🤝Banks, NBFCs, and fintechs can now co-lend to deliver affordable credit beyond priority sector loans. Read our latest blog to learn more about the draft RBI co-lending regulation 👉 https://t.co/7RkmzgOy4c

🤔 𝐖𝐡𝐲 𝐰𝐚𝐬 𝐭𝐡𝐢𝐬 𝐫𝐞𝐠𝐮𝐥𝐚𝐭𝐢𝐨𝐧 𝐧𝐞𝐞𝐝𝐞𝐝?

▪️ Current regulations allowed limited players

▪️ Co-lending has evolved beyond priority sector to personal and consumption loans

▪️ Need for affordable interest rates for underserved segments

The big challenge? Balancing robust fraud defenses with a seamless borrower experience. If you work in digital lending, how do you navigate this? We'd love to hear your thoughts!

#DigitalLending#FraudDetection#FinTech#Innovation

Fraud in digital lending isn't just about lost money—it erodes trust and slows innovation. How are lenders staying ahead of evolving fraud tactics? 🛡️

Dive into our blog to explore the strategies shaping the future of fraud prevention: https://t.co/LigSFsT67G

💡Fraud in Digital Lending: Mapping the Risks Lenders Face

India reported ₹11,000+ crore in cyber fraud losses in the first 9 months of 2024. 📈

While illegal loan apps dominate headlines, the lender’s perspective is rarely explored. 🧵

🔗Read our latest blog on this:

🔍This blog dives into how fraud emerges and its real impact on lenders and borrowers.

🔜 Stay tuned for Part 2, where we explore detection & mitigation strategies to sustain trust in digital lending.

💡 As part of the D91 Labs Inner Circle, Devyani Parameshwar and @raghavb from Mera Kal explore how leveraging life insurance can unlock affordable credit for underserved households. 👉 https://t.co/XFWhqTOTDm

With 400 million active policies, life insurance is a trusted but underutilized asset. Instead of being surrendered at a loss, these policies can be leveraged as scalable credit solutions, enabling liquidity and building credit profiles.

Our parent fintech, @Setu_API , has 𝐢𝐧𝐭𝐞𝐠𝐫𝐚𝐭𝐞𝐝 𝐍𝐏𝐒 𝐜𝐨𝐧𝐭𝐫𝐢𝐛𝐮𝐭𝐢𝐨𝐧𝐬 𝐢𝐧𝐭𝐨 𝐁𝐡𝐚𝐫𝐚𝐭 𝐂𝐨𝐧𝐧𝐞𝐜𝐭.

Curious to learn more? Check out Setu’s blog for details. -

https://t.co/aVKzEfKpUc

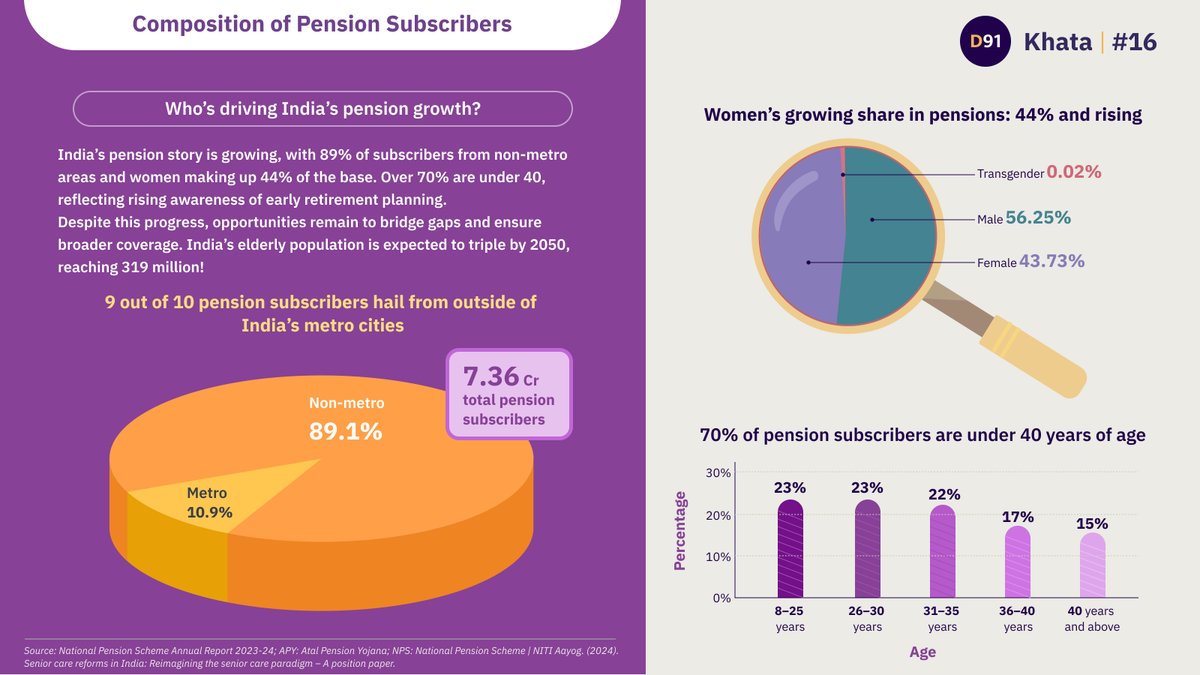

With 𝐈𝐧𝐝𝐢𝐚’𝐬 𝐞𝐥𝐝𝐞𝐫𝐥𝐲 𝐩𝐨𝐩𝐮𝐥𝐚𝐭𝐢𝐨𝐧 𝐩𝐫𝐨𝐣𝐞𝐜𝐭𝐞𝐝 𝐭𝐨 𝐭𝐫𝐢𝐩𝐥𝐞 𝐭𝐨 319 𝐦𝐢𝐥𝐥𝐢𝐨𝐧 𝐛𝐲 2050, the need for a robust pension ecosystem is more urgent than ever. This requires focused efforts on financial literacy, access, and better product design.