Push Chain has successfully completed its security audit with @hackenclub.

By the numbers:

- Zero critical-severity findings were identified

- 300 hours of audit work

- 3 smart contracts and full chain audit completed

- $100,000 bug bounty launching soon

Introducing the Maple Transparency page - live protocol data, all reconciled with Dune.

Transparency isn't a feature of onchain capital - it's the entire point.

We're often asked for the same data from the Maple community: How big is each product? How much are people actually depositing? Is Maple making money?

Now you can verify everything, anytime: https://t.co/mygHBW4jhU

Next up: a full transparency hub with token metrics, product-level deep-dives, and proof of reserves.

One day, Kleros will become the indestructible decentralized Corpus Juris, directly serving AI Agents, DAOs, and TradFi cross-border contracts, while becoming the industry standard for Legal RM.

It’s a wrap!

In collaboration with the Centre for Socio-Legal Studies and the Department of Computer Science from the @UniofOxford, we co-hosted “Law in the Digital Age of Crowds and Code”.

The workshop brought together legal scholars, arbitration practitioners, computer scientists, and institutional designers to discuss the future of law in the era of algorithms.

We structured the afternoon around two conversations that rarely happen in the same room.

In the first panel, we discussed the legal implications of the rise of decentralised justice systems.

Traditional legal systems were built for physical courts, national jurisdictions, and usually slow-moving disputes. The digital age has rendered those assumptions unstable. Cross-border e-commerce, autonomous AI agents, and decentralised organisations are already the new normal, yet legal infrastructure hasn’t caught up.

Together with Florian Grisel (CNRS/Oxford) and Nicole Stremlau (Oxford), and moderated by Fernanda Pirie (Oxford), we explored how decentralised dispute resolution systems interact with (and challenge) existing legal institutions, and what the transformation of international arbitration looks like in this new context.

In the second panel, we went deep into mechanism design.

With our Research Director @williamhwgeorge and @robertgdean (Diales and Kleros Supervisory Board), we discussed the architectural frontiers of decentralised justice: better jury selection models, more sophisticated incentive design, and above all the integration of AI into decentralised adjudication.

At the core of this work is the transition to second-generation decentralised justice systems, protocols with significantly more robust identity mechanisms, better jury selection frameworks, and architectures built for mass adoption.

It was a memorable afternoon with a convergence of arbitration practitioners, philosophers of law, game theorists, legal anthropologists, and cryptographers, all working on the same problem from different angles.

The questions raised in that room about fairness, automation, the rule of law, and the limits of algorithmic governance are no longer theoretical. They are live.

Many thanks to Fernanda Pirie, the Centre for Socio-Legal Studies and @KebleOxford for hosting this conference with us!

Recording coming soon!

On June 11, I will be presenting @Kleros_io with @williamhwgeorge at the University of Edinburgh! 🏴

Algorithms, incentives, and the justice infrastructure for the age of AI agents.

Scottish Enlightenment vibes.

Sign up here! 👇

https://t.co/93b3FnS17Z

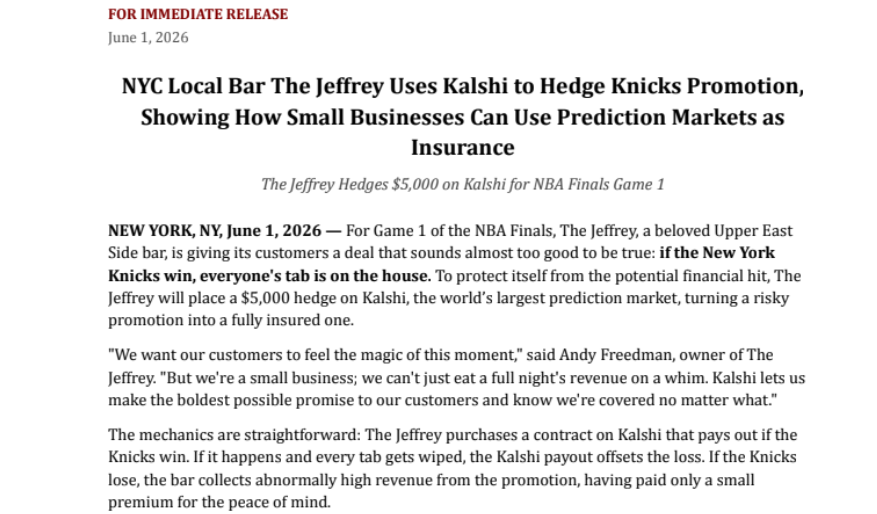

Kalshi's first example of a small business using it as hedging tool is The Jeffrey, an NYC bar that's promising free drinks to all customers if New York Knicks wins NBA Finals Game 1 on Wednesday

Vitalik Buterin on why consortium blockchains have mostly failed

“The original vision of consortium blockchains — the idea that you have 5 banks or major companies that come together and create their own chain — has been mostly a failure. I think the reason why is it ends up inheriting most of the disadvantages of centralization and most of the disadvantages of decentralization at the same time.”

“The first five banks join, and they all feel like ‘Yay, we’re building a system together. We can all be part of it.’ But then once bank #6 and bank #7 and bank #29 come in, they’re joining a system where there’s already an established power structure, established participants, and basically to them it still feels like they’re joining some kind of centralized thing that’s controlled by a cartel.”

“You don’t actually gain the benefits of true openness that people are looking for. You don’t have Etherscan. You don’t have a connection to an open, public network. At the same time, if you build on one of those systems, you have to figure out how to program distributed systems; you lose privacy — you might think you still have some, but the reality is you’re putting your data on a network where the only people that get to see it are you and all your closest competitors. From a privacy perspective, it actually doesn’t make much sense.”

“The compromise between centralization and decentralization that actually makes a lot more sense is: you have an application and today that application is a server. You can keep your server, but instead, we’re going to add scaffolding on top to give users extra security guarantees. You put Merkle roots on chain. You put proofs on chain. And you give your users assurance that whatever is happening inside of your system is actually following the rules. So you have high scale, high performance, and you optimize for a minimal delta for existing centralized infrastructure deployment. Keep your existing infrastructure the way it is, and you just add a side car that makes the roots and the proofs.”

Source: @arbitrum

@hoffmang@macky025 Understood on the Americus Trust precedent. 🙏

Any update on when Permuto plans to file the formal '40 Act registration forms (N-2 or S-6)? Their latest filings are still S-1 amendments from mid-2025.

For listed companies, they will no longer be dealing with a single shareholder. Instead, they will have to manage a dispersed group of DC and AC holders, with the Trust acting as the voting proxy. This will significantly complicate shareholder communication, dividend tracking, and decision-making on major matters.

Technically, it is indeed possible not to involve the issuer at all, but this is precisely the fundamental reason why Permuto has still not received approval to this day — it simply shifts the issuer-side problems onto the regulator and the market, rather than truly resolving the governance conflicts. The SEC is currently putting the brakes on this kind of “no issuer endorsement” innovation.

For listed companies, Permuto’s product structure (splitting shares into separate Dividend and Asset Certificates) would create major complications. It leads to confusion in shareholder communication, dividend management, and voting rights. In effect, this forms “two separate stock markets” for the same underlying company shares.

Today we’re launching an alpha/playground version of statistical volatility perpetuals with leverage. Try it out at https://t.co/zqswY63SAd. We will run this in this mode for a week or two to let folks get up to speed on how to trade in it and how to make markets in it