Steven Pinker is a Harvard psychologist who wrote the only style guide based on how the brain actually reads.

Here are 10 writing fixes from "The Sense of Style" rooted in cognitive science, not grammar rules.

1) The curse of knowledge ruins more writing than laziness

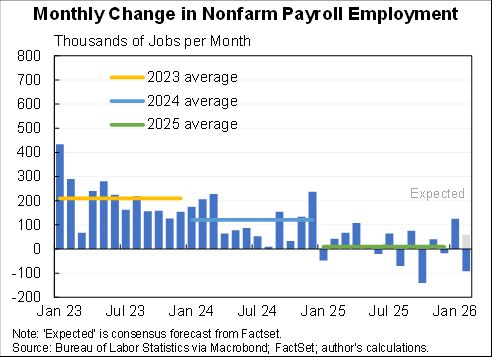

Another strong month for job growth. 172K in May with upward revisions for previous months that brings the three month average to 188K.

Unemployment rate stable at 4.3% while broader measures (U-6 and employment rate) both improved.

In crude terms two big things happening: (1) tariffs/Iran and (2) AI boom (including direct effects but also indirect like higher stock prices helping to support consumption).

Both of them lead to higher inflation but they cancel out when it comes to the labor market.

In crude terms two big things happening: (1) tariffs/Iran and (2) AI boom (including direct effects but also indirect like higher stock prices helping to support consumption).

Both of them lead to higher inflation but they cancel out when it comes to the labor market.

DOS BIOINGENIERAS CREARON UNA IA QUE PASA DE DETECTAR MUTACIONES DE CÁNCER EN UNA BIOPSIA EN UN MES A CINCO MINUTOS

Ana Gorodisch y Martina Belluomini son de Buenos Aires. Se recibieron de bioingenieras en el ITBA en 2023. Para su tesis de grado desarrollaron un algoritmo de inteligencia artificial que analiza imágenes de biopsias tumorales y detecta mutaciones genéticas invisibles a simple vista. En 2024, lo presentaron en el congreso de la American Society of Clinical Oncology. Ahí vieron que la necesidad era real y que nadie estaba desarrollando algo similar localmente.

En 2025 fundaron Kuvia. La tecnología toma la imagen de una biopsia tumoral, que ya se obtiene de rutina en cualquier paciente oncológico, y detecta en cinco minutos los biomarcadores que definen el mejor tratamiento, sin insumos adicionales. Hoy ese proceso puede tardar hasta un mes y no está disponible en todos los centros médicos.

Desarrollaron un producto para detectar un biomarcador clave en el cáncer de colon y endometrio, entrenado con los primeros datos de patología digital del país y en validación en más de cinco instituciones. Una de ellas es Biogenar, un laboratorio de anatomía patológica ubicado en Buenos Aires.

Fueron seleccionadas en Transformar Salud, la iniciativa de la Fundación Garrahan y Roche, para desarrollar una IA orientada a cáncer pediátrico. Y el Harvard Health Systems Innovation Lab destacó su solución entre los desarrollos globales de IA en salud.

Hoy son cuatro en el equipo: Ana como CEO, Martina como CTO y dos data scientists. Colaboran con un laboratorio de diagnósticos en Estados Unidos y están en conversaciones para llegar a Brasil.

"Queremos usar nuestra tecnología no solo para generar diagnósticos más rápidos y económicos, sino también para desarrollar nuevos diagnósticos que hoy no existen"

New NYT: CPI was super hot. But core was relatively tame. Two huge one-time factors raising inflation: tariffs & Iran. Fed can't solve them because they're not about excessive demand. Only Trump or time can solve.

Now the usual wonky thread I didn't have time for before.

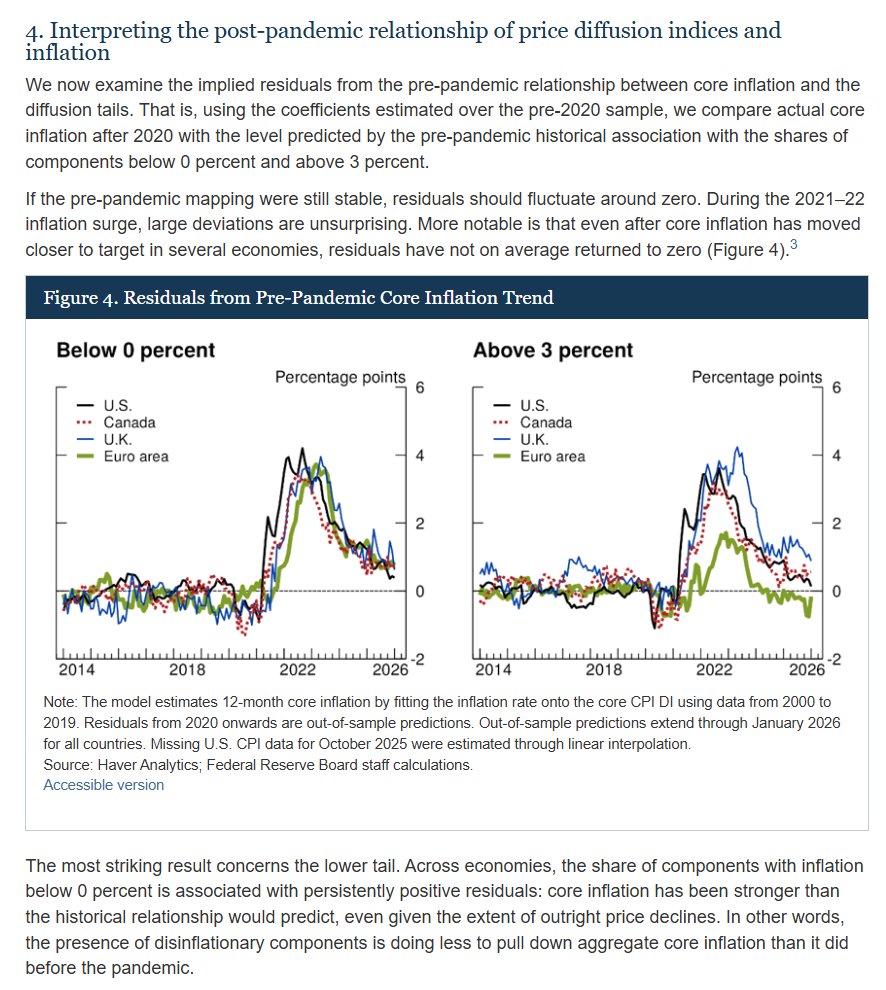

Fed research suggests the inflation engine may be running differently across advanced economies since the pandemic:

1/ More categories continue to see price growth above 3%, with broad-based wage growth in services appearing to be a key driver

2/ Even categories with flat or falling prices aren't pulling the overall number down the way they used to

3/ Pre-pandemic models consistently underpredict current inflation, suggesting the relationship between price dispersion and aggregate inflation may have shifted https://t.co/fjdQTsaV8e

Last week, I outlined questions I would be looking to have answered when the President’s budget is released. Now that we have the full proposal, we can now answer them.

Hint: It fails to offer affordability solutions to make life more affordable while raising the risk of hasty, harmful cuts.

The job market continues to be reasonably good (for an aging workforce with low net immigration).

178K jobs in March, much a bounceback from strikes and weather that resulted in -133K (revised) in February. The three month average is 68K.

Urate ticked down to 4.3%.

The job market continues to be reasonably good (for an aging workforce with low net immigration).

178K jobs in March, much a bounceback from strikes and weather that resulted in -133K (revised) in February. The three month average is 68K.

Urate ticked down to 4.3%.

[HILO 1/11]

🛑 El viernes prometí ofrecer mis opiniones sobre la decisión de la Corte de Apelaciones del Segundo Circuito en el caso YPF. Son varias opiniones y son diferentes a las ofrecidas por la mayoría de los foristas. Empiezo.

[THREAD 1/11]

🛑On Friday, I promised to share my views on the Second Circuit Court of Appeals’ decision in the YPF case. I have several—and they differ from those offered by most commentators. Let’s begin.

🛑Próximos pasos en el juicio por la expropiación de YPF:

1. Pedido de revisión a todos los jueces de la Corte de Apelaciones. A esto se le llama Hearing en banc. Aunque rara vez la totalidad de los jueces aceptan este pedido, este juicio es muy particular y tuvo una decisión 2-1. Si los jueces aceptan, el caso tomaría una dimensión excepcional frente a la justicia neoyorquina. Tiempo estimado de presentación: 14 días. Tiempo estimado de respuesta: otros 20 a 45 días.

2. Si el paso anterior falla, la alternativa que queda es la Corte Suprema. Los jueces supremos entran en receso el 31 de julio y regresan la primera semana de octubre. Si se presenta un pedido de revision (certiorari) antes de julio, probablemente tengamos una respuesta la Corte en diciembre. Si rechaza el caso, las vías legales en EEUU se habrán agotado. Si acepta revisar el caso, se espera una respuesta para julio 2027.

3. La alternativa paralela (que puede ser presentada sin necesidad de agotar los dos puntos anteriores) es ir al CIADI. El síndico concursal madrileño no abandonará sus responsabilidades de representar a los acreedores y de cumplir con el mandato de la Corte Mercantil N.3 de Madrid. La denuncia en el CIADI seguramente será presentada antes de lo previsto.

🛑Next steps in the YPF Expropriation Case:

1.Request for review by the full Court of Appeals (en banc hearing). While rarely granted, this case is unusual and was decided 2–1. If accepted, it would take on exceptional significance before the New York courts. Estimated timing: filing within 14 days; decision within 20–45 days.

2.If that fails, the next step is the U.S. Supreme Court. The Court recesses on July 31 and returns in early October. If a certiorari petition is filed before July, a response could come by December. If denied, all U.S. legal avenues are exhausted. If granted, a decision would likely be expected by July 2027.

3.Parallel path: ICSID. This route can be pursued without exhausting the previous steps. The Madrid-based insolvency trustee will continue representing creditors and complying with the mandate of Commercial Court No. 3. An ICSID filing will likely come sooner than expected.

Petrodollars! Nothing produces more heated discussion and, in my experience, less insight. Myths trump facts, because the actual data is a bit obscure --

But here is the most important thing to know. Before the Hormuz crisis, the flow of petrodollars had more or less dried up

1/many

My two posts on AI in academia got over a million views and a thousand angry responses. I got a few things wrong. I stand by the rest. But most people reacted to the headline, not the arguments.

So here are all 20 theses laid out. Tell me which ones you actually disagree with 🧵

Jobs report uniformly weak: 92K jobs lost (with job losses in almost every industry), household survey employment down too, unemployment rate up to 4.4%, participation down, avg weekly hours flat.

Main sign in the other direction was strong wage growth.

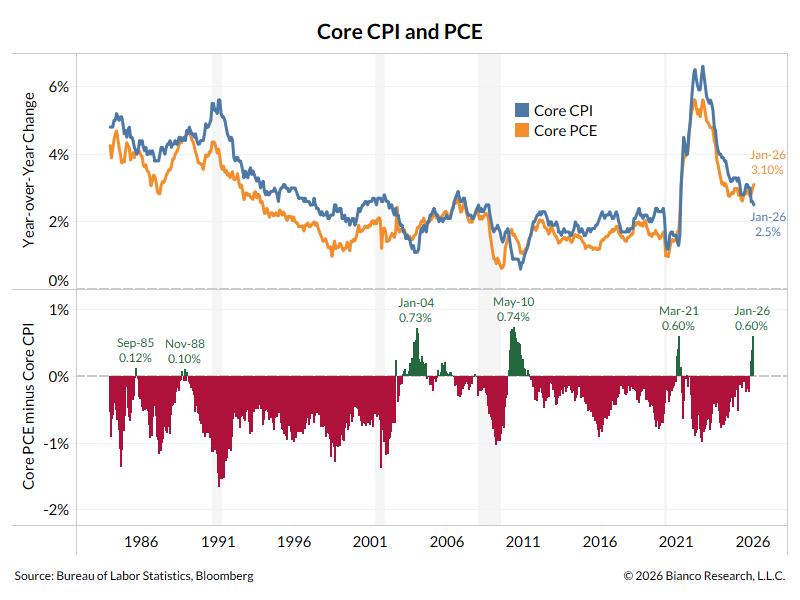

Once CPI and PPI are released, the street is VERY ACCURATE at taking that raw data and re-weighting it for PCE.

PCE uses the same raw inputs as CPI and PPI (some PPI categories are included in PCE), but with different weightings.

I plugged in 3.1% for January YoY core PCE into the chart below (from the table in the repost), and it shows YoY core PCE is now running 0.6% ABOVE YoY Core CPI. It is very close to a 40+ year extreme.

---

The joke for decades was that the Fed preferred PCE over CPI simply because PCE was typically a lower inflation measure (red bars, bottom panel). The only time this spread flipped to positive (green bars, bottom panel) was in the aftermath of a recession, which was attributed to distortions from the previous recession.

Now this spread is flipping again, meaning the Feds' preferred inflation measure is getting WORSE relative to the public's preferred inflation measure (CPI).

---

This is why the Fed is adamant about not cutting rates anytime soon. The measure they watch is going north, as the measure the public watches is going south.

Question? Does the Fed now abandon decades of precedent with its PCE inflation target of 2% because it has become inconvenient?

It would not be the first time they have done this, especially around inflation measures (see how quickly the Fed abandoned the University of Michigan inflation expectations measures the second they became inconvenient with high readings).

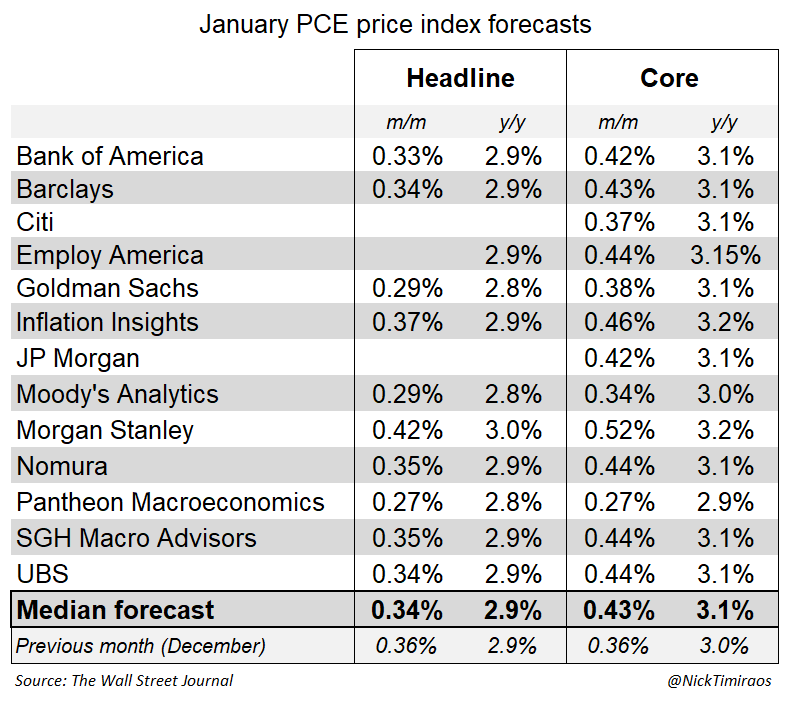

CPI and PPI translations into PCE suggest core prices in January rose around 0.43%, give or take.

That would be the highest month-over-month reading since February (which was +0.448%) and annualizes to 5.3%.

It corresponds to a 3.1% y/y rate, the highest since March 2024.

Why does Fed target PCE instead of CPI? My pet explanation. Monetary policy controls the growth of nominal (money) demand. Inflation is the difference between money demand and the volume of goods and services, i.e. nominal PCE divided by real PCE. This inflation must measure all the goods and services consumed by households even if they didn't pay for them. Suppose the cost of health care goes up 10%, but the government pays providers a subsidy to absorb half that. The CPI, a cost of living index, would correctly record a 5% increase in what consumers pay for health care. But this would understate true inflation, and the Fed would be misled by following CPI instead of PCE. PCE's odd imputations , for non profit services, financial services, etc. are designed to capture everything consumers consume regardless of the price they pay or whether there's even a price. It's not perfect (uses same awkward measure of shelter as CPI) and throws some head fakes. It is less comprehensive than the GDP deflator. Contra @biancoresearch this is why the Fed targets PCE instead of CPI, not because it's lower. At least it ought to be why. The Fed usually advances a different reason (usually about PCE chain weighting being better than CPI fixed weights). But I like mine more.