Algunos hilos sobre energía y desarrollo:

Bienes de capital e hidrocarburos: https://t.co/cnsaCFOlVX

Pol. industrial y energía: https://t.co/REk1Q877Cj

Transición energética en Argentina: https://t.co/EourEeqXx4

Electrificación y transición: https://t.co/f9DkPh65PH

1. Hagamos una visita más al mundo de la electricidad de la mano de Shell. En una reciente entrevista, https://t.co/9jOUFOrB4f, Maarten Wetselaar, director de Unidad integrada de gas y nuevas energías de Shell ha señalado que la empresa busca ser líder para 2030 en el negocio de.

¿En qué se basa la ventaja estratégica que tiene China en minerales? EN CONOCIMIENTO, y está claro el porqué.

El presidente estadounidense Donald "Trump y otros líderes occidentales han prometido miles de millones de dólares en inversiones para romper el monopolio chino en el refinado de tierras raras, una poderosa baza que Pekín ha utilizado en su guerra comercial con Washington. Sin embargo, China aún conserva una ventaja significativa en la captación de talento que ha desarrollado durante décadas en lugares como Baotou."

¿Que se necesita para crear un ecosistema que entienda y desarrolle esos procesos productivos?, sin dudas recursos monetarios, tecnologia, voluntad política y tiempo, EEUU tiene mucho de lo primero segundo y tercero , pero no tiene lo cuarto, si quiere alcanzar a China en esta carrera mineral...la cuestión actual es de una ventaja atroz para los asiáticos, que vienen de décadas de no sólo preparase, sino tener en su territorio el conocimiento necesario para ser los más relevantes a nivel mundial. Si China decide cerrar la canilla a las expo de tierras raras refinadas, grandes porciones de cadenas industriales de producción, desde autos hasta armamento, simplemente se detendrán. Aquí @Reuters lo explica claramente.

https://t.co/3LFtlfbzv9

Vladimir Putin's visit to Beijing showcased an unbreakable alliance with Xi Jinping. But behind the closed doors, the crisis in the Strait of Hormuz is completely scrambling the rules of the Sino-Russian energy relationship.

The hard data tells a different story.

🧵👇

The US Department of Energy just mapped every data center in America.

This is what the AI power grid looks like.

The dots are data centers.

Yellow = operating.

Orange = under construction.

White = planned.

The lines are high-voltage transmission 735kV, 500kV, 345kV the arteries that move electrons from generators to compute loads.

Look at the density along the East Coast, Northern Virginia to the Carolinas.

Then look at Texas.

Then Northern California.

The largest circles on this map represent facilities demanding over 5,000 MW of power.

Single campuses pulling more electricity than mid-sized cities.

Northern Virginia is so dense the dots overlap.

Data centers cluster on transmission corridors.

Not because land is cheap because power is available.

When the line is full, the next data center goes somewhere else.

The grid is the bottleneck.

Every orange dot is a power purchase agreement being negotiated right now.

Every white dot is a utility commission filing, a gas plant approval, a pipeline capacity booking.

The $66.8 bn NextEra-Dominion deal, Meta's 10 new gas plants in Louisiana, the Alaska LNG FID push they all trace back to maps that look like this.

AI infrastructure is built in substations, on transmission corridors, and at the end of gas pipelines.

Link in the comments, to see my stocks 👇

🇬🇧🏭 Starmer anunció un proyecto de ley para estatizar British Steel: buscan que el 50% del consumo británico de acero sea producido localmente. Por otro lado, en la estatizada Sheffield Forgemasters avanza la construcción de una prensa de 13.000 toneladas (£ 1.300 millones).

🇸🇦🇵🇰UN NUEVO 'PARAGUAS NUCLEAR' SURGE EN EL GOLFO PÉRSICO

Arabia Saudita y Pakistán firmaron en 2025 el Acuerdo Estratégico de Defensa Mutua. El pacto establece que un ataque contra uno será considerado ataque contra ambos.

¿Qué implica esto en el escenario mundial de hoy?

As Europe is slowly warming up again it’s time for my annual reminder that adding shade to the urban environment helps to reduce the urban heat island effect massively. It's a super important tool to keep cities cool during the summer.

🚨The world's 5 largest energy consumers

1 number changes how you read everything else on this chart

🇨🇳 China: 48,400 TWh

🇺🇸 US: 25,800 TWh

🇮🇳 India: 11,200 TWh

🇷🇺 Russia: 9,000 TWh

🇯🇵 Japan: 4,800 TWh

China consumes nearly twice as much energy as the United States.

But the mix is what tells the real story.

China's coal consumption alone is visually larger than the entire US energy stack combined.

The US is running on gas and oil, with nuclear and renewables as meaningful contributors.

China is running on coal, with everything else added on top.

India, the 3rd largest consumer and the fastest growing major economy, is also coal-dominant with gas playing a minimal role compared to its peers.

Russia's profile is the inverse: gas-heavy, oil-significant, almost no coal at scale.

That's a direct reflection of geography Yamal and Western Siberia make gas the default fuel for everything from heating to industry.

Any global energy transition runs through coal in China and India first.

Until those bars change shape, the conversation about net zero is largely theoretical.

A medida q sube conflictividad geopolitica China acelera sus procesos de baja de dependencia de importaciones, mas alarmas para expos nacionales: Sustitución de soja en cerdos: el nuevo enfoque de China para asegurar su alimentación animal https://t.co/Li8ciWCiAs

¿Qué es lo que ocurre cuando descuidas sectores industriales estratégicos? simplemente ocurre lo que le está pasando a Australia.

¿Cual es el modelo de Australia? como la mayoría conoce es el de exportaciones de commodities, el cual no es erróneo, pero sí insuficiente en cierto sectores (por ello se habla de sectores estratégicos y no estratégicos). Este gran país, al cual admiro, exporta crudo e importa refinados, o sea combustibles. Esto trajo aparejado que ante el shock externo que estamos viviendo, se encontró con un problema, tiene dificultades para conseguir combustible....

"El sistema de refinación nacional de Australia ofrece poco alivio. El país opera solo dos refinerías: Lytton (110 000 b/d) y Geelong (120 000 b/d), con una capacidad combinada de 230 000 b/d, que cubren apenas el 20 % de la demanda nacional. Ambas instalaciones presentan limitaciones estructurales . Dependen completamente del crudo importado, ya que la producción nacional australiana (principalmente crudo ultraligero, rico en condensado, con una gravedad API superior a 55-60) no es adecuada para su configuración. Las refinerías en sí son activos obsoletos, construidos en las décadas de 1950 y 1960, diseñados para una mezcla de crudo y un entorno de mercado diferentes. Su perfil de producción también se desfasa con respecto a la demanda interna. Las refinerías australianas producen principalmente gasolina, alrededor de 100 000 b/d de gasolina y 80 000 b/d de diésel, mientras que el consumo se inclina hacia el diésel, el segmento que actualmente sufre la mayor presión."

En síntesis, hay sectores que son necesario atender y mantener, aquellos que son esenciales para el continuo desarrollo.

Fuente:https://t.co/FsXKaoCPoV

Everyone is talking about the oil. Almost nobody is talking about the machines.

When Iranian missiles hit Ras Laffan on March 18 and 19, they did not just knock out LNG production. They struck the most concentrated node of cryogenic industrial infrastructure on earth. And the reason QatarEnergy’s CEO told Reuters that repairs will take three to five years is not because the buildings are hard to rebuild. It is because the machines inside them are nearly impossible to replace.

The core technology in every LNG train and helium extraction unit at Ras Laffan is the brazed aluminium plate-fin heat exchanger, known in the industry as a BAHX. These are not off-the-shelf components. They are custom-engineered cryogenic cores weighing up to 470 tonnes, standing 60 metres tall inside insulated cold boxes, manufactured by exactly five companies on earth: Chart Industries in the United States, Fives Cryo in France, Kobe Steel in Japan, Linde in Germany, and Sumitomo in Japan. That is the entire global supply per ALPEMA, the manufacturers’ own association.

Current lead time for a full mega-scale air separation unit built around these exchangers: three to four years from contract to commissioning. Lead time for the BAHX cores alone: 12 to 18 months with order books already full before the war started.

Here is why field repair is so difficult.

Aluminium has no fatigue endurance limit. Every thermal cycle accumulates irreversible damage. The brazed joints crack under thermal stress, and ALPEMA’s Integrity Operating Windows cap temperature changes at below 1 degree Celsius per minute during normal cycling and below 5 degrees per minute even during startup events.

When a joint cracks, the only field repair is layer blocking: welding shut the distributor openings of the damaged layer while leaving adjacent layers open. Chart Industries, the primary manufacturer, recommends a maximum of two blocks before the entire core must be replaced. Each block reduces heat transfer efficiency. Each block increases stress on remaining layers, accelerating the fatigue cycle.

Shell confirmed on March 20 that Pearl GTL Train 2 will take approximately one year to repair. The LNG trains S4 and S6, with 12.8 million tonnes per annum combined capacity, will take three to five years per QatarEnergy. The difference in timelines reflects damage extent, not repair difficulty. Both face the same physics.

And both face the same logistics problem. Every replacement module, every specialist welder with an ASME R-stamp authorization, every 470-tonne cold box shipment must transit the Strait of Hormuz. The same strait where 90 percent of the world’s ocean-going tonnage has lost war risk insurance coverage. The same strait where the IRGC operates a selective vetting corridor with at least two confirmed yuan-settled payments per Lloyd’s List. The same strait where premiums have surged from 0.125 percent to 7.5 percent of hull value.

The machines cannot be repaired without parts that cannot be shipped through a strait that cannot be insured.

This is the machine layer that connects the helium shortage to the semiconductor shortage to the AI compute shortage. Qatar produces one-third of the world’s helium as a byproduct of LNG processing through these exact machines. Helium spot prices have doubled. Samsung and SK Hynix hold six months of inventory. There is no substitute in cryogenic semiconductor applications per the USGS.

The market priced the oil shock. It has not priced the machine shock. The timeline is measured in years, not weeks.

https://t.co/32ixeQpN7N

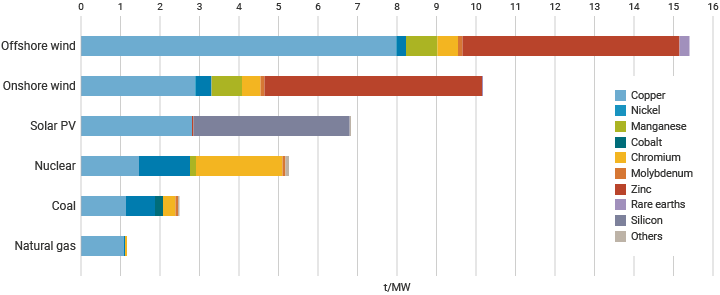

China’s new Five-Year Plan will increase demand for copper

- Add 238-287 GW of new solar capacity annually

- Add at least 120 GW of new wind capacity annually

Copper requirement per installed MW of capacity

- Offshore wind: 8t

- Onshore wind: 3t

- Solar: 3t

- Coal: 1t

- Gas: 1t

Renewables need 3x-8x more copper per installed MW than fossil fuels

This is a massive tailwind for copper demand. In fact, the energy transition is the main driver of copper demand, accounting for ~60%.

Los autores de este artículo, dos de los científicos del comportamiento más influyentes del mundo, realizan una autocrítica sincera sobre el tema de los nudges (empujoncitos).

Durante años creyeron que los pequeños “nudges” (empujones sutiles) podían resolver grandes problemas sociales y ambientales haciendo que las personas tomaran mejores decisiones individuales: comer más sano, ahorrar más, reducir su huella de carbono, vacunarse, etc. Hoy admiten que se equivocaron.

Según ellos, el enfoque conductual ha caído en una trampa: al centrarse casi exclusivamente en modificar el comportamiento individual, ha desviado la atención de las verdaderas causas de los problemas, que son sistémicas (diseño de mercados, incentivos corporativos, políticas económicas, entornos laborales y comerciales). En lugar de cambiar los sistemas que empujan a la gente hacia decisiones perjudiciales, la ciencia del comportamiento ha terminado culpando sutilmente a los individuos por sus “malas elecciones”, ofreciendo soluciones superficiales que no resuelven los problemas de fondo.

Chater y Loewenstein concluyen que ha llegado el momento de cambiar de dirección: la ciencia conductual debe dejar de obsesionarse con nudges individuales y empezar a presionar por cambios estructurales reales en las empresas, los mercados y las políticas públicas. Parchear el comportamiento de las personas ya no es suficiente.

The war at Hormuz does not end at the gas pump. It ends at the grocery store.

Urea at the port of New Orleans just hit $690 per ton. It was $475 three weeks ago. That is a 45% surge in the nitrogen fertilizer that American corn depends on to exist.

The Fertilizer Institute says US farmers are short roughly 2 million tons of nitrogen for spring planting. USDA projected 94 million corn acres for 2026, already down 4.8 million from last year. That projection was made before the Strait of Hormuz closed. Before urea doubled. Before the planting window started closing.

Here is the part nobody is modelling.

Roughly 25% to 30% of globally traded nitrogen moves through the Strait of Hormuz. The strait has been functionally closed for 27 days. QatarEnergy halted downstream urea production after the missile strikes on Ras Laffan. China has restricted fertilizer exports to protect its domestic market. Europe is still running at 75% nitrogen production capacity because of high natural gas costs from the Russia-Ukraine war.

Three of the world’s four major nitrogen supply sources are simultaneously constrained. That has never happened before.

American Farm Bureau Federation President Zippy Duvall wrote directly to Trump calling it a production shock threatening national security. CRU Group’s Chris Lawson told CNBC that 30% of global urea trade comes out of Iran and Hormuz-constrained countries: “If farmers aren’t able to get the urea that they need, crop yields will inevitably go lower.”

It takes 30 days for a vessel of urea to load in the Persian Gulf, sail to the US, and reach the interior. A vessel loading today might not arrive until May 1. The spring application window does not wait for a ceasefire.

Every week of continued disruption pushes more acreage from nitrogen-intensive corn toward soybeans. Once planted, that decision is irreversible for the growing season. The corn-urea ratio is at 87 to 90 bushels per ton, a five-year high per CME Group data. Farmers cannot afford to plant corn at these nitrogen prices.

This is not a commodity cycle. This is a structural acreage reallocation being driven by a naval blockade eight thousand miles from Iowa, and it will show up on every American’s grocery receipt by autumn.

USDA Prospective Plantings report drops March 31. Watch the corn number.

https://t.co/32ixeQpN7N

“… we will increase the operation of coal-fired power plants and conserve LNG usage…” — Japan’s Prime Minister Sanae Takaichi

(Tokyo believes it can reduce its needs of LNG via Hormuz by ~40% via leaning on coal and the re-start of a nuclear power reactor shut for 14 years)

Proceso de refinacion de petroleo, y como el crudo finalmente es combustible de distinto tipo y asfalto. Como ven el proceso requiere de varios segmentos, no es simplemente la destilación.

Se publica hoy en el BO https://t.co/IKWR0S2Gy2 resolución que actualiza normativa técnica para permitir mezclas de hasta 15% de bioetanol con nafta, salvando inconsistencia que se arrastraba desde reglamentación de ley 27.640 mediante reso 689/22 que ya permitía corte del 15%.

para aumentar el corte como manera de contener el precio en el surtidor, ya que el bioetanol es más barato que las naftas, a la vez que es el aditivo de octanaje más barato. Buena noticia p/ el sector de bioetanol y para los consumidores. @BioetanolDe@Bio4Argentina@fkrakowiak