Dabbled with some exposure (never traded options on margin or uncovered but did today). Sold $SPCX call for 7/17, $380 strike, $630 in premium if it expires worthless.

Dabbled with some exposure (never traded options on margin or uncovered but did today). Sold $SPCX call for 7/17, $380 strike, $630 in premium if it expires worthless.

@BoBbyPleWniaK Insane trade - it is partially lucky that the stock ran so much and is so volatile to help those call premiums, but a great strategy. Getting the shares for effectively $60 a share is nuts. Between that and selling puts, you’re acquiring free shares

I strongly believe $LMND has the potential to become a long-term 10x.

Here is the actual 10x math:

$LMND currently has a market cap of roughly 4.4B.

A 10x would value the company at approximately:

$4.4B × 10 = $44B

With approximately 76M diluted shares, that would translate to roughly:

$44B ÷ 76M shares = $579 per share

Dilution could lower the eventual per-share result, but that is the general target required for a 10x from today’s valuation.

So how could $LMND ever justify a $40B–$45B valuation?

Start with the operating momentum.

In Q1 2026:

- Revenue reached $258M, up 71% YoY

- Gross profit reached $100M, up 159%

- In-force premium reached $1.33B, up 32%

- Customers reached 3.14M, up 23%

- Gross loss ratio improved from 78% to 62%

- Adjusted EBITDA loss narrowed from $47M to $17M

- Net loss improved from $62M to $36M

Revenue is growing much faster than operating expenses, which increased only 25%. That is the operating leverage investors have been waiting to see.

$LMND now expects approximately $1.2B in 2026 revenue and $1.63B–$1.64B in year-end in-force premium, while targeting positive adjusted EBITDA during Q4 2026.

But the long-term opportunity is much larger.

Management has laid out an ambition to eventually reach approximately $10B in premium volume.

Growing from $1.33B of IFP to $10B would mean increasing the insurance book by roughly:

$10B ÷ $1.33B = 7.5x

At 25% annual growth, that would take approximately nine years.

At 30% annual growth, it would take approximately seven years.

That is aggressive, but $LMND IFP is currently growing above 30%, and the company is still small relative to the overall homeowners, renters, pet and auto insurance markets.

Now assume $LMND eventually produces $7B–$8B in annual revenue from that larger premium base.

At a mature adjusted EBITDA margin of 12%–15%, it could generate:

$7B × 12% = $840M EBITDA

$8B × 15% = $1.2B EBITDA

Apply a premium 35x–40x multiple to a profitable insurance platform still growing faster than traditional insurers:

$840M × 35 = $29.4B

$1.2B × 40 = $48B

That produces a potential valuation range of approximately $30B–$48B.

The upper end is around the level required for a 10x.

This is where AI matters.

$LMND is not simply adding a chatbot to a traditional insurer. Its technology is integrated throughout the operating model:

- AI helps determine which customers to target

- Pricing models improve as more claims and behaviour data enter the system

- Automated claims reduce the cost of servicing smaller, frequent claims

- Direct distribution removes much of the traditional broker infrastructure

- Automation allows premium volume to grow without headcount increasing at the same rate

$LMND recently reached approximately $1M of IFP per employee, nearly tripling that figure over four years. Management has also maintained roughly a 3:1 lifetime-value-to-customer-acquisition-cost ratio, even while aggressively increasing growth spending.

That is the structural advantage.

More customers create more data.

More data can improve pricing and risk selection.

Better underwriting lowers loss ratios.

Lower loss ratios expand gross profit.

Automation allows that gross profit to scale without expenses increasing proportionally.

The 10x thesis is therefore not “AI hype.”

It requires Lemonade to:

- Continue compounding IFP around 25%–30%

- Keep its loss ratio near the low-to-mid 60% range

- Reach and sustain EBITDA profitability

- Scale Car without destroying underwriting discipline

- Control customer-acquisition costs

- Limit dilution

- Eventually approach $7B–$8B in revenue and approximately $1B in EBITDA

The path is now visible.

Just launched LTV13, our most capable prediction model ever.

Version 13 sharpens Car prediction specifically, giving our systems a much clearer view into the future: with higher resolution down to the individual policy, and up to 57% better precision than the previous model.

Look, I’m going to make it simple for you:

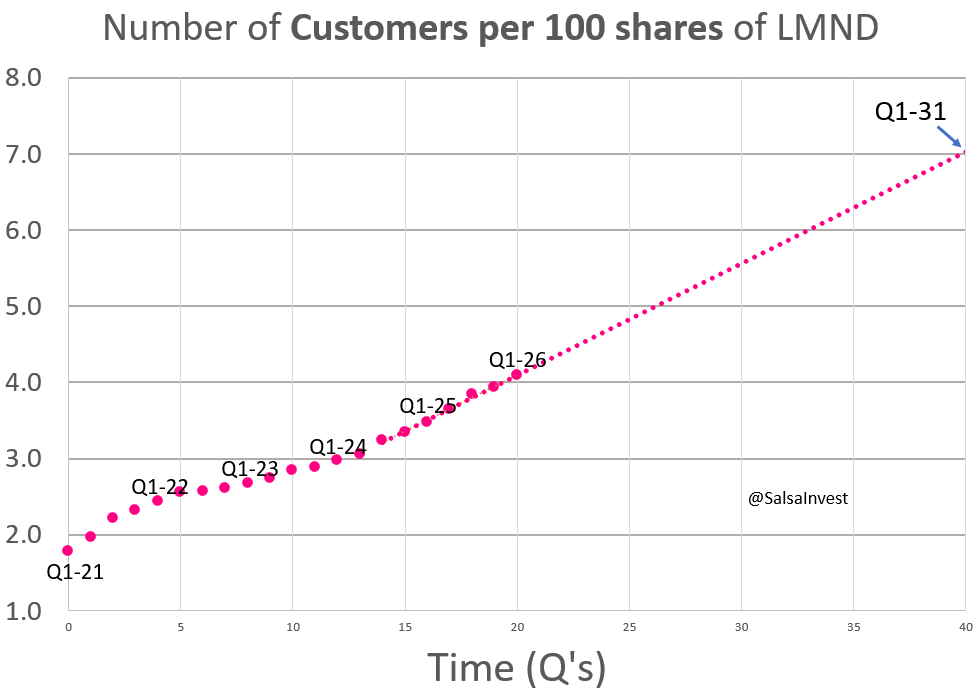

$LMND shares outstanding: 76,786,720

$LMND # of customers: 3,142,581 🍋

You get 1 customer for every 24.4 shares that you buy. At the current share price of ~$53, it means you get 1 customer for every $1293 you invest. FOREVER.

Think about all the profits you make for your insurance companies over the course of your life... You got it, a lot more than $1293!!!

Better yet, that 1 customer may turn to 1.7 customers magically in 5 years, and continue to multiply thereafter, WITHOUT YOU HAVING TO DO ANYTHING.

Indeed, $LMND 's customer count is increasing faster than its outstanding # of shares, so you have a free accretion of customers over time.

Look at the chart. What you see is your passive accretion of customers over time. The trend suggests that you would have ~7 customers/100 shares in 5 years from now, that is a net accretion of ~72%.

Of course, the value of your customers will go way up as well over time as they mature and get a 🚗, a 🏡, a🐶, etc.

THE TAKEAWAY: Thinking in terms of owned customers help you think long term. Track the # of customers that you own instead of your position size in $, because it concretely represents the future value of what you own. 🍋🍋🍋

One thing I learned at SpaceX. Good ideas aren’t worth anything. Lots of people have good ideas, and they are willing to share them. What actually is valuable is the implementation. If you can make a good idea a reality, that is the secret sauce.

There were several times when someone felt guilty about getting credit for implementing someone else’s good idea. Good ideas aren’t worth took 5 seconds to spout out, implementation took 6 months of 12 hour work days and blood sweat and tears. Full credit always goes to the implementer

That was a short-term loan when I ran out of money in 2008. He did not receive any equity for it.

Antonio’s ownership stems from absolute support, even when it looked like SpaceX would fail, and many investments over 2 decades.

One could not ask for a better friend. He is a great man.

@jawwwn_@60Minutes There is obviously no “degree” you can get from a university that actually teaches you how to make an orbital rocket, as none of the professors know how to do it!

Tesla drivers in Indiana can now get an up to 50% insurance discount when using FSD (Supervised), with the launch of Lemonade’s new Autonomous Car insurance program.

"Tesla FSD is twice as safe, so Lemonade takes 50% off every mile driven with FSD. The more you drive with FSD, the less you pay. As FSD versions improve, prices go down."

HW4 Tesla owners only. Expansion to other states is coming soon.