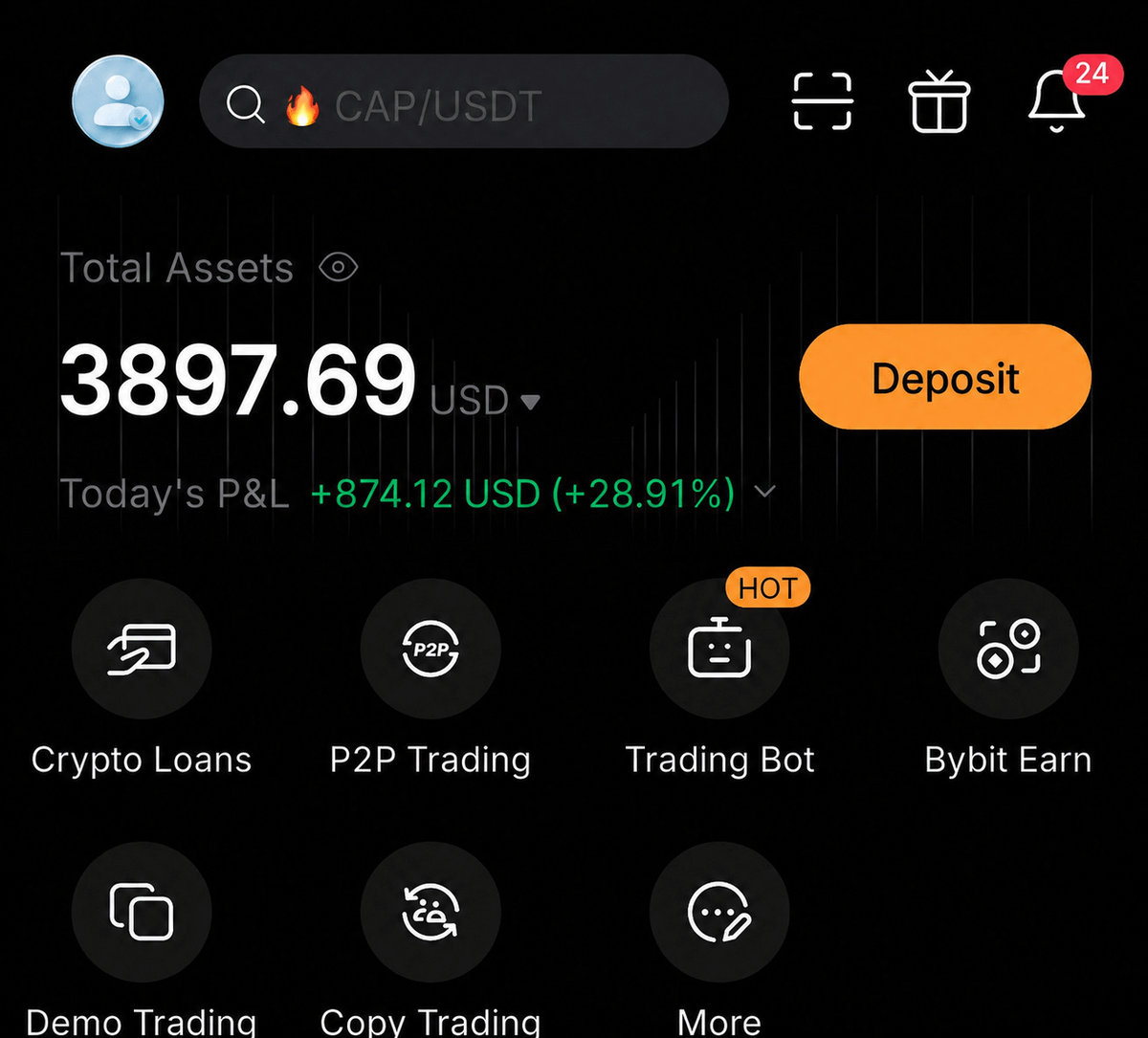

I didn't expect Claude Fable 5 to perform like this

I connected it to a fresh crypto account

Here are the results after 4 days:

Starting balance: $100

Current balance: $3,897

I'm thinking about selling this setup soon

But I'll also give it away for free to 3 people who like + reply to this post

Do you understand what this means?

The smart end to end agents are coming.

Compute demand is about to 1000x again.

Long $NBIS is really a nobrainer here.

Also, was quiet last few days because I have a big personal announcement tomorrow.

AI Interconnect for Data Centers (Watchlist)

Breakdown of companies worth researching that could be great buying opportunities for the long-term:

1. Lasers & modules: $SIVE, $COHR, $LITE, $AAOI

2. Analog chips: $SMTC

3. Connectivity silicon: $CRDO, $MRVL, $ALAB, $MXL

4. Foundry: $TSEM, $XFAB

5. Substrates/Epitaxy: $IQE, $AXTI, $SOI

6. Glass processing & substrates: $LPK, $GLW

7. Test equipment & services: $AEHR, $TRT, $VIAV

8. Others: $NOK, $PENG

Notes:

- EMS like $JBL, $FLEX, $CLS, $FN weren't considered but are worth researching for more diversified exposure.

- $CSCO & $ANET are two established giants in the industry. Since the focus is on emerging/more upside companies, they also weren't considered.

- $ADTN, $CIEN - Still researching and so they weren't added yet. Worth looking into as well.

Top picks:

- $AAOI $SIVE (1)

- $SMTC (2)

- $CRDO $MRVL (3)

- $TSEM (4)

- $IQE (5)

- $LPK (6)

- $TRT $AEHR (7)

- $PENG (8)

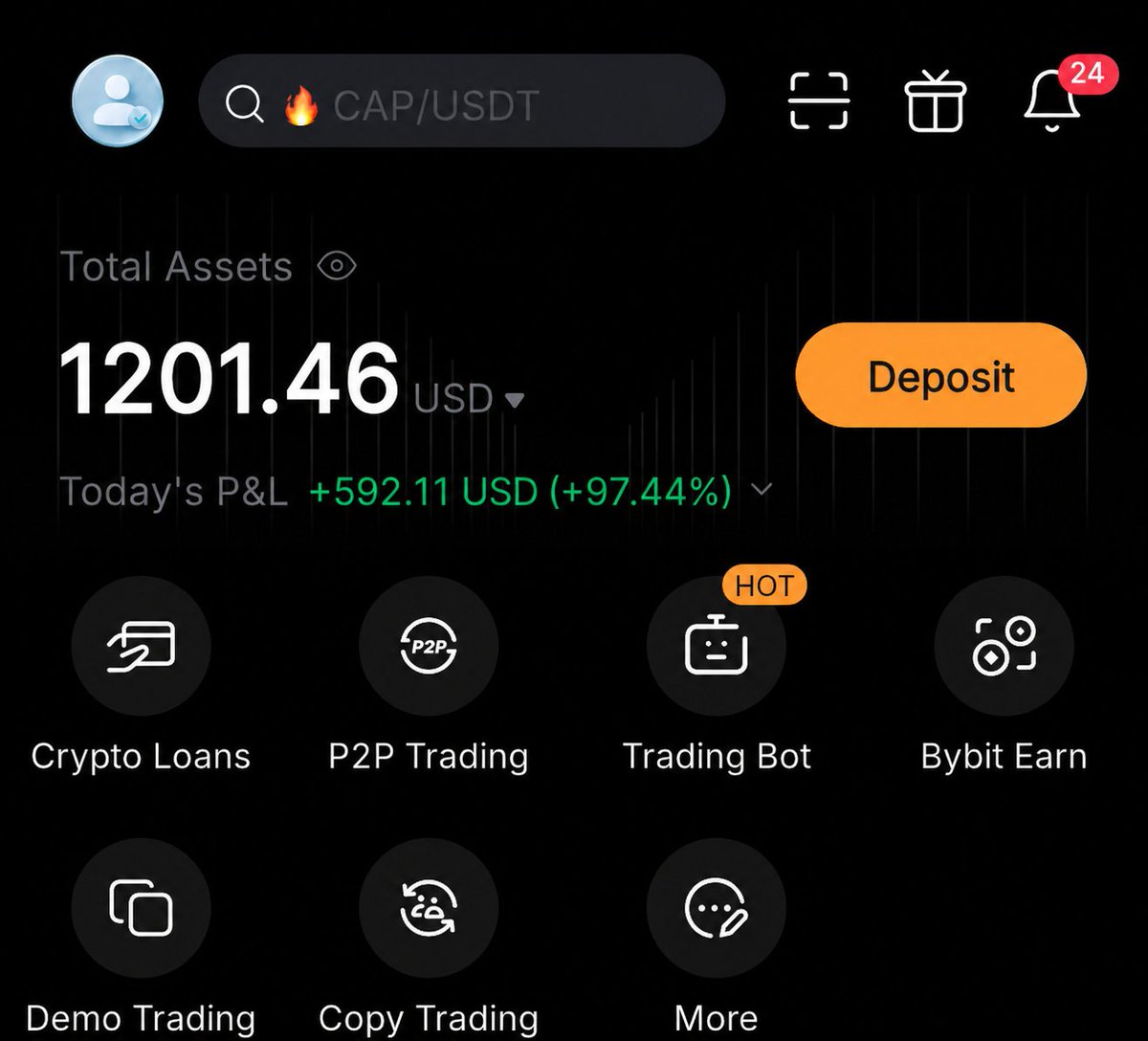

I let Claude Fable 5 trade with a fresh crypto account.

In just 2 days:

Starting balance: $57

Current balance: $1203

Like + reply and I'll share exactly how I set it up.

There's a certain stock sector not many people are talking about.

But I'm buying in here.

Let me explain why:

The sector is the $BTC -> AI pivot companies.

People hate them, but I'm loving them here.

For a couple reasons that I'll explain below.

First, I believe crypto has bottomed.

I have written multiple reasons why.

Just check my profile for this.

This means bitcoin becomes another growth engine for these companies.

Secondly, AI companies constantly need capital, and as $BTC appreciates, management can potentially do a couple of things:

- borrow against $BTC

- sell a small amount

- finance additional GPU purchases

- expand datacenters

And lastly, it creates multiple valuation drivers.

Think of a traditional AI company, the stock depends mostly on a few things: earnings, AI demand, GPU utilization, margins, etc..

But a BTC + AI company, now the stock depends on: AI earnings, BTC appreciation, treasury value, NAV expansion, institutional Bitcoin demand.

This is one of the reasons why $IREN > $NBIS here (there are more ofc, such as one being priced as trash and the other as perfection).

And a few reasons why I love all the $HIVE, $CLSK, $MARA, $CIFR type of companies here.

But not many people are paying attention to these types, yet.

We're still early.

$GCT

+3%

-24% last 3 months.

Trying to build a base around 360ma, i think overlooked not many are talking.

Don’t miss this one. 100$ stock chilling

I think this could be one of the highest-quality beaten-down growth names in the market.

Now I’m watching $GCT.

Look at $SHOP, $GLBE, $JD and even global e-commerce leaders like $AMZN and $BABA for the blueprint.

Unlike $AMZN and $BABA, which operate massive horizontal marketplaces across virtually every retail category, $GCT is a pure-play specialist focused exclusively on large-parcel B2B e-commerce and logistics.

$GCT provides an end-to-end operating platform for manufacturers and resellers by combining marketplace discovery, payments, warehousing, ocean freight, fulfillment, and last-mile delivery into one ecosystem.

The company operates 35+ fulfillment centers totaling over 11 million square feet across the U.S., Europe, Japan, and Canada while connecting Asian manufacturers directly with Western resellers.

Its marketplace continues expanding with approximately:

• $1.7B trailing GMV (+17% YoY)

• 1,377 active third-party sellers (+19%)

• 12,473 active buyers (+25%)

• 70,000+ SKUs

• Growing third-party marketplace mix driving higher margins

As more buyers join, more suppliers participate.

As more suppliers join, selection improves.

That flywheel creates meaningful network effects while proprietary logistics make the platform increasingly difficult to replicate.

Every additional transaction also strengthens GigaCloud’s proprietary data.

Now recurring marketplace activity continues accelerating, margins are expanding, AI tools are improving logistics efficiency, buybacks continue reducing share count, and management continues raising guidance.

Market cap comparison:

• $GCT: ~$1.2B

• $GLBE: ~$6B+

• $SHOP: ~$170B+

• $AMZN: $2T+

• $BABA: ~$250B+

The valuation disconnect is difficult to ignore considering GCT continues delivering profitable growth.

Recent growth has been exceptional:

• Q1 2026 Revenue: $359.5M (+32.2% YoY)

• Gross Profit: $85.8M (+34.7%)

• GAAP EPS: $1.04 (+53%)

• Non-GAAP EPS: $1.24

• Adjusted EBITDA: $45.6M (+37.3%)

• Marketplace GMV: ~$1.7B (+17%)

• Active Buyers: 12,473 (+25%)

• Active 3P Sellers: 1,377 (+19%)

• Net Margins: ~10-11%

• ROE: ~32%

Management also provided strong Q2 guidance:

• Revenue: $365M-$390M

• Midpoint above prior consensus

• Analysts project FY2026 revenue approaching $1.5B

• Continued EPS growth expected

• Ongoing share repurchases reducing float

AI is quietly becoming another competitive advantage.

New platform capabilities include:

• AI-powered demand forecasting

• Intelligent inventory optimization

• Dynamic pricing tools

• Predictive logistics planning

• Virtual warehousing

• Marketplace recommendation engine

Upcoming catalysts include:

• Q2 2026 earnings

• FY2026 guidance updates

• Continued Europe expansion

• New Classic acquisition synergies

• Additional marketplace seller growth

• Continued shift toward higher-margin third-party marketplace revenue

• AI platform enhancements

• Margin expansion

• Accelerating GMV growth

$SHOP and $GLBE are excellent e-commerce platforms.

$AMZN and $BABA dominate broad global commerce.

$GCT has established itself as one of the leading pure-play platforms in one of the most overlooked and difficult niches in global e-commerce.

Integrated logistics.

Marketplace network effects.

Asset-efficient business model.

One of the deepest moats in large-parcel cross-border B2B commerce.

Follow these legends while you’re researching $GCT moat

@riverwolf0518@brandon_Invests@Redknight8811@AlphaOwlTrading@MoMoMacro@mom0_fx@LongBullz@_LamNam_@CryptoSlider@EdgeReport91@JacobTradesX@JDynan@EdgeReport91@rahbar_rod@RK_Capital@InvestifyDaily@CompoundCurious@seahorse_anton@fundmyfund@ZeekTyt@AdityaInvests90@glocalinvestor@WeighTheStreet@BrandonWealth@WealthJourney21@Tape_Vector@KanKanandB@gulVasikova

$ZS

-33% YTD.

A leader in cloud-native cybersecurity.

This is a $300 stock trading around $150.

Another obvious opportunity to potentially double your money over the long term.

Hit that sub for $1. The research never stops here X fam.

And I still believe many of those are only getting started.

Now I’m watching $ZS.

Look at $CRWD, $PANW, $NET, and even $FTNT for the blueprint.

Unlike many cybersecurity companies that combine endpoint security, hardware, or broad enterprise software, Zscaler is one of the purest cloud-native cybersecurity companies in the market.

Its primary competitors include CrowdStrike, Palo Alto Networks, Cloudflare, Fortinet, Microsoft, $CSCO, and $NTSK, yet Zscaler continues to lead the enterprise Zero Trust and Security Service Edge (SSE) markets.

The company pioneered the Zero Trust Exchange, eliminating legacy VPNs and perimeter firewalls by securely connecting users, applications, workloads, IoT devices, branches, and now AI agents directly through the cloud.

It operates one of the world’s largest inline security clouds, processing more than 500 billion transactions every day across 160+ global data centers, protecting 47+ million users worldwide.

More than 40-45% of the Global 2000 rely on Zscaler, including 748 customers generating over $1M in ARR, while the company continues to deliver elite enterprise retention, and strong recurring revenue.

Zscaler is consistently recognized as a Gartner Leader for Security Service Edge (SSE) and remains one of the clear leaders in Secure Access Service Edge (SASE), two of the fastest-growing segments in cybersecurity.

Global demand continues accelerating.

• Cloud security is expected to grow from roughly $35B today toward $60B-$100B+ over the next decade.

• SASE is projected to compound at roughly 29% CAGR.

• SSE continues growing 25%+ annually.

Management estimates its long-term addressable market now exceeds $100B across users, workloads, applications, AI, branches, and connected devices.

Despite already serving 40-45% of the Global 2000, Zscaler has captured only a small percentage of its total addressable market, leaving a massive runway for continued enterprise expansion, platform adoption, AI security, and long-term recurring revenue growth.

Now recurring revenue continues compounding, AI adoption is exploding, margins are expanding, and management continues raising guidance.

• $ZS: ~$25B market cap

• $CRWD: ~$70B+

• $PANW: ~$110B+

• $NET: ~$30B+

• $FTNT: ~$55B+

Recent growth remains exceptional:

• Q3 FY26 Revenue: $850.5M (+25% YoY)

• TTM Revenue: ~$3.17B (+25%)

• ARR: ~$3.53B (+25%)

• FY26 Revenue Guidance: ~$3.33B (+24–25%)

• FY26 ARR Guidance: $3.74B–$3.75B (+24%)

• Data Security ARR surpassed $500M (+30%)

• Zero Trust Branch ARR tripled YoY

• Cloud Marketplace business more than doubled YoY

• Non-seat ARR growing 100%+

• Z-Flex contract value exceeded $1B

• Record 23% non-GAAP operating margin

• Strong and growing free cash flow

The AI opportunity may be even bigger.

Enterprise AI adoption across the platform continues accelerating rapidly.

• AI Protect surpassed $100M in bookings

• AI applications on the platform increased 4x YoY

• Enterprise AI/ML activity increased by as much as 3,000% in certain environments

• Data transferred to AI platforms increased 93% YoY

These products are increasing platform adoption, expanding wallet share, improving security outcomes, accelerating larger enterprise deployments, and opening another multi-billion-dollar growth opportunity.

Upcoming catalysts include:

• FY26 earnings

• FY27 guidance

• Continued ARR acceleration

• AI Protect expansion

• Agentic AI adoption

• Additional Global 2000 customer wins

• Continued Zero Trust adoption

• Additional AI security product launches

$PANW and $CRWD are phenomenal cybersecurity companies.

But $ZS remains one of the purest ways to invest in Zero Trust, SSE, SASE, and AI-powered cloud security.

I gave you the exact game plan on $SIVE.

I said to sell on the exit pump to 73 and wait for it to come to the 2 support levels as listed.

Now, here's what I'm doing next:

I'm buying some shares.

I know, I know, this might be a shocker to some, but I am SLOWLY going to DCA in here.

We got a lot of FUD here. Yes, we have some actual concerns, such as moving their Q2 report from Aug 6 to Aug 27 (which is suspicious, I will say, but there are some concise reasons for doing so).

So what'd I'd say to you is be careful here.

I don't expect a huge V shaped rebound as we all know and love.

Maybe some consolidation to the side (before breaking out of this wedge to the upside).

I do think there are other plays here (that are better). But $SIVE is getting to a very, very nice price worth adding into your portfolio here.

So, that'd my game plan: buy here, and wait out this FUD.

I'm also using this dip as a great buying opportunity for other names I love: $IREN, $AAOI, $ASYS, $OPTX, $BRUN, $SHMD.

But soon (not now), the time to sell will come.

And when that happens, I will be telling you all to sell.

I hope you will listen...

Came across an interesting report from SVRC Research called "State of Robotics 2026", published in April.

Which listed:

1. Figure AI

2. Agility Robotics $CCXI

3. Apptronik

4. $TSLA

5. Boston Dynamics

6. Physical Intelligence

7. 1X Technologies

8. $AMZN Robotics

9. Covariant

10. Skild AI

As the National Champions of the United States robotics program.

"The United States leads the world in where robotics is heading: Fundation models, OpenAI-style scaling laws applied to action, autonomous vehicles.

While losing the race on where robotics is shipping today."

Then it frames:

1. Rare Earths Exposure: from Neodymium for motors to samarium-cobalt for high-temp applications as a critical vulnerability.

2. Actuator dependency. Series elastic actuators, quasi-direct-drive motors, and precision reducers overwhelmingly sourced from Japan, Germany, and China

As one of the main vulnerabilities alongside Manufacturing velocity/data collection cost/regulations. Then their take was:

"With at least six well-funded US humanoid companies competing for a market still in early formation, we expect at least two significant consolidation events (acquisition or merger) in 2027".

With Logistics / E-commerce (like $AMZN / $FDX) and Automotive from $GM to $FORD as being the immediate top use cases for deployment.

I think it's just interesting to see a lot of my points I've been talking about reiterated by research firms. Regardless, I do think it's going to be a major frontier race between the US and China.

Agility Robotics (which I own), Tesla, Figure, and Apptronik as leaders representing the USA. Competing against Unitree, AGIbot, Ubtech, and others in China.

There is no doubting that robotics is the future of physical AI.

Here are 5 stocks you may not have heard of to play the robotics super cycle.

1. $OUST - Ouster

Ouster is a roughly $3.3 billion lidar company whose Rev8 digital platform is showing up across robotics, autonomous vehicles, and industrial machinery. Q1 2026 revenue hit $48.6 million, up 49% year over year, and the company just raised $200 million in a follow-on offering to fund production. It expanded its manufacturing partnership with Benchmark toward 100,000-plus units a year, signed AIM Intelligent Machines to put sensors on autonomous heavy equipment in mining, construction, and defense, and is working with FieldAI to help general-purpose robots navigate complex environments using Rev8's native color lidar.

My portfolio is quite covered in all scenarios.

Sure it limits my upside a bit, but I'm thematically covering a few key areas.

-> $LMND (AI Applications) did the heavy lifting today +10% (biggest position).

-> $OUST has done the heavy lifting for the last month (2nd largest position).

-> $CRDO & $AAOI for the interconnect story has done well for the last 3 months.

-> Biotech & healthcare is a smaller part of my portfolio but $ABCL, $LLY, $TEM, $CLPT, and $HROW have been steady.

-> Silver miners like $SLV and $HL or copper miners like $TMQ and $COPX haven't been strong lately but I think capital will rotate there.

-> Rare earths is another weaker area of my portfolio but again I hold conviction in $USAR long term.

Sure it's not a massively concentrated portfolio...but I still hold over 50% of the portfolio in the top 7 positions.

Upside has been very strong.

Downside has been limited.

I don't prompt Claude Code anymore.

I have loops running that prompt Fable, and my job is just to write loops.

This is the Boris Cherny method, and I have to say, it's extremely powerful.

Everything you need to get started with loop engineering (as a complete beginner):

Metí 200$.

Este bot los convirtió en +13.000$.

Y ni siquiera lo programé yo.

Cogí un proyecto open source de GitHub.

Le dediqué un par de horas en Claude Code para limpiarlo, entender cómo funcionaba y hacer algunos ajustes.

Le di a ejecutar.

Pensaba que iba a fundir la cuenta en menos de una hora.

Minimicé la terminal y seguí con mi día.

Cuando volví por la noche, ya no eran 200$.

Eran +700$.

Desde ese momento, simplemente dejo los logs abiertos en el segundo monitor y veo cómo ejecuta operación tras operación.

La clave está en el timing.

El bot espera hasta los últimos dos minutos de cada ronda de 5 minutos de BTC.

Para entonces, Bitcoin ya ha hecho gran parte del movimiento y la dirección suele estar bastante definida.

En ese momento entra a favor de la tendencia, comprando contratos que cotizan entre 0,80$ y 0,99$.

Unos minutos después, si el movimiento se mantiene, la posición se liquida a 1$.

La lógica es sorprendentemente simple:

→ Esperar hasta que falten unos 2 minutos para el cierre de la ronda

→ Comprobar que BTC ya se ha movido entre 70$ y 100$ durante ese intervalo

→ Operar siempre a favor del movimiento, nunca en contra

→ Cubrir una pequeña parte de la posición únicamente si el mercado se desequilibra demasiado (por ejemplo, 95/5)

Es como comprar un boleto de lotería cuando prácticamente ya han anunciado el resultado.

El código es público y cualquiera puede usarlo en su pc:

https://t.co/9Khz1PzJKH

Gratis.

No matter how the S-4 turns out, money is piling into $CCXI.

It is the only ticker in the US market that gets you a pure play humanoid company.

A robot maker, backed by $NVDA, $AMZN, Softbank, and Foxconn, with $300 million in binding orders already signed.

The hottest theme in the market and exactly one way to play it. Flows find scarcity every time.

$DRAM ONCE IN A LIFETIME Rare Fibonacci Pyramid

Buy Zone: 53 to 60 Target 91 down 25% from highs!

Loading up 100k minimum - LOW RISK HIGH REWARD setup

I will alert all here on X no charge - let's make some more millionaires

First, this is the bottleneck: precision actuation (motors + gearboxes + integrated force/torque sensing)

Not compute, not lidar, not even batteries it's the actuator/joint system.

Here's why:

1. It's the single biggest cost and engineering line item. McKinsey breaks the humanoid hardware stack into five domains, and actuators alone account for 40–60% of the bill of materials more than double any other subsystem.

2. The supplier base is tiny and not built for volume. Fewer than 10 global suppliers can currently produce actuators with the precision required, and the humanoid supply chain is expected to consolidate around a small set of dominant designs by 2027–2028 meaning whoever locks in a qualified position now has a durable moat.

3. There's no "off-the-shelf" solution everyone is custom-building. There is currently no equivalent of an engine supplier for humanoid actuators; every leading project is doing custom development, which is both the bottleneck and the opportunity, since it prevents the kind of automotive-style commoditization that would collapse margins.

4. It's geopolitically exposed. High-torque actuators depend on rare-earth permanent magnets, particularly neodymium-iron-boron, and China controls roughly 69% of global rare-earth mining and 90% of magnet processing capacity so even well-funded Western programs face physical supply risk, not just engineering risk.

5. It's bottlenecking pilots, not just scale-up. Specialized actuator, gearbox, and sensor suppliers operate at limited scale with extended lead times for components like harmonic drives and high-torque motors, creating delays even in today's low-volume pilot programs this isn't a 2030 problem, it's showing up right now in shipment timelines.

$VPG is the closest robotics company which controls this bottleneck, not the gearbox/motor, but the force/torque sensing that has to be embedded in every joint for a humanoid to have proprioception (knowing how hard it's gripping, how much torque a joint is under, etc.).

That's precision load-cell/strain-gauge technology, which is $VPG's core competency, and it's exactly why they're already booking humanoid orders and in engineering discussions with a fourth humanoid developer.

Leaving you with these master cheatsheet so you can SAVE it and study it. These are the top 5 robot plays: