The Clarity Act is competing for floor time against reconciliation, FISA, and more.

The window is open, but it won't be for long.

Contact your Senator today and ask them to make crypto legislation a priority.

What does the @dmgblockchain 50 MW LOI look like once contracts finalized. Assuming revenues of $1.75m per MW and EBITDA margin of 70% the deal could provide an additional $3.54 to the $DMGI.NE share price, using a multiple of 20!

The CLARITY Act will strengthen consumer protections, establish clear rules for digital assets, and provide U.S. law enforcement with powerful new tools to combat illicit finance and protect America's national security.

Proud to join @BlockchainAssn and more than 160 distinguished law enforcement and national security leaders in urging the Senate to pass the CLARITY Act.

1/ Today, we’re sending a letter to Senate Majority Leader Thune and Senate Democratic Leader Schumer signed by 160 former national security, intelligence, and law enforcement professionals in support of the Clarity Act.

https://t.co/1lSQkoaaXI

This small AI infrastructure company currently has a $49M market cap…. Book value over $109M, $DMGI

Working towards definitive agreements for their data center sites. Well worth the watch.

$HUT $IREN $SLNH $WULF

https://t.co/IgzMDpespW

If the United States doesn't establish the global standard for digital asset regulation, someone else will.

China is not waiting.

The Clarity Act is how America leads — and how we ensure our adversaries don't write the rules of the next financial era.

This is an odd clip. I find it hard to believe that the CEO of a major BBB could be this uninformed about a major piece of financial legislation.

The Clarity Act “doesn’t do anything for AML/BSA.” Really? Have you read Titles II or III?

“It allows them to effectively pay interest on deposits.” False. Section 404 explicitly prohibits digital asset companies from paying any form of interest or yield on a stablecoin balance in a manner that is “economically or functionally equivalent to the payment of interest or yield on an interest-bearing bank deposit.”

It is becoming increasingly clear that bank opposition to the Clarity Act is more about personality than policy.

Debate is healthy, but the facts on CLARITY aren’t debatable.

1 - On rewards: Section 404 addresses banks’ purported concerns by barring any digital asset service provider or their affiliate from paying rewards in a manner that is economically or functionally equivalent to the payment of yield on a bank deposit and more (e.g., captures direct and indirect arrangements, includes strict anti-evasion language and civil penalties, etc.). Crypto gave many real concessions here.

2 - On AML/BSA: CLARITY bolsters law enforcement’s authority / capacity to target bad actors and CIF with clear obligations for digital asset companies, coordinated info-sharing mechanisms, protections that close regulatory gaps, increased funding for FinCEN, and much more (see, e.g., sections 201-206, 301-313, 507, 508, 801, 903, etc.).

3 - On benefits to banks: CLARITY ensures banks may engage in a broad range of activities, including providing digital asset custodial services, operating a node, making loans collateralized by digital assets, providing self-custodial wallet software, and more (see § 401).

4 - On benefits to Americans: Crypto represents ~$3 trillion global market cap, but currently 88% of global trading volume occurs on non-U.S. exchanges and only 19% of crypto developers are located in the U.S. CLARITY will bring all this onshore, under U.S. regulatory oversight.

CLARITY has benefits that extend far beyond any one company or constituency. This is a bill for ALL Americans, including banks. CLARITY awaits. The time is now.

$IREN's >4000% AI growth in the coming 15 months with 5 new deals announced in the coming 6 months. The path to >$12B ARR and >$100 share price by 2027 👇

I believe the upcoming 6-9 months will be highly compelling for Iren, and I expect the stock to significantly outperform the broader market. This outlook is driven by numerous positive catalysts poised to push the share price upward, which I will outline below:

1. Exceptional AI Revenue Growth (>4000% over the next 15 months)

Over the next five quarters, Iren is projected to achieve triple-digit quarter-over-quarter (QoQ) growth, scaling revenue from $34 million to over $1.4 billion within this timeframe. According to calculations by @bitcoinbutcher1 , Iren is on track to reach an annual Recurring Revenue (ARR) exceeding $12 billion by the end of 2027. (check his post)

2. Anticipated Contract Announcements (5 deals in the next 6 months)

Over the next three months, I anticipate Iren will announce several contracts related to their 2027 capacity. Iren currently has an ARR of $4.4 billion, and over the next six months, I expect management to increase contracted ARR from the current $3.1 billion (as of May 29, 2026) to over $10 billion. This growth will be driven by multiple agreements utilizing their 2027 capacity. Below is an overview of these expected agreements:

Mackenzie (80MW):

Iren has purchased approximately 36,000 B300 NVIDIA GPUs, scheduled for delivery in the second half of 2026. This data center will begin generating cash flow for Iren within the year. While the GPUs have been procured, a formal customer announcement for this facility has not yet been made. Market speculation suggests these resources may be allocated to existing clients such as Fireworks AI or togetherAI. However, I am optimistic that Anthropic could secure this capacity, given that Mackenzie is likely one of the data centers offering the fastest time-to-compute. Industry observers are keenly aware that Anthropic is in urgent need of immediate capacity. I expect an agreement for Mackenzie to materialize in the coming months, which would subsequently boost the projected EOY 2026 ARR from $3.7 billion to $4 billion.

Canal Flats (30MW):

As Iren's smallest data center, Canal Flats is set to be retrofitted from Bitcoin mining to air-cooled AI capacity. Consequently, an announcement from Investor Relations regarding additional B300 purchases for this site is highly probable in the near term. This facility is expected to be operational by the first half of 2027, contributing an estimated ARR of over $300 million.

Horizon 5-6 (Liquid-Cooled, VR200):

In their Q1 report, Iren announced plans to build an additional 100MW of IT load utilizing liquid-cooled data centers. I suspect this capacity will be contracted to Microsoft, which is already a client for Horizon 1-4. The key differentiator is that Horizon 5 and 6 will be designed for NVIDIA's latest Vera Rubin models. Estimating the ARR contribution is difficult, as comparable contracts are not currently present in the market, but I anticipate this contract will be secured shortly. With Horizon 1-4 slated for completion by EOY 2026, it is logical to commence groundwork and expansion soon—a process significantly aided by having a committed client.

Childress 250MW (Air-Cooled, Retrofitted):

Iren also announced an additional 250MW of air-cooled capacity for Childress. This involves retrofitting existing Bitcoin data centers into air-cooled AI facilities. The strategic decision to prioritize air cooling is driven by the ability to offer faster time-to-compute, a critical focal point in today's market (again, highly relevant to companies like Anthropic). We already know that 60MW of this capacity is contracted to NVIDIA, leaving 190MW currently available. This remaining 190MW could contribute an additional $2.1 billion in ARR (calculated as $700 million ARR from the NVIDIA contract multiplied by 3).

Sweetwater (300MW to 1.4GW):

This facility has been designated as NVIDIA's "flagship deployment for NVIDIA's DSX architecture." An initial 300MW is scheduled for development in 2027, scaling up to a massive 1400MW data center over time. The immediate 300MW phase currently requires a committed contract. Iren has already completed significant groundwork for the site and secured grid connection approval in early May. This contract will involve NVIDIA's VR200 GPUs, likely making it the largest data center globally with a VR200 installation. This is the contract I am most anticipating due to its sheer scale, potentially exceeding $20 billion. While it is a long-shot, there is a possibility that the entire 1400MW could be leased to a single client. Such a scenario would imply a potential contract size of over $100 billion—a staggering figure considering Iren's current market capitalization of $22 billion.

3. Strategic Rerating: From Bitcoin Miner to Neocloud:

Despite being a strong proponent of Bitcoin myself, its current association does more harm than good for the company's valuation. Bitcoin is generally viewed unfavorably by Wall Street, resulting in the stock trading at significantly lower multiples compared to pure-play AI companies. As Iren transitions away from Bitcoin over the next 6-9 months, I expect the stock to undergo a significant rerating as the perceived risk associated with cryptocurrency is eliminated. This pivot will serve as a major positive catalyst; the company will shed its label as a mining operation and be formally recognized as a premier data center provider.

@JSeyff@SpaceX Want to front run the Spacex IPO? Small cap Neptune Digital (NPPTF) owns shares on its balance sheet. Not many are aware of this fact. Buy NPPTF before the SpaceX IPO.

👀👀👀 @IREN_Ltd Sweetwater — the scale of this site is hard to comprehend 👀👀👀

⚡ 2,000 MW total capacity across Sweetwater 1 and Sweetwater 2 — West Texas

⚡ 2,200 acres of total land area — one of the largest single AI infrastructure footprints in North America

⚡ Capable of supporting 700,000+ state-of-the-art liquid-cooled GPUs at full buildout

⚡ Three revenue pathways on a single campus — AI Cloud, Build-to-Suit, and Colocation — maximum commercial flexibility

⚡ Sweetwater 1 substation already energized ✅ — Sweetwater 2 advancing — backed by the $9.7B Microsoft and $3.4B NVIDIA contracts

Sweetwater alone could be worth more than $IREN 's entire current market cap if fully contracted at current lease rates... 🤯🤯🤯

The Purdue BOT voted to approve Mitch Daniels as interim president, effective July 1. “If the board believes that recalling me to active duty temporarily can help in this respect, no one as devoted to this institution as I am could say anything but yes.” https://t.co/o5Tm3aOCd6

💎 @BitDigital_BTBT is a Strategic Asset Company (SAC) built for long-duration relevance 💎

⚡ Ethereum Economic Infrastructure — 155K+ ETH staking and earning protocol-native yield — treating ETH as productive economic infrastructure, not passive inventory

⚡ AI/HPC Intelligence Infrastructure — majority equity ownership @WhiteFiber_ — scalable, energy-dense capacity for AI and HPC workloads

⚡ Capital allocation model — actively deploys capital across productive strategic assets, monetizing usage, yield and participation

Two foundational infrastructure themes — Ethereum settlement rails + AI compute — compounding inside one publicly traded vehicle

HAPPY 90th 🎂 Coach Keady! One of the Coaching G.O.A.T. !! Thanks for all you did for our Family - the Purdue 🏀 Family - and for changing the Life’s of so many along the way !!! 💛🖤

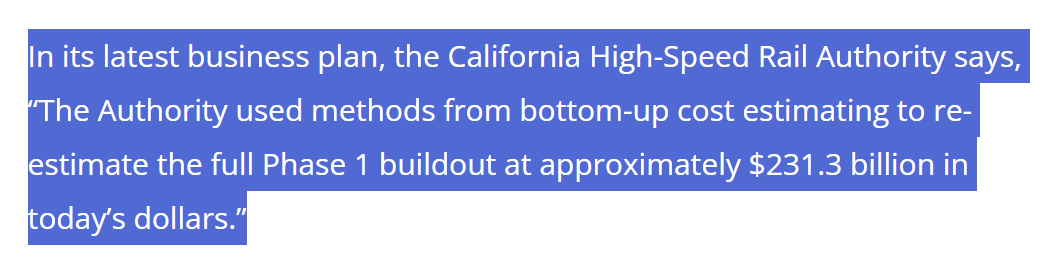

California high-speed rail cost now up to $231 billion. That means the average worker in the state will pay out over $12,000 to fund a single project that almost no one will ride.

CA rail will be studied for generations, a truly once-in-a-lifetime level of government failure.

𝐓𝐡𝐫𝐞𝐞 𝐋𝐚𝐲𝐞𝐫𝐬. 𝐎𝐧𝐞 𝐂𝐨𝐦𝐩𝐨𝐮𝐧𝐝𝐢𝐧𝐠 𝐀𝐝𝐯𝐚𝐧𝐭𝐚𝐠𝐞. 𝐓𝐡𝐞 𝐈𝐑𝐄𝐍 𝐓𝐡𝐞𝐬𝐢𝐬.

There's been a lot happening at IREN recently.

Expansion across North America, Europe and Asia-Pacific.

The NVIDIA partnership.

The Mirantis acquisition.

New GPU deployments.

New customer discussions.

A growing global footprint.

Underneath all of it is a fairly simple view of where the world is heading, and a deliberate strategy for how we position IREN within it.

That strategy is built on three layers. Together, they compound into a structural advantage that gets harder to replicate every quarter we execute.

Layer 1: Physical infrastructure. Power, land, substations, data centers, cooling. The foundation that everything else sits on.

Layer 2: Compute infrastructure. The GPUs, servers and networking that go inside those buildings. Deployed at scale. Generating revenue. Building execution track record.

Layer 3: Software and operational capability. The orchestration, deployment tooling and enterprise expertise that makes the first two layers work harder for customers, and opens the door to a broader, higher-value market over time.

Layers 1 and 2 are where the overwhelming majority of IREN's value is being created today. Layer 3 is where that advantage compounds further over time, but only because Layers 1 and 2 are built, owned and controlled at scale by IREN, not subscale nor contracted from a third party.

Think of Amazon. They didn't win e-commerce by building a great website. They won it by controlling the fulfilment infrastructure at a scale nobody else could replicate. The foundation you don't control becomes the ceiling on your business.

That is exactly how we think about IREN. The physical infrastructure - the land, the power, the substations, the data centers - is owned and controlled by us. The compute deployed into it generates the revenue and execution track record. And the software, orchestration and enterprise capability we are more methodically building on top is what turns the total product into a vertically integrated AI Cloud platform that compounds over time and deepens into a competitive moat.

AI is still early. The bottleneck is increasingly physical. And we have spent eight years building the foundations.