Former Defense Secretary and CIA Director Leon Panetta:

Trump walked away from our allies, threatening to leave NATO. Our allies do not trust United States right now. We don’t have experienced diplomats, and he hasn’t been willing to stand up to Putin and help Ukraine succeed.

Latest Tanker spot rates from Affinity.

Clean rates remain at or near historical highs.

Dirty remains at around $100K and higher.

$FRO $NAT $TEN $TRMD $BWET $STNG $TNK $DHT $INSW $ASC $ECO $HAFN

Last night was the biggest disaster in the history of Tesla.

Let me walk you through what actually happened on that earnings call, because the headlines are doing you a disservice:

Elon Musk got on the call and admitted (his words) that Hardware 3 "simply does not have the capability to achieve unsupervised FSD."

He said he wished it were otherwise. He said the memory bandwidth is one-eighth of what Hardware 4 has. And that's the end of the conversation.

Approximately 4 million Tesla vehicles on the road right now have Hardware 3. Many of those owners paid $8,000 to $15,000 for Full Self-Driving capability based on Musk's repeated promises (going back to 2016) that the hardware was sufficient for full autonomy. As recently as 2022, Musk was publicly assuring owners that HW3 had the processing power to get it done.

BUT IT DIDN'T

Those promises are now officially broken.

The solution is a "discounted trade-in" toward a new car with Hardware 4.

Not a refund or a free upgrade...

A discount on buying ANOTHER Tesla.

Investor Ross Gerber said it too - all HW3 owners got screwed, and with roughly 285,000 FSD purchasers affected, the potential liability runs into the BILLIONS.

But that's not even the worst part.

Musk was asked if the current FSD v14.3 was ready for unsupervised deployment. He said yes. Then immediately walked it back and admitted Tesla has "major architectural improvements" in the pipeline that would significantly improve safety.

What he really means: the software isn't SAFE ENOUGH to deploy without a human watching. Full unsupervised FSD for consumer cars is pushed to Q4 2026. At the earliest... Maybe.

How many times has this deadline been pushed? I've lost count. And trust me, I've seen a lot of broken promises. But this one takes the cake.

Now let's talk about the numbers everyone is celebrating:

Tesla reported $22.4 billion in revenue and $0.41 in non-GAAP earnings. A "double beat." The stock popped 4% after hours. Victory, right?

WRONG

Dig into the actual filing:

The number one driver of operating income improvement wasn't cost reductions, wasn't volume growth, wasn't FSD revenue. It was - and Tesla listed this FIRST in their own shareholder letter - "one-time benefits related to warranty and tariffs."

They released warranty reserves. They booked tariff refund windfalls. They stretched supplier payments by 10 days. They took on billions in new debt. Then they presented everything through non-GAAP metrics that strip out over $1 billion in stock-based compensation.

GAAP net income was $477 million on $22.4 billion in revenue. That's a 2.1% net margin. On a $1.4 trillion market cap.

Let me put that in perspective:

3.75 billion shares outstanding. Annualize the Q1 GAAP profit and you get roughly $1.9 billion. That's a trailing P/E ratio north of 700. Use the adjusted number - strip out stock comp, which is a REAL cost to shareholders through dilution - and you're still at around 250x earnings.

All of this is extremely bad, but I didn't even talk about the CAPEX BOMB yet...

3 months ago, Tesla guided to "over $20 billion" in 2026 capital expenditure. Last night they raised it to over $25 billion. A $5 billion increase in a single quarter. That's 3x their historical annual capex run rate - $8.5 billion in 2025, $11.3 billion in 2024. The CFO confirmed on the call that Tesla expects NEGATIVE free cash flow for the rest of the year.

So you have a company generating roughly $6 billion in annual free cash flow on a good year, and they're about to spend $25 billion.

The math doesn't work.

They will almost certainly need to issue equity. Which means dilution. Which means the $1.9 billion in annual earnings gets spread across even MORE shares.

The core auto business is literally deteriorating in real time:

Tesla delivered 358,000 vehicles in Q1 (missed estimates again).

They produced 408,000. That's 50,000 cars sitting on lots that nobody bought.

Inventory days jumped from 10 to 27 in just a few quarters. California (their most important US market) saw registrations crash 24% year over year.

Their market share in the state fell from 9.2% to 7.7%. That's on top of a Q1 2025 that was ALREADY weak from Model Y retooling. They're declining off a decline.

And here's what really kills the bull case...

The entire valuation rests on robotaxis, Optimus robots, and autonomy. So let's put numbers on it:

Waymo - the actual leader in autonomous driving with 15 million completed rides in 2025 alone, over 127 million autonomous miles driven, operating commercially across 6 US cities with plans to expand to 20 more - just raised $16 billion at a $126 billion valuation.

That's the market's verdict on what the LEADING robotaxi company is worth. $126 billion.

And Waymo is YEARS ahead of Tesla in actual deployment.

Tesla has 3.75 billion shares outstanding. So even if you assign $126 billion in robotaxi value (giving Tesla full credit for matching Waymo despite being nowhere close) that's $33 a share. Add the auto business at generous auto-industry multiples, maybe $20 a share. Throw in energy storage and services, $10-15.

Sum of the parts gets you to roughly $65-70 a share if you're feeling generous. Maybe $50 if you're not.

The stock is $387.

So what exactly are you paying for?

You're paying for a STORY. You're paying for PROMISES that keep getting pushed back, technology that keeps falling short, and a business plan that requires spending $25 billion a year while the core product sells fewer units at declining margins in a market where California sales just fell 24% and the federal EV tax credit is gone.

I managed the number one mutual fund in America. I founded two billion-dollar hedge funds. I've been doing this since 1981.

And I am telling you:

Tesla at $387 is one of the most egregious mispricings I have seen in my entire career.

THE CRASH WILL BE EPIC

Nasdaq is proposing to facilitate the largest involuntary wealth transfer from retirement savers to venture capitalists in market history. And nobody seems to be talking about it.

SpaceX demanded, as a condition for listing, that Nasdaq cut index inclusion seasoning from 3 months to 15 days. Nasdaq agreed (what?! where are the regulators?!) because losing a $1.5T listing fee to NYSE was unthinkable.

Over $600B in passive funds track the Nasdaq 100. These are 401(k)s, target-date retirement funds, index funds with capital auto-allocated from every paycheck by people who never make an active investment decision. When a stock enters the index, those funds MUST buy at weight. No analysis. No discretion. No opt-out.

The 3-month seasoning period exists so that price discovery, real buying and selling by people making actual decisions, can happen before that involuntary capital gets deployed. It's the one structural safeguard between a hyped IPO price and your retirement account.

SpaceX wants to IPO at $1.5T on a 3% float, get indexed in 15 days, and let insiders sell into the forced demand as lockups expire. The exit liquidity is your grandmother, scoolteacher, and lifesaver's 401(k).

I went through an IPO. I've been on the inside of the lockup and liquidation process. This is exactly how it works: insiders need buyers, and passive index capital is the largest pool of involuntary buyers on earth.

This isn't market innovation. It's manufacturing exit liquidity from people who don't know they're providing it.

https://t.co/B5WB3k3RXW

Former Trump White House attorney Ty Cobb blasts Trump’s “shameful” and “despicable” post about Robert Mueller’s death:

“He’s a demented narcissist. You know, seriously hates anybody who stands in opposition to him, has reworked the justice department into a revenge machine, and rules the country in a very authoritarian manner with the assistance of a cowardly cabinet and even more cowardly Republicans in Congress.”

BROWDER: We've seen Trump berate Zelenskyy in that awful Oval Office meeting with J.D. Vance, cut off U.S. military aid to Ukraine, and send emissaries to pressure Ukraine into giving up territory Russia hasn't even won.

Now Trump wants to hand Putin oil money. Ironically, this hurts India, Turkey, and China by forcing them to pay more for oil. It's a zero-sum game, and Putin gets the cash.

Middle East Conflict Readthrough: US land services, Canadian oil sands E&P and Brazil, Guyana deepwater E&P are early beneficiaries, with shallow water jackups most impacted (Middle East 35-40% demand) and a short-term negative, but long-term positive read on deepwater rigs #oott

(1) The Middle East accounts for 35–40% of global jackup demand, making shallow water the offshore segment most exposed to the current conflict. Saudi Arabia alone represents 13–17% of jackup demand, with the UAE, Qatar, and Kuwait adding materially to that figure. The Middle East is a low-cost production region that has historically supported jackup market stability, though subject to geopolitcal risk. Borr carries limited direct exposure with only three rigs in the region, but a prolonged conflict (not base case) that drives rig relocations could pressure dayrates across the jackup market, which appears unlikely thus far.

(2) Borr’s 10% 2028s (B3/B-) are still well-bid at 103 but down 1 ¾ pts. Borr enters 2H26 with 48% of its fleet open at a $139k average dayrate. Diversification across the GoM, West Africa, SE Asia and Europe should support utilization at current oil prices, though dayrates may depend on conflict duration and whether Mid East rigs are ultimately relocated (not expected)

Watch Item: Saudi Aramco has more influence over the jackup rig market than any other operator. It’s MSC-13 capacity expansion tightened the market in 2022–2023, only for Aramco to shed over 10% of global supply as prices weakened in 2024–2025. The program targeting ~700k bpd growth via Berri, Marjan, Zuluf and Safaniya was put on hold in Jan ‘24.

(3) US land services benefit from shale's short-cycle E&P capex, with natural exposure to the front end of the futures curve with >$30/bbl above 2028-2030 levels and geopolitical stability. Canadian oil sands E&P’s combine a low-decline production profile with minimal incremental capex requirements, generating strong free cash flow with low geopolitical risk.

(4) Deepwater's long-cycle nature limits its direct exposure to elevated spot oil prices. A small share of floater demand — roughly 2–3% — is tied to East Med projects in Israel and Cyprus, with some work expected for 2H26. Deferral into 2027 is a risk, though outright cancellation is unlikely given the geopolitical importance of the region’s gas supply (Egypt).

Longer-term, deepwater stands to benefit as energy security becomes a higher-order priority following the supply shocks of recent years. Large, import-dependent economies have strong incentives to develop domestic offshore resources with Turkey's successful Black Sea program, and India's deepwater ambitions having early-stage potential.

(5) SPR Releases are a Curve-Flattener: The futures curve is in steep backwardation, reflecting near-term supply disruption premiums. While the front end has risen sharply, coordinated SPR releases are designed to cap the move which likely results in a modest curve flattening. Longer-dated prices may find support, however, from future SPR refill demand.

Long-term futures in the low $70s for 2028–2030 remain sufficient to generate returns on greenfield deepwater developments, supporting FID potential.

Iran war imperils $300bn in Gulf AI spending. UAE and Saudi Arabia have been big investors in AI and major destinations for data centers. https://t.co/V7640CyKCt

Saudi Arabia is booking more and more super oil tankers at sky high rates (>$450,000 a day vs pre-war levels of $100,000 a day) to shift crude from the Red Sea into global markets.

This is the most SHAMELESS structural manipulation of a major index I've ever seen.

SpaceX is preparing what could be the largest IPO in history.

Target valuation: $1.75 trillion.

That would make it the sixth-largest company in America on day one.

And Nasdaq wants the listing so badly they're literally CHANGING how the Nasdaq-100 works.

In February, Nasdaq published a "consultation" proposing sweeping changes to how companies enter the index. The timing is pure coincidence, of course.

Just like it's pure coincidence that SpaceX has reportedly made fast index inclusion a CONDITION of listing on Nasdaq.

Here's what they're proposing:

A new "Fast Entry" rule would let any newly listed company whose market cap ranks in the top 40 of current Nasdaq-100 members get added to the index after just 15 trading days.

No seasoning period. No liquidity requirements. Completely exempt from the standards every other company had to meet.

Currently, new public companies typically wait up to a year before they're eligible for major index inclusion.

That waiting period exists for a reason. It lets the market establish real price discovery. It protects passive investors from being forced into untested, illiquid stocks.

And Nasdaq wants to throw all of that out. For ONE listing.

But the Fast Entry rule isn't even the worst part...

The real scandal is the 5x float multiplier.

Right now, the S&P 500 uses a free-float adjusted methodology. If only 5% of a company's shares are available for public trading, the index weights you at 5% of total market cap.

That's common sense. You weight a company based on what investors can actually buy.

Nasdaq's current methodology already uses total market cap rather than free-float for weighting. But for very low-float stocks, they at least had a 10% minimum float threshold.

Under the new proposal, that threshold DISAPPEARS entirely.

Instead, any stock with less than 20% free float gets weighted at FIVE TIMES its actual float percentage, capped at 100%.

Do the math on SpaceX:

If SpaceX IPOs at $1.75 trillion and floats 5% of its shares, there would be roughly $87.5 billion worth of stock available for public trading.

Under Nasdaq's proposed 5x multiplier, the index would weight SpaceX at 25% of its total market cap. That means passive funds would be forced to buy as if SpaceX were a $437.5 billion company.

But only $87.5 billion of stock actually exists in the market.

You are forcing hundreds of billions in passive buying into a $87.5 billion float.

QQQ alone manages nearly $400 billion. The total Nasdaq-100 ecosystem represents over $1.4 trillion in exposure across ETFs, mutual funds, structured notes, and derivatives.

Every single passive vehicle tracking this index would be REQUIRED to buy SpaceX at whatever price the market dictates.

On Day 15.

With zero price discovery. Zero track record as a public company. And a float so thin you could read through it.

So what this actually does is it creates a structural wealth transfer mechanism.

The passive bid from index funds pushes the stock price higher. That higher price benefits exactly one group of people: the insiders and early investors who own the other 95% of the shares.

And when lock-up periods expire 90 to 180 days later? Those insiders sell into the artificially inflated passive bid. Your 401(k) is the exit liquidity.

This is the fundamental corruption of indexing.

Indexing used to be brilliant. Low cost. Efficient. You were free-riding on the price discovery done by active managers. The index reflected the market.

Now the index IS the market. Trillions of dollars flow blindly into whatever the index tells them to buy. And the people who control the index methodology are changing the rules to serve the interests of a single IPO candidate.

The S&P 500 requires companies to have at least 50% of shares available for public trading. It requires 6 to 12 months of seasoning. It uses free-float adjusted weighting so passive investors aren't buying phantom liquidity.

Nasdaq is doing the exact opposite. 15 days. No float requirement. 5x multiplier on insider-held shares.

Every passive investor in QQQ, QQQM, and every fund benchmarked to the Nasdaq-100 should understand what's about to happen:

The rules are being rewritten to benefit IPO issuers and early-stage insiders, and your capital is the tool being USED to enrich them.

45 years in this business and I've watched Wall Street find creative new ways to separate retail investors from their money in every cycle. But usually they at least try to be subtle about it.

This one they put in a PDF and called it a "consultation."

What's your take?

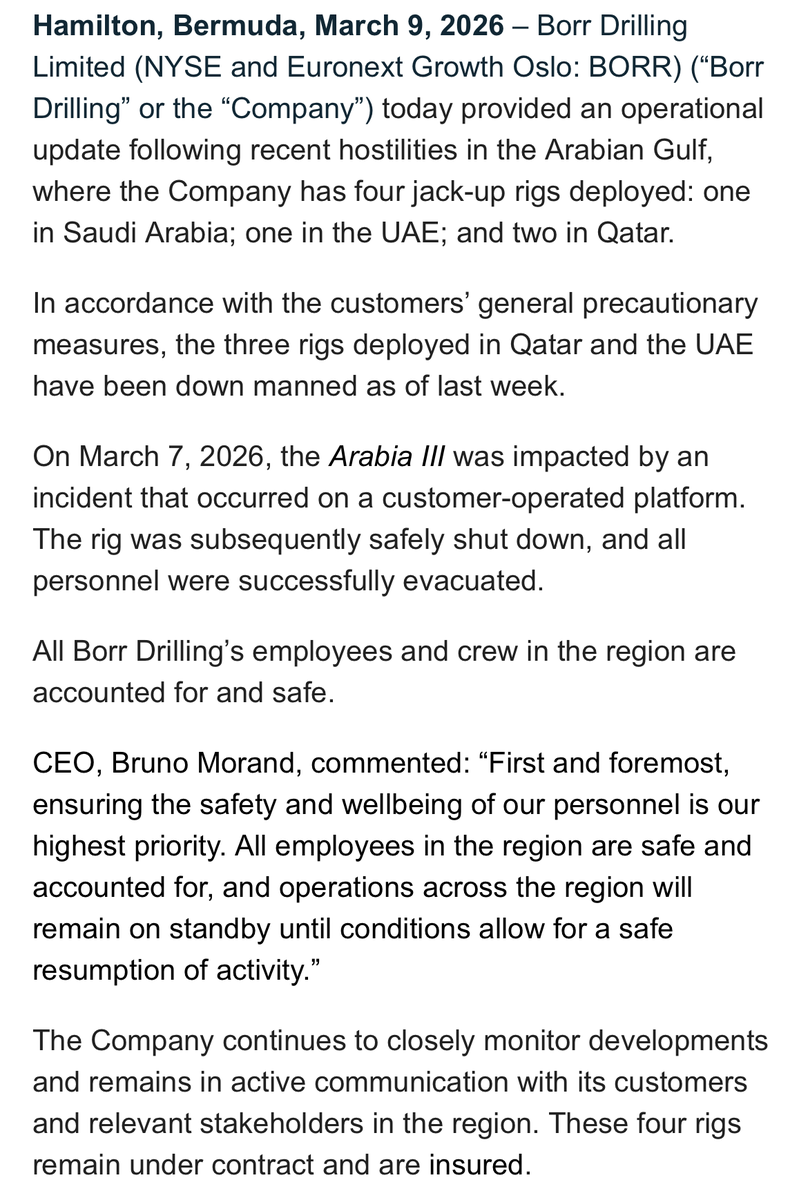

$BORR check:

1. 4 out of 29 rigs in a war zone safely preserved: quality premium pays off

2. Only truly international player to overly benefit from sky rocketing Demand for Jackups outside of conflict

Expect all time high rates soon as customers scramble for energy security