Former analyst and portfolio manager. Fundamental buy-and-hold investor. Talking stocks and markets. Politics and golf occasionally. This is not advice.

I’m prepared to be proven wrong, but deep down in my gut I feel like $BR at $150, $INTU at $310, and $MA at $470 will prove to be exceptional entry/add points.

@jefernandez8@stripe Not really. I think stablecoins are a solution in search of a problem that really doesn’t exist for consumer payments, especially in developed markets.

I'm not sure why payment and fintech stocks gap down from day-to-day (b/c it happens so frequently) but I'm guessing this *may* be a reason for today's decline. @stripe $v and $ma are close to launching a stablecoin infrastructure platform for 'mainstream' payments in potential collaboration with $coin. While the success of stablecoin payments are going to depend on the willingness of consumers to adopt (which I don't think there's a strong case for as of yet), the major players are certainly planning for that eventuality. Also, dovetails with the theme of most of the 'value' in payments being accrued to @stripe and away from the public players like $adyen $gpn and $fisv.

Payment giants Stripe, Visa, Mastercard said to be among backers of soon-to-debut stablecoin platform https://t.co/qofRGqiQpK via @coindesk

@BarnieTaintpipe@stripe Are these stocks really going down that much on tariffs/Iran, while the rest of the market shrugs it off. It seems hard to believe.

$COST (43x) $CTAS (32x) $WMT (39x) $TJX (29x) $ROST (29x) $SHW (25x) $ORLY (26x) all trade at higher multiples than $V (23x) and $MA (24x). Does that seem right to you? It doesn't to me.

Each quarter, I aggregate KPIs across payments and fintech to assess performance. Here is the Q1 2026 edition. Despite compressing multiples, fundamentals remain very solid.

$v $ma $axp $fisv $tost $adyen $shop $pypl $xyz $gpn $four $jkhy $afrm $klar $chym $bill $cpay

Sheesh. $ADYEN falls nearly 7% on a downgrade from BNP Paribas. “Share gains are slowing” Are they? FXN volume growth was likely mid-20s % in Q1 vs. HSD for card volumes in developed markets. Sentiment not bad enough apparently.

Update: Made the swap this morning selling $MSCI and opening a starter in $MA. Payments and fintech holdings by sizing: $V $GPN $INTU $XYZ $ADYEN $FOUR $PAYX $MA $BR

Hard to believe a name like $MSCI (30x) trades at 6-7 point premium to $MA (24x) and $V (23x). Bought the $MSCI dip in February. Feel like a swap into $MA may be the play here.

Hard to believe a name like $MSCI (30x) trades at 6-7 point premium to $MA (24x) and $V (23x). Bought the $MSCI dip in February. Feel like a swap into $MA may be the play here.

Mostly agree with your line of thinking. My concern is longer-term and what the appetite is to push the envelope further when growth from this round of monetization eventually moderates. Also, consumers like (love) the products no doubt, but how about regulators in different political regime. All that being said, these stocks are not expensive, so a lot of this may already be baked in.

$CHYM $XYZ $KLAR. One of the key themes in fintech currently is how aggressively companies are monetizing their base. While I'm not opposed to this strategy, I think it's important to understand long-term value creation will be driven by customer growth and satisfaction. So any near-term monetization efforts must be balanced against this objective. It is also important to note that while fintech lending products are likely better for consumers than something they could obtain from a bank (if they could get anything at all), the 'consumer friendliness spread' is likely narrowing. Here are a couple of examples:

Chime: $CHYM is actively moving debit card spend (which generates a low-90bps take rate) to its secured credit card (close to 200-bps) and outbound instant transfers (175-bps). On the lending side, $CHYM recently introduced a variable pricing structure on MyPay loans (its EWA product), which has resulted in yields increasing from about 190-bps to 260-270bps (still among the lowest in the industry). Additionally, $CHYM is ramping Instant Loans, which charge $5 for every $100 borrowed (capped at a 36% APR).

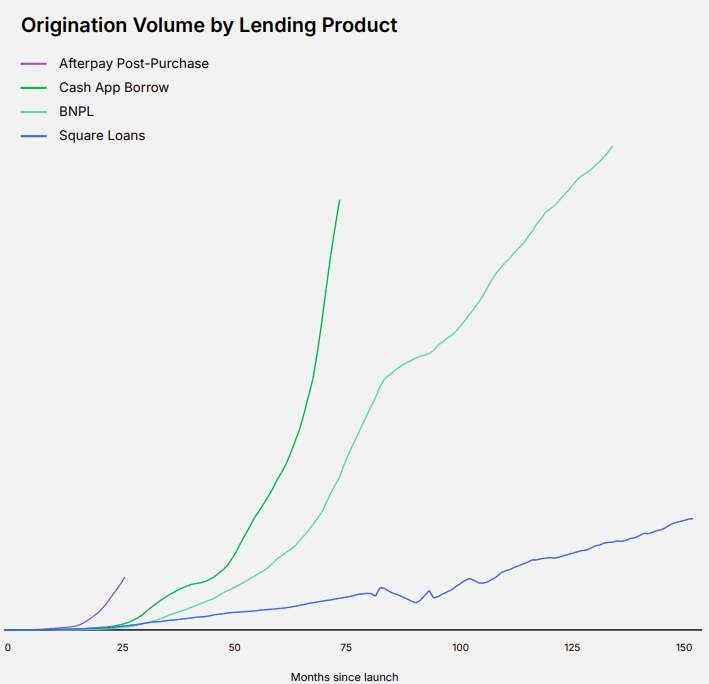

Cash App: $XYZ's (which I'm long) Cash App gross profit has inflected from 12% growth in Q1'25 to 40% in Q1'26 (excluding Bitcoin) despite the fact overall customer growth remains modest (Cash App MAUs were up 4% in Q1, an improvement from flat a year ago, and primary banking actives are up 18% vs. 17% a year ago). How are they doing it. Borrow originations, which yield ~5%, were up 175% in Q1. Further, post-purchase BNPL is ramping faster than any lending product in $XYZ's history (see chart below). To the best of my knowledge, $XYZ is trading a traditional pre-decisioned Pay in 4 take rate in the 3-4% range for a debit card take rate of ~1% PLUS up to a 7.5% fee assessed on the borrower (so an incremental 4-5 points). They are also rolling out the feature for P2P transfers with a similar 7.5% fee.

Klarna: $KLAR is ramping fair financing lending, its high-APR (up to 36%) installment loan product. In Q1, fair financing represented >12% of total group GMV, nearly double the rate from a year ago. In the U.S., fair financing was nearly 40% of GMV in Q1.

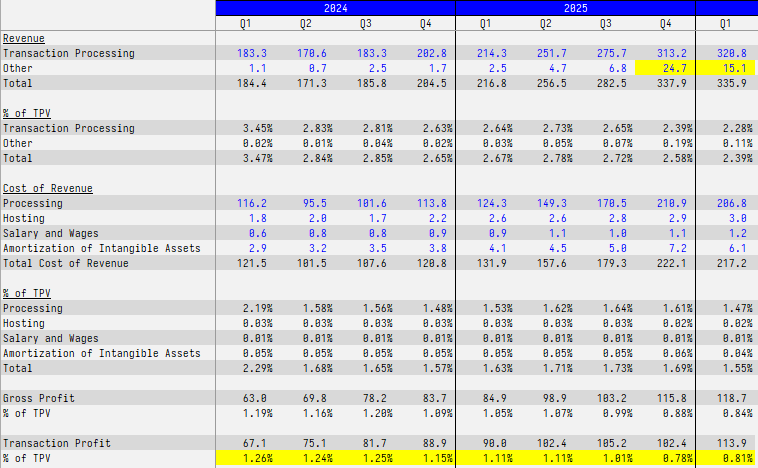

? for the $DLO experts: After taking an initial pass through $DLO's financials one thing that jumped out right away was the significant jump in 'other revenue' during Q425/Q126, which boosted the gross profit take rate.

If you just take transaction processing fees less processing costs (i.e., transaction profit), the decline in that take rate is more severe. It fell 37-bps and 30-bps year-over-year in Q425/Q126 vs. a 21-bps year-over-year decline in both quarters on a gross profit take rate basis.

Other revenue is described as transactional taxes, minimum monthly fees, transfer and initial setup fees.

My guess is that most of the other revenue is from transactional taxes, which is passed-through as a part of processing costs. Does anyone know if that's the case?