Few things I noticed:

@MoneyGram dropped MGUSD on @StellarOrg the other day, with their native stable baked right into the app. Moneygram has 60M+ customers with ~500k cash locations as per public sources. @Stablecoin + @m0 issuance infra.

@WesternUnion shipped USDPT on Solana a month ago . 150M customers, with ~500k cash locations as per their public source,they're not doing retail first. they're ripping out SWIFT for agent settlement. Issuance partner @Anchorage@deel just launched DLUSD with @Stablecoin as issuance partner - their native wallet for contractors to receive payroll. They have presence in 150+ countries(reportedly). Payroll going on-chain, out in the open. Even @GustoHQ adopted stablecoin payroll (via Zerohash) a few months ago.

If this isn't enough check @tempo partner's list: DoorDash, UBS, Klarna, Kalshi, Howard Hughes and more.Looks like nobody is sitting on the sidelines anymore and things are accelerating.

Pre-2025, stablecoins were basically a trading + DeFi native. Transfer funds into wallet, farm some yield, maybe move money across borders with limited on/offramp options. Now? payroll. remittance. treasury, card spend powered by real-world money plumbing. and the boring old use cases are the bullish ones.

looking back, 2026 will be remembered as the year stablecoins stopped being a crypto thing and become a part of real world commerce. Most banks haven't locked-in yet.

Why do we often learn about our own country's reserve movements from external institutions reporting that “India sold/bought X billion worth of gold”?

With the scale of technology we have today, would it really be difficult to build a transparent platform showing near real-time government reserves - gold, forex, and other major holdings?

Not questioning the decisions. Every country manages reserves strategically.

But shouldn't citizens have easier access to clear, official data rather than waiting for third-party reports?

Curious to know what others think.

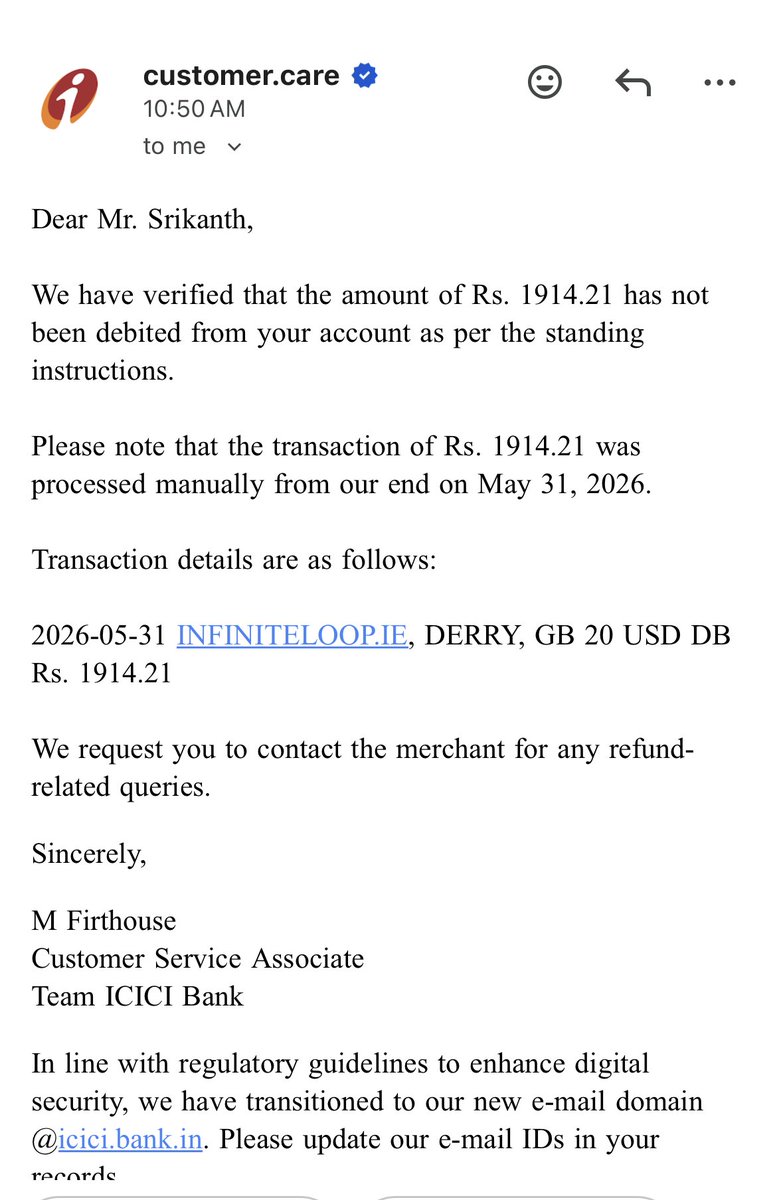

Finally received a disappointing response from @ICICIBank_Care@ICICIBank

A payment was manually processed on my credit card without my approval and without an active mandate.

Let that sink in.

If a mandate is cancelled, how can a bank still debit the amount from my card (manually)?

And instead of taking responsibility, I’m being asked to chase the merchant for a refund.

This is not about one transaction - this raises a serious concern:

👉 Can banks process payments from credit cards without customer consent?

Requesting urgent clarification and intervention from @RBI@RBIsays

Is this how autopay mandate cancellation is supposed to work @ICICIBank@ICICIBank_Care ?

I cancelled an #autopay mandate on my ICICI Credit Card on 27 May through their portal. Today (31 May), the payment was still deducted.

When I contacted #ICICI support, they confirmed that the mandate had been cancelled on their end. However, I was later told that the merchant had not cancelled it on their side, so the payment request was processed anyway.

What I don't understand is:

• If a mandate is cancelled through the bank's official platform, why is a merchant still able to initiate a debit against that mandate?

• If a payment request arrives after the mandate has been cancelled, why is it processed without any fresh authorization from the cardholder?

• What is the practical meaning of "mandate cancelled" if a debit can still go through afterward?

I'm attaching my conversation with customer support as proof. The conversation is a mix of Telugu and English, so it may not be understandable to everyone, but it clearly shows that ICICI acknowledged the mandate was cancelled and still explained that the payment was processed because the merchant had not cancelled it on their end.

Looking to understand whether this is expected behavior, a process gap, something that needs escalation or am i missing something. Has anyone faced a similar issue?

Requesting @RBI and @RBIsays to clarify: If a customer cancels an autopay mandate through the bank, should any subsequent debit request still be honored without fresh authorization?

Is this how autopay mandate cancellation is supposed to work @ICICIBank@ICICIBank_Care ?

I cancelled an #autopay mandate on my ICICI Credit Card on 27 May through their portal. Today (31 May), the payment was still deducted.

When I contacted #ICICI support, they confirmed that the mandate had been cancelled on their end. However, I was later told that the merchant had not cancelled it on their side, so the payment request was processed anyway.

What I don't understand is:

• If a mandate is cancelled through the bank's official platform, why is a merchant still able to initiate a debit against that mandate?

• If a payment request arrives after the mandate has been cancelled, why is it processed without any fresh authorization from the cardholder?

• What is the practical meaning of "mandate cancelled" if a debit can still go through afterward?

I'm attaching my conversation with customer support as proof. The conversation is a mix of Telugu and English, so it may not be understandable to everyone, but it clearly shows that ICICI acknowledged the mandate was cancelled and still explained that the payment was processed because the merchant had not cancelled it on their end.

Looking to understand whether this is expected behavior, a process gap, something that needs escalation or am i missing something. Has anyone faced a similar issue?

Requesting @RBI and @RBIsays to clarify: If a customer cancels an autopay mandate through the bank, should any subsequent debit request still be honored without fresh authorization?

Same happened with me.. and surprisingly there is no way to reach out to the support team.

Upon asking the driver he says talk to the support.

For the ride of 2043+300 collected 2643 (1000 ola money and 1643 UPI)

Personal note: Selling my OLA bag in the next market session.

Booked an Ola ride from Karjat to Prabhadevi. Final invoice already included Toll/Parking charges, and ₹1838 was charged via Ola Money.

But the driver still collected ₹350 cash separately for toll during the trip. This is unfair double charging and feels like fraud @olacabs

It is a trick being played since ages..

To cover pain create a bigger diversion that absorbs pain or makes it less important.

Bigger economy crash would seem smaller in global chaos

Grandpa still playing old tricks in west and fun part is, this trap is working 🙆#Greenland

@raghav_chadha sir, your vision is being envisioned by other countries.. Apke aawaz kahi aur suni jaari he 😅

Hopefully we bring tokenization in India too..

🚨 BREAKING: NYSE announces new tokenization platform.

Here's what they're building:

A completely new trading venue with:

• 24/7 operations (no market hours)

• Instant settlement (not T+1)

• Stablecoin-based funding (not bank wires)

• "Tokens natively issued as digital securities"

Not retrofitting the existing exchange.

Not adding blockchain to the back office.

An entirely new venue.

---

Think about what this means:

NYSE will run two exchanges.

The old one: 9:30-4:00 EST, T+1 settlement, bank wires.

The new one: 24/7, instant settlement, stablecoin rails.

They're not choosing between traditional and digital.

They're operating both in parallel.

---

How does this compare to others?

Everyone else is building infrastructure to tokenize existing assets:

• DTCC tokenizes existing custodied securities

• State Street tokenizes MMFs and ETFs

• Nasdaq amends rules for tokenized trading alongside traditional

NYSE is building a new way to bring equities on-chain AND the venue to trade them.

This puts them in competition with Figure's OPEN and Superstate.

Native digital issuance. Native digital trading.

---

Tokenized stocks enable a world where:

• Settlement happens on-chain

• Custody lives in wallets, not DTCC

• Trading never stops

• Capital formation happens in stablecoins

The question for every institution:

Are you digitizing your existing business or building the business that replaces it?

NYSE just answered: both.

---

#fintech #tokenization #infrastructure #digitalassets #stablecoins