We’re co-leading the $475M seed round for Unconventional AI, a research lab tackling the moonshot of highly efficient AI-first chips. CEO Naveen Rao has sold two companies previously, and we’re excited to be partnering with him in his next endeavor. He joined a16z’s Matt Bornstein at NeurIPS for a conversation on starting a new chip company, what better chips would mean for AGI, why Naveen is so passionate about this mission, and more.

00:00 Intro

00:56 Exploring hardware for running AI workloads

02:02 Why Naveen built lots of software in a "hardware company"

03:22 Why start a new chip company?

05:13 How computing systems went digital

09:26 Why intelligence is a good fit for analog computer systems

12:30 What tradeoffs Naveen faced in pursuing his own path

15:23 The Data modalities Unconventional chips will be best for

16:54 Does this get us closer to AGI?

21:00 Where Naveen gets his excitement and motivation

22:37 What makes Naveen confident that Unconventional will work

24:43 Unconventional's hiring priorities

26:27 Career advice for young people

28:19 What Naveen has done best in his companies

@NaveenGRao@BornsteinMatt@unconvAI

Private credit margin compression speedrun:

Q1 2023: 650 bps median spread

Q4 2025: Sub-500 bps

This month: Deals at 400 bps

Banks: 285 bps

What happened: Everyone raised billions and shifted to credit just as banks came back with cheaper pricing

The denominator got bigger, the returns got smaller.

I am on sabbatical this academic year, and while I will not be teaching my corporate finance & valuation classes at NYU in Spring 2026, the full versions of my Spring 2025 classes, with lectures, class material and tests/exams are accessible online. https://t.co/pxLrAzyXQx

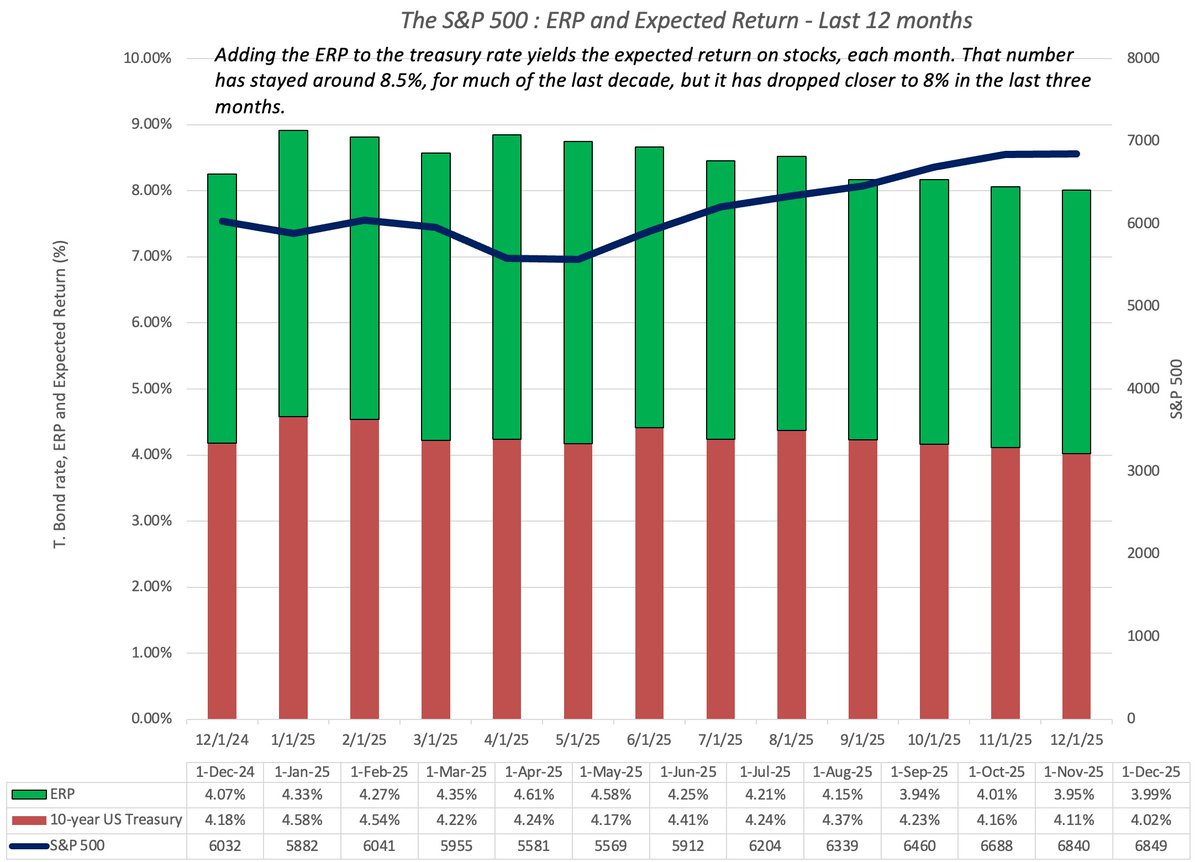

In November 2025, the S&P 500 and treasury rates barely moved month-to-month, but day-to-day, it was rocky. The equity risk premium starts December at 3.99%, and with the ten-year treasury at 4.02%, the expected return on stocks is 8.01%. https://t.co/IfY5XbiNdu

*ALTICE USA SUES APOLLO, ARES, BLACKROCK OVER COOPERATION PACT

We’re so back. Distressed debt needs this level of hostility. Debtors and creditors fighting, and everyone getting their popcorn out to watch. What’s next for Patrick Drahi’s empire? $ATUS $OPTU $CSCHLD

Have been saying this for a while but private equity is no longer the career it used to be

> Funds are no longer returning capital to LPs at the same rate. Means carry dollars are worth much less and also you are waiting much longer for carry to vest

> At the top end, deals are becoming increasingly competitive. Numbers of firms bidding on a quality deal is simply too high. Auction led process drives prices up, leverage up, and the risk / reward becomes much less favorable

> As time for carry to vest is increasing, middle managers and sticking around for much longer at any given firm. This puts pressure on the VPs and Associates as promotion pipelines then get extended or delayed. The entire career stack becomes less attractive, even from a junior perspective

> Everyone at these private equity firms are all running the same math, hiring the same consultants and accountants, and creating the same analysis to push deals through IC. There is nothing proprietary about the underwriting anymore. The only differentiation is in: (i) type of deals you source, which might give you an edge and (ii) the operational value you add

> Junior private equity folks are realizing that there are simply better ways to make money if you are working 70-80 hours a week. You can make reasonably good money working on the business or strategy side of tech and AI companies while working 75% of the hours. The trade off doesn’t make sense anymore given the reward is so much smaller today