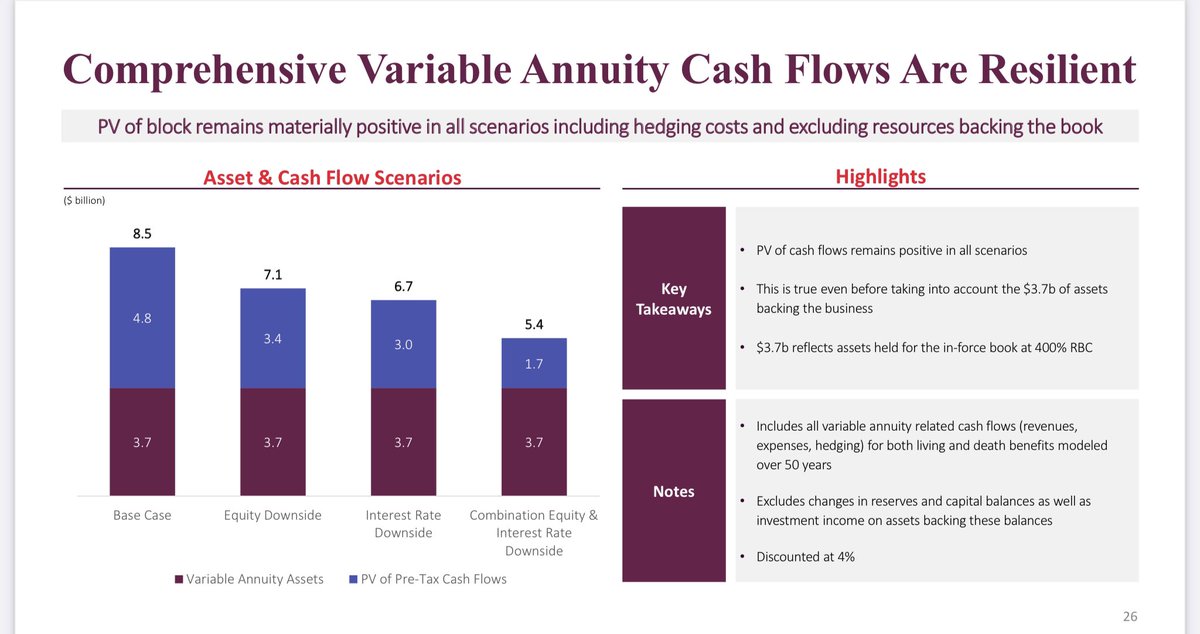

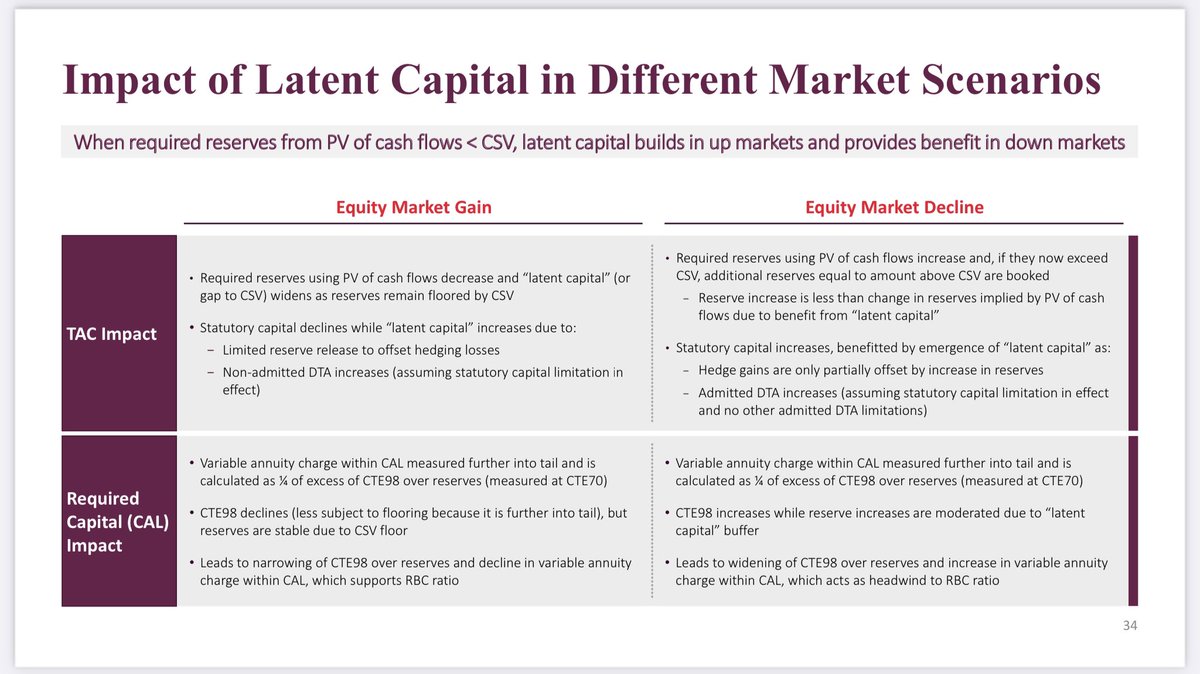

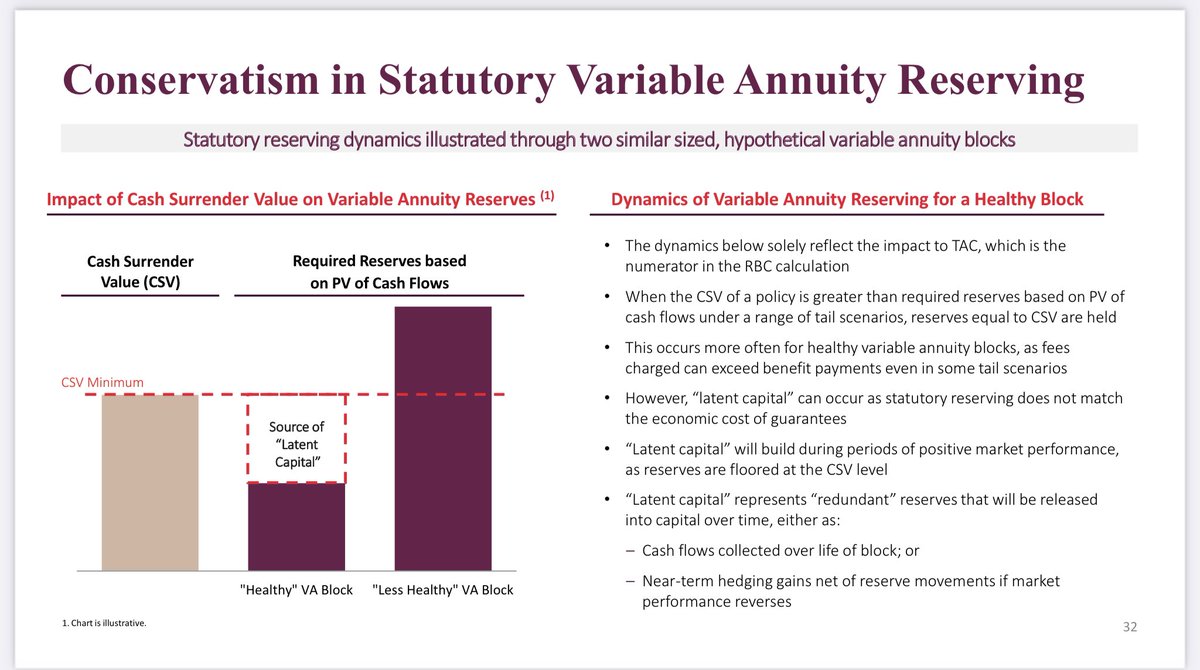

@the_red_deer@GrandTokamak@hank_moody12@x3nophan3s@hungry_cap@MadThunderdome@brkb19 $JXN valuation makes zero sense. Current EV ($2.2bn MC + $1.6bn net debt at hold co) roughly equals NTA (per analyst day). Infers VA book is worthless, despite $JXN having latent capital (excess reserves)! Moreover, rate rise has reduced NPV of guarantees and cost of hedges.

2. Idea Generation

"The idea generation process is very organic. We've got 10 stocks, we own them and we're fully invested. I've told our team on any given day you come to work, we're not looking for new ideas. What I want you to do and what I do is go deeper into what we already own. So if there's a customer out there, if there's a competitor out there, if there's a conference out there, let's go attend that and try to turn over one more stone. There are stocks that we own today that we've owned for six years. You can imagine doing work on a stock for six continuous years, in your fifth or sixth year or even in your third year, you're no longer asking the basic questions. You're going several layers deep. I will bet you any amount of money that if you own a stock for three years, by year three, you have turned over the stone on 10 of the companies and in year four you're actually now going quite deep into some of these companies. Some of them might be private, some of them might be competitors, some of them might be just other companies in the supply chain. Odds are your next best idea will come from that diligence process. So we don't do screens, we don't look at 13Fs as a formula for finding ideas. We don't check CNBC or read Substack and newsletters or anything like that. We're doing research and there has never been a day, a week, a month, a quarter, a year where out of that research we don't find 10 other ideas. That's the crux of our idea process. Every single idea we own today came from something else we owned, and I will bet the next 10 ideas will come out of things we own today."

Ran a small operating biz for 2 years prior to allocating capital full time. 15-20 person motel, real small fry, hyper-competitive, constantly felt like we were on death’s doorstep. Biz had been mismanaged for years. So, was essentially a 2-yr turnaround project. Biggest lesson relevant to investing: pivoting a business - culture, strategy, product - is incredibly hard to borderline impossible. The easy levers you can pull are finance-related / balance sheet engineering. If I’d only ever been a passive investor, would never have appreciated just how path-dependent businesses really are. Not a groundbreaking insight - “Halo Effect” explains a similar illusion of control attributed by outsiders / investors to corp insiders. All of this is amplified if you’re selling a commodity product - your fate really does rest on the industry tide. Whole experience blew up whatever romantic notions I had of business “control”. And instilled a big dose of humility / respect for the intricacy in every business / industry.

Ran a small operating biz for 2 years prior to allocating capital full time. 15-20 person motel, real small fry, hyper-competitive, constantly felt like we were on death’s doorstep. Biz had been mismanaged for years. So, was essentially a 2-yr turnaround project. Biggest lesson relevant to investing: pivoting a business - culture, strategy, product - is incredibly hard to borderline impossible. The easy levers you can pull are finance-related / balance sheet engineering. If I’d only ever been a passive investor, would never have appreciated just how path-dependent businesses really are. Not a groundbreaking insight - “Halo Effect” explains a similar illusion of control attributed by outsiders / investors to corp insiders. All of this is amplified if you’re selling a commodity product - your fate really does rest on the industry tide. Whole experience blew up whatever romantic notions I had of business “control”. And instilled a big dose of humility / respect for the intricacy in every business / industry.

"the largest source of income for the 1% highest earners in the U.S. isn’t being a partner at an investment bank or launching a one-in-a-million tech startup. It is owning a medium-size regional business. Many of them are distinctly boring" https://t.co/38GVllqnzi

Officially drunk the Kool Aid on Japanese cap return story (see recent pods by @puppyeh1@evantindell@verdadcap for full details of corp gov reforms). New holding: $7267 (Honda). Current market cap 6tn¥. P/B < 0.5. Dividend yield ≈ 5%. And 1.1tn ¥ buyback plan for CY25. (1/3)

@Scott_Reardon_ The generational buying opportunity in O&G was 2020 - not today. Energy was ground zero for lockdowns. The comparable bargain today is more likely to be the Auto OEMs - ground zero for tariffs.

@Scott_Reardon_ How many of the greats you studied took the Kelly criterion seriously? Munger, Soros, the Chandler Brothers? 8 stocks achieves 80% of the diversification benefit of owning 200 (statistically). But if vol is not an issue (permanent capital), what's the optimal portfolio size? 3-4?

@Scott_Reardon_ EV/bpd seems like a terrible metric (ignores reserve life & capital intensity). IMHO, better off backing out val of mid & downstream business to calc EV/PDP (your F&D cost). Compare that to OCF margins and you've got your own investor recycle ratio: https://t.co/mj0tBXSuhI

Biz has ≈ 40% market share, ≈ 17% OP margins & >20% ROCE. It ALONE is probably worth the current market cap (5-6tn ¥). SOTP val (cash & sec; leasing; bikes) gets you close to BV of 13.5tn ¥. Auto OEM is free upside. Even with EV shift, tariffs etc - looks way too cheap. (3/3)

Officially drunk the Kool Aid on Japanese cap return story (see recent pods by @puppyeh1@evantindell@verdadcap for full details of corp gov reforms). New holding: $7267 (Honda). Current market cap 6tn¥. P/B < 0.5. Dividend yield ≈ 5%. And 1.1tn ¥ buyback plan for CY25. (1/3)

Net cash & securities ≈ 4.4tn ¥; BV of auto leasing biz ≈3.25tn ¥. So, even assuming Auto OEM biz is worthless & only half the net cash is excess capital, that still ≈ covers the market cap. But wait, there's more! Honda is also the world's premier motorcycle OEM (2/3)

If you look at scientific discoveries before ~1800, it's not 25 people collaborating on a paper from large, well-funded institutions, it's some lone, weirdo aristocrat who either personally or by patronage found it more interesting than duels and prostitutes

Saw some chatter from folks here I respect on exiting $JXN (e.g. @ArrakisGlobal@blondesnmoney). Can't blame the thinking, the shares have had an amazing year, so I get the rationale and pullback this month. Some high-level thoughts on the longer-term case as a counterpoint fwiw: