advancement creates real productivity gains. A real technological or economic improvement increases productivity and leads to genuine revenue and earnings growth.

2. Stock prices leak into reported profitability. Rising stock prices improve reported earnings, financing conditions, collateral values, and perceived business performance.

3. Reported profitability drives real investment. Companies increase hiring, capital spending, construction, expansion, and speculative investment because of their own or their customers’ reported profitability.

4. Bubble beliefs and abandonment of present-value discipline. Investors stop focusing on discounted cash flows and begin relying on continuing gains from the greater fool theory, believing they can sell later at a higher price.

5. Inflows from sideline investors. Previously cautious investors enter the market in large numbers. New money from existing and new investors participation drive prices higher.

6. Extreme overvaluation. Prices rise far above historical normal multiples of reported fundamentals, even ignoring the fact that reported fundamentals have been driven by rising stock prices.

7. Issuance. Companies take advantage of high valuations through IPOs, secondary offerings, stock-based acquisitions, SPACs, and insider selling.

8. Exhaustion of inflows. The flow of new investors starts shrinking while existing investors approach their risk and leverage limits. Volatility and dispersion grow and gains become less uniform across stocks.

9. Earnings disappointments from slowing price appreciation. As stock prices stop rising rapidly, the earlier boost from higher valuations into earnings weakens or reverses. Companies begin missing expectations.

10. Stock-price collapse with high volatility. Confidence in both the fundamental growth and in the greater fool theory break down and prices fall sharply. Volatility rises further as leverage unwinds.

11. Bear-market rallies and progressively greater exhaustion. Bargain hunters and frustrated latecomers repeatedly buy the dips, creating violent temporary rallies that fail. Markets make lower highs and lower lows.

12. Capitulation, abandonment, and normalization. Bubble participants eventually give up in disgust or exhaustion. Volatility falls, valuations normalize, and the market returns to more ordinary behavior.

$1 billion translates to about $2.86 per person in the US and $0.12 per person in the world. Steve Jobs and Jeff Bezos and many other entrepreneurs surely have produced more value per person than that.

Scientists who make useful discoveries can produce billions of dollars of value too. But due to the public goods nature of science, scientists are not able to capture a share of that value. So we get too few scientists and too little science—the tragedy of the commons. Government funding and philanthropy try to fix this, but there is still far less research than there would have been if scientists had earned a fraction of the value they produce.

The fact that entrepreneurs, unlike scientists, are able to capture a share of the value they create, is a good thing.

AOC: “There’s a certain level of wealth and accumulation that is unearned. You can’t earn a billion dollars. You just can’t earn that. You can get market power, you can break rules, you can abuse labor laws, you can pay people less than what they’re worth, but you can’t earn that”

Technology has made it easy to invest well—you can buy a diversified portfolio of stocks with the click of a button. It has also made it easy to gamble away your wealth on risky bets with negative expected returns.

The return on financial education has never been higher.

Bettors expect to break even. They actually lose 7.5 cents per dollar wagered. A new IFDM policy brief on sports betting, behavioral bias, and what consumer protection in this space should look like:

https://t.co/WpQWhtc8bc

Bettors expect to break even. They actually lose 7.5 cents per dollar wagered. A new IFDM policy brief on sports betting, behavioral bias, and what consumer protection in this space should look like:

https://t.co/WpQWhtc8bc

I think people should be allowed to lose money however they like, and I resent the rising trend of lowest-common-denominator temperance thinking. But I'm not sure "less likely to lose money than options day trading" is an ironclad position

Yes, delaying action makes Social Security reform harder. But NOT for the politicians and citizens who did the delaying, who avoided 3 decades of higher taxes or lower benefits.

Those costs then get borne by younger Americans. That's generational inequity in action.

The neat thing about expressing percentage changes using logs is that the rise and fall would be symmetric. The price increase from $100 to $600 would be ln(600/100) = 179% and the price decrease from $600 back to $100 would be ln(100/600) = -179%. Cancels like you would expect.

RFK Jr: "A Democratic senator claimed it's mathematically impossible to have a drug drop by 600%. I said, 'Well, if the drug was $100 and it raises to $600, that would be a 600% rise. If it drops from $600 to $100, that's a 600% savings.'"

Trump: "Right"

In the last 30 years, the number of public companies has been cut in half. The situation has gotten so bad that the Wilshire 5000 index, founded in 1974 to track the broadest portfolio of all US publicly traded stocks, now listsonly about 3700 stocks!

In my latest piece in @washingtonpost, I explain how frivolous class action suits by trial lawyers have contributed to that problem and how the Supreme Court can strengthen public markets by curbing abuses of securities law.

The losers--ordinary Americans who have fewer options for investing their retirement savings and the American economy which has less opportunities for growth and innovation.

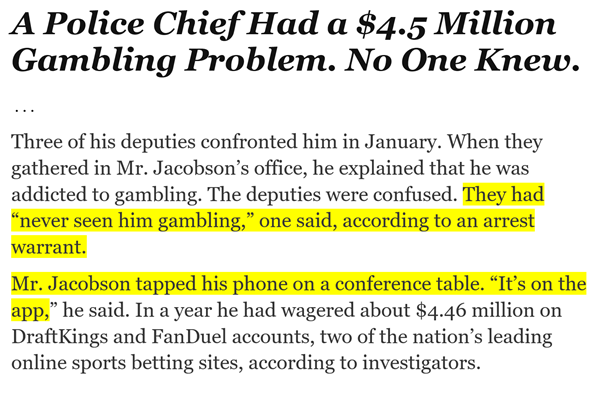

Online gambling is the silent epidemic. You will probably know if someone close to you has a drinking or a drug problem. You will see the effects. But people can end up in dire straits with an online gambling addiction without any visible warning signs.

via NYT

Sports betting is reaching teenagers at an alarming rate. One important lesson we can teach them is the difference between gambling and investing. A timely read for Financial Literacy Month: https://t.co/6bHq3Vopcd