In my 4 years in crypto, I witness 3 major bottom so far. 3k in 2020, 15k I'm 2022 and 49k in 2024. Every cycle, the previous bottom never revisited again. I think #BTC will never touch 49k again. We are going to 150k in 4th quarter of 2025.

The country is in a very dire situation politically and economically. As if there is no ending to the suffering of the ordinary Filipinos. Is there any reason to be hopeful for the country to be better?

My column today: There must be no sacred cows, not his cousin, not his son, not his political allies. Regaining confidence is the most important objective BBM must have now. Otherwise, his public trust ratings will fall further in negative territory. https://t.co/RbjZcPxel3

More food for thought. A short one for your weekend reading list…

This is from the August 27th MIT report:

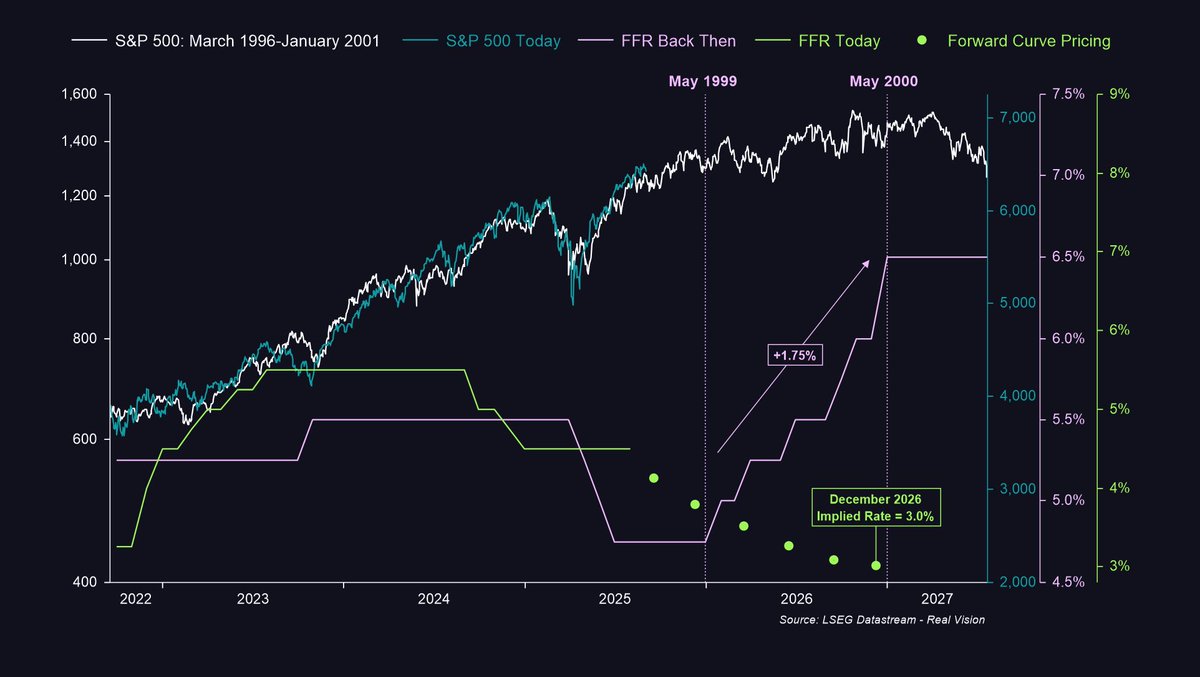

The last chart I want to leave you with this week is this one…

As you know, we were one of the very few who were contrarian at the lows, citing this chart (excluding the Fed Funds Rate) as one of several we used to build the case for a sharp V-shape recovery in equity prices following our Urgent Flash Update back in April.

Now, here’s the thing I want us to think about next...

Starting in May of 1999, the Fed turned hawkish and hiked rates by 175bps (1.75%).

Today, according to the forward curve, we are looking at the opposite situation.

Into year-end 2026, the market currently expects the Fed to ease by 150bps (1.5%), with around two cuts priced in this side of the year and another three next year.

If that plays out, we would be in a completely different environment from 1999.

Back then, equities ground higher into the September 2000 peak while the Fed was hiking rates and draining liquidity.

This time, we could have the Fed cutting rates and adding liquidity. Two very different scenarios.

That’s why I believe the odds point to next year being another strong year for risk-taking, even though almost nobody is talking about the cycle extending beyond this year.

If this turns out to be right, 2026 would be 1999/2000 on steroids.

We still have another three months or so to build the case, but to me this is incredibly interesting to think about. Let’s see…

Wanted to share a few thoughts tonight...

This is from the September 11th MIT publication that dropped on @RealVision:

For starters, unemployment keeps grinding higher, exactly as our lead indicators and GMI/MIT work flagged back in Q1.

That keeps the Fed engaged and is why, as I noted in last week’s video update, the market has started pricing in a higher probability of cuts at the September, October, and December meetings...

US unemployment is now at 4.3%, right on the Fed’s low estimate for 2025 (chart 1).

If it drifts toward 4.5% or 4.6%, as our lead indicators suggest, that’s a green light for more cuts into 2026, even though there are early signs the employment cycle has already turned up. More on that in a moment...

At the same time, unemployment breadth peaked over a year ago and continued to fall in August (chart 2).

Quantitatively, this is a good sign. The index rises into recession, it doesn’t fall…

We peaked last June at 92%, but it has since dropped to 62% of US states reporting a year-on-year rise in unemployment.

Now, take a look at this next chart...

This index tracks weekly overtime hours in the most cyclical parts of the US economy, with data back to the 1950s (chart 3).

Every recession has come when it rolls over toward the -2 standard deviation level, and we are nowhere near that.

Additionally, the August data showed a further pick-up in overtime hours, which, as I have been highlighting in these reports, is much more consistent with an early-cycle economy trying to build momentum than anything else...

This is exactly why S&P earnings revisions keep exploding higher, just as we’ve been expecting (chart 4).

The Fed is cutting rates right as the business cycle is turning up. That’s hugely bullish for risk assets.

These aren’t late-cycle recession cuts. They’re early-cycle insurance cuts... two very different things.

The end of The Waiting Room is near...

I’ve been seeing a lot of chatter on X about “peak cycle” and how the economy looks late-cycle. So I wanted to tackle this head on and share a few thoughts of my own...

This is from the August 21st MIT publication:

A classic late-cycle economy typically has all the following ingredients:

✅ Manufacturing sentiment is extreme (think ISM ~60)

✅ Services sentiment is extreme

✅ Homebuilder sentiment is extreme

✅ Consumer confidence is high

✅ Worker confidence is high (JOLTS quits rate rising sharply)

✅ Investor sentiment is very bullish

✅ Small business confidence is high

✅ Job openings and hiring plans are rising

✅ Wage data and surveys show accelerating pay increases

✅ CEO confidence is strong and capex is booming

Now, I could add more to this, but when you score all of these inputs and turn them into a single timeseries, here’s what you get (chart 1).

Using data from ISM, NAHB, NFIB, BLS, AAII, The Conference Board, etc., US sentiment, when viewed as a complete picture, remains very subdued. We’re just not even close to the euphoric levels we see late in the business cycle, when everything listed above is stretched to extremes.

Peak cycle is when the ISM rolls over from 60+ to sub-50, inventories unwind, and demand cools. Supply and demand reset, inflation pressures ease, and the cycle eventually recovers out of the slowdown or recession – mostly depending on the extent to which financial conditions tightened during the cycle, particularly late on as central banks hike rates and drain liquidity.

However, based on this full set of indicators, the data is pointing to something very different. This does not look like an above-trend late-cycle economy. It looks much more like an early-cycle economy trying to build momentum.

Another really important factor, and a key reason we believe both the ISM and this sentiment composite will grind higher this year and into 2026, is the sheer scale of central bank easing via rate cuts.

Right now, nearly 90% of central banks are cutting rates. That is extraordinary, and on a forward-looking basis, it is a massive tailwind for the business cycle (chart 2).

By my playbook, the time to start talking late-cycle is when the teal line rolls over and begins to drop, as central banks turn to hiking rates to slow growth. Even then, there’s usually a nine-month lag before higher rates hit the real economy.

Right now, we’re just nowhere near that... in fact, the opposite is true.

To my earlier point, slowdown or recession is largely a function of how much financial conditions tighten late in the cycle. Oil prices are a big part of this equation. When oil runs 50% above trend, that represents a massive tightening and has almost always signaled recession, looking back to the early 1970s.

However, right now, we are nearly 20% below trend and still falling, which shows this component of financial conditions is still easing (chart 3).

Also, as I’ve pointed out many times in previous reports, when you look at Temporary Help Services, it has early-cycle vibes written all over it (chart 4).

Rising growth from deeply negative levels is an early-cycle dynamic. It tells you the economy is in recovery mode, not rolling over.

Late-cycle is the opposite: positive year-on-year growth that’s slowing, which reflects an overheated economy losing steam.

Why is unemployment still rising?

Because it lags the cycle. Jobs data is a six-month look in the rear-view mirror.

Here’s the thing: full-time hires are expensive. Benefits, pensions, overhead…

So what do businesses do first?

They typically increase overtime hours and bring in temp workers. Only when they feel confident do they finally lock in full-time staff. That way, they can scale without locking themselves into long-term payroll commitments.

So, this isn’t late-cycle. It’s early-cycle (growth up + inflation down = Macro Spring), soon transitioning to mid-cycle (growth up + inflation up = Macro Summer).

That’s how I see it, anyway...

I turn 44 today, and here's some honest, tough-love advice for people in their 20s.

1: If you have a comfortable job, you're doing it wrong.

2: Your designer degree from an overpriced university is overrated for 99.99% of career fields.

Actually, nadidisorient ako at namamangha every time na pinag-uusapan ang “obligasyon” sa magulang. We don’t use the word “obligation” when it comes to family. We take care of whoever needs it the most—just like they took care of us when we knew nothing about this world while growing up. Now it’s our turn as they slowly drift away. It’s the cycle of life. Family takes care of each other.

It even feels cringey to treat it like an issue or a responsibility. Looking after one another, in whatever way we can, is simply the nature of family. Whether we’re poor or wealthy, we share what we have—we take care of each other because that’s what family does.

Pag hindi kaya ng isa, pagtulung-tulungan ng lahat. Ang salat sa pera, magbigay ng oras; ang may pera, mag-share. Kung ano ang kaya, yun lang naman ang aasahan. Pag pare-pareho walang pera, eh ‘di sama-samang pagsaluhan kung anong meron. Wala pa ring iwanan. That’s what family is all about.

Pag may naka-angat, hilahin paakyat ang lahat. Ngayon, kung hindi ka lumaki sa sarili mong magulang, siguradong mag-iiba ang dynamics nito—at hindi ‘yun kataka-taka.

Ang alam ko sa Singapore, pag nag alaga ka ng magulang and they’re staying with you, may incentive ka or tax deduction from the government. If you live near your parents’ house or moved them closer to you, may incentive pa rin—though smaller. Ang ganda nun.

In my 4 years in crypto, I witness 3 major bottom so far. 3k in 2020, 15k I'm 2022 and 49k in 2024. Every cycle, the previous bottom never revisited again. I think #BTC will never touch 49k again. We are going to 150k in 4th quarter of 2025.

When asked about calls for him to run for national post in 2028, Pasig City Mayor Vico Sotto says:

“Hindi porke't pulitiko ay pataas ka nang pataas. Ayaw n’yo nga ng traditional politics, ayaw n’yo nga ng trapo di’ba? So dapat hindi laging ganun ang pag-iisip.”