Official Statement Regarding the Polymarket MicroStrategy Market

I have contacted multiple legal advisors, partners, and people familiar with crypto and prediction market disputes regarding the Polymarket market “MicroStrategy sells any Bitcoin by May 31, 2026?”

I accept that I took risk. My position was aggressive, and maybe I was greedy. But risk-taking does not change the facts, and it does not allow a platform to apply an unclear or unwritten rule after real money has already been placed.

The written rule said the market resolves YES if MicroStrategy sells any of its Bitcoin by the date in the title. It did not clearly say the sale had to be publicly disclosed by May 31, filed in an 8-K by May 31, or confirmed before the deadline. A sale date and a disclosure date are not the same thing.

If Polymarket intended this to be a disclosure-based market, the rule should have said so clearly. Ordinary users read “sells any Bitcoin by May 31” as an event-based condition, not a disclosure-timing condition. Any ambiguity was created by the market wording itself.

I purchased 49,695.76 YES shares for approximately 35,000 USDC. This is real money, and this issue deserves serious review. I will continue improving my legal materials, collecting evidence, and contacting relevant legal support. I will pursue this matter to the end through every available lawful channel.

I am not asking for special treatment. I am asking for the written rules to be respected, the facts to be addressed directly, and this market to be reviewed fairly.

Prediction markets only work when users can trust that words mean what they say.

@Polymarket@PolymarketHelp

Two weeks ago, I was offered over $40,000 per month to promote companies on X, with this “Zoomer” account acting as the middleman. Instead of taking the money and cashing in, I exposed the entire network to help make X a better place.

Nikita Beer didn’t thank me once. He literally gave $10,000 to the Chinese guy running that platform-manipulation network. And as a “reward” for exposing it, my ad revenue share was cut in half and my reach dropped by 90%.

I’m tired and speechless.

@CoWSwap@FaucisBeagles price impact of at least 100% sounds like you're buying something at 2x the price

is english not your native language or did you inhale too much defi hopium

@StaniKulechov another case of "PRICE IMPACT IS NOT SLIPPAGE HUR HUR HUR " retarded DeFi design that does nothing good to the user. hope you got your choice of language signed off by some lawyer to cover your ass

China knows exactly what this does. Their domestic version of TikTok caps kids under 14 at 40 minutes a day, locks access between 6am and 10pm, and swaps the entire feed to educational content. Science, history, museums.

The version they export to everyone else? Unlimited, unrestricted, pure dopamine on demand.

When kids in the US and China were asked what they wanted to be when they grew up, the number one answer in America was influencer. In China it was astronaut.

Macron calls this a cognitive war. Export what dulls young minds and keep what makes them intelligent for your own population.

This is the most effective weapon ever deployed against a generation’s ability to think.

Remember this scene in The Big Short?

Jamie Shipley and Charlie Geller have bet everything against the housing market.

They've been bleeding for months, wondering if they're wrong.

Then they flip on CNN and see it: New Century Financial - the second-largest subprime lender in America - has filed for bankruptcy.

"It's starting."

That was April 2, 2007. New Century wasn't the crisis. It was 1% of the problem. But it was the first domino.

4 months later, BNP Paribas froze 3 funds citing "complete evaporation of liquidity." 18 months after that, Lehman was dead.

I'd encourage you to watch that scene today. Because we JUST got our New Century moment in private credit:

Blue Owl Capital - $307 billion in assets under management - just permanently halted investor redemptions at its retail private credit fund, OBDC II.

Investors will NEVER AGAIN redeem shares from this fund.

On January 25th, I wrote that private credit was showing cracks at the exact moment Wall Street wanted to open it up to your 401(k).

3 weeks later, here we are.

The timeline follows a pattern anyone who's been around markets long enough recognizes:

Through the first 9 months of 2025, OBDC II investors withdrew $150 million - up 20% year over year.

Meanwhile, Blue Owl execs publicly assured investors there was "no meaningful pressure" on their asset base.

But there was. And they're now facing a federal class-action lawsuit for saying otherwise.

In November, they attempted a merger that would have forced OBDC II investors into a publicly traded fund trading at a 20% discount to NAV. Effectively confiscating a fifth of their capital.

Blue Owl's own CFO conceded investors "could take a potential haircut." The stock dropped 11% in 8 days. They killed the deal.

Now they've abandoned the pretense entirely. PERMANENT halt. Fire-selling $1.4 billion in loans across three funds.

Investors get roughly 30% of NAV back through quarterly distributions - on Blue Owl's schedule, not theirs.

One delightful detail:

Blue Owl's co-CEOs have pledged $1.9 billion of their OWN company shares as collateral for personal loans - proceeds used, in part, to acquire the Tampa Bay Lightning.

The stock is down 33% this year. That collateral has literally shed $260 million since January.

Founders leveraging company stock for hockey teams while retail investors queue up for their own money. Wall Street's version of noblesse oblige.

But here's what matters:

This isn't about Blue Owl.

Blue Owl is a symptom.

The disease is a $3.4 TRILLION private credit industry built on opacity, conflicts of interest, and the polite fiction that illiquid assets can offer liquid redemptions.

Morningstar DBRS reports the trailing default rate has risen to 4%, up from 2.8% a year ago.

Downgrades outpacing upgrades. Outlook negative. UBS warns defaults could reach 13% if AI disrupts the software companies making up 17% of BDC loan portfolios.

Payment-in-kind loans (where borrowers can't pay cash interest and simply pile it onto the debt) have surged past 11% of BDC income.

When your borrowers are paying you with IOUs, the word "income" deserves quotation marks.

And the government's response?

Open YOUR 401(k) to private credit.

Trump's executive order directed regulators to do exactly that.

They want to "democratize" an asset class whose flagship retail product just permanently locked investors out.

The KKRs. The Blackstones. The Apollos. Everyone loaded up on private credit is exposed.

When the tide goes out, you find out who's swimming naked.

In April 2007, New Century went bankrupt.

Most of the financial world shrugged. 17 months later, Lehman made the point impossible to ignore.

And Blue Owl permanently halted redemptions TODAY.

AVOID PRIVATE CREDIT

AVOID PRIVATE EQUITY

Because it's starting...

This is a great point.

When it comes to bubbles the path is not as simple as most would expect.

It takes deep disruption, progress and businesses cases before everyone is on board.

1996: -33%

1998: -39%

1999: -50%

Within 4 years of the top the world thought it was over at least 3 times.

And we are not talking about tech as a whole that got disrupted, we are talking about the internet sector that was supposed to be the new digital gold.

Same fears about disruption, same thoughts about cannibalization. Yet we went and went upwards.

What we would need to see to form the top.

1. Everyone going into AI and implementing agents

2. A massive amount of AI IPOs

3. Lower rates

4. Deflationary impulse shown through @truflation reflect in data

5. Text from family and taxi drivers talking

6. Massive pre revenue rounds, so called narrative plays

7. Talent war with massive checks

8. Massive market cap concentration

I’d say we have the last two at least but the rest is not given.

Will be interested to follow this. Agree the biggest funds have been slow to adapt to AI, not because they are complacent, but because there hasn't been a clear alpha signal from large language models (yet). LLMs are trained on a giant web scrape and can correctly complete quantitative tasks about 75% of the time..."unreliable world calculator" isn't necessarily a tool that has the big quant firms shaking in their boots, even though there are elements of the investment research process where LLMs can be highly useful.

Fwiw, large quant funds also generally capture small gross alphas (single digits) that they produce into impressive ROE with incredible amounts of leverage & intense focus on slippage, fed with massive computing & data budgets. That's a pretty hard incumbent to unseat if you are "two guys and a swarm of agents", but good luck! (makes the task of unseating Bloomberg look like child's play)

The much bigger opportunity is to help fundamental investors become more "quanty" by regaining some of the stacked alpha into the fundamental process that quants have eating for the last 10+ years. Building the "Iron Man" suit that becomes an AI Native operating system about both internal & external data (i.e. a swarm of agents can't walk the floor of a tradeshow or attend the JPM HC conference). No one has really done this yet, because it is an incredibly difficult, but incredibly high ROI task if done right.

$GOOG has $170b of OCF growing like 10-20% a year they can throw around at compute to force OAI to do giant fundraising every year which they can’t do forever.

Kinda smart to throw their weight around now tbh. Should probably max the fuck out of capex for like 3-4 years just to fuck the Twink.

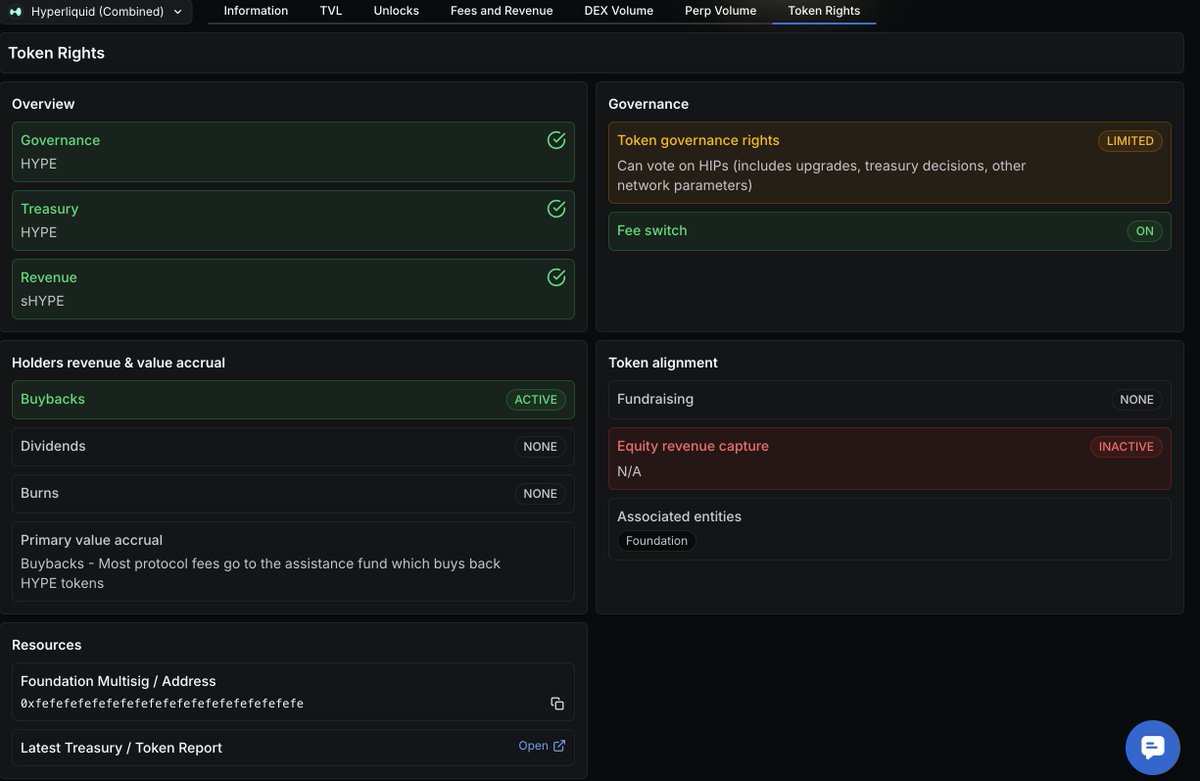

What does the token actually do?

This has been one of the most fundamental unanswered questions in DeFi since the beginning.

Does the token control governance?

Does it have any claim on the treasury?

Does it receive protocol revenue via buybacks or dividends?

Today, we launched Token Rights on DefiLlama.

Token Rights gives you a clear, standardized view of what a token entitles holders to: revenue, treasury, governance, or none of the above.

We’ve rolled this out across two dozen protocols, including additional context like historical governance discussions around token rights and whether teams raised equity separately from the token.