In a few years we’ll look back reminiscently at these “boring” times for $LMND and think how simple it was to just DCA while reading one encouraging report after another - all while approaching FCF+, lower loss ratios, higher IFP, stabilizing OPEX, and new geographies/products

Remember when $LMND 🍋 was trading at $16 after 5x’ing its IFP since their IPO and being on a clear path to profitability? Yeah, I remember that.

I bought more today ✅

Took this as an opportunity to reflect on my LMND journey.

Logged into the brokerage and did some digging.

Over the past several years, I have purchased shares on 71 separate occasions (8 times in 2021, 7 times in 2022, 3 times in 2023, 23 times in 2024, 19 times in 2025, and 11 times in 2026)

Wow.. what a journey this has been.

Thanks to everyone at @Lemonade_Inc, the Lemonade community on X, and all the wonderful thought-leaders in the space.

@jakebrowatzke In less than a year from now, we’ll be staring break even in the face. No more wondering, questioning, doubting. It will just be here. Plain and simple.

At that point, the numbers will not look horrendous.

By then, the stock will not be where it is now.

Appreciate these thoughts.

I think it’s funny how a consistent and relentless 34% compounder can get overlooked in the 80% growth phase of these hardware names.

I’m happy to have a 30+ % CAGR over a decade or more compared to what may be a shorter term growth rate in these other names

Any thoughts on how to fix housing unaffordability in California? Or, is it too far gone?

According to the California Association of Realtors, CA's median home price is ~$905,000 requiring an annual income of $213,200 per year and a downpayment of $181,000.

CA median household income is less than half of the annual income requirement for a median priced home, at $100,100.

Depending on the neighborhood and region, the near-million home would likely be a run down 2 or 3 bedroom house built in the 1960s.

The national median sale price for a home is sitting right around $436,523. Buying a median-priced US home requires an income of roughly $115,000 to $120,000 if you are putting 20% down.

💵 $375k House: Needs ~$102k income ($2,395 total monthly)

💵 $500k Condo (+HOA): Needs ~$150k income ($3,510 total monthly)

💵 $750k House: Needs ~$205k income ($4,790 total monthly)

💵 $900k House: Needs ~$246k income ($5,747 total monthly)

Ah I appreciate it!

You’ve been a great resource to follow.

On a conviction scale, 10 being very high almost sure and 0 being not sure at all would never invest

I have LMND at a 9 and HIMS at a 5

The risk reward just looked super compelling for HIMS back in February.

Other stocks I have above a 5 or more for are BEPC, ASML, $MELI

But LMND is by far the highest.

It is easy for me to sit back and watch management compound their book of business at a 32+ % CAGR over a decade

Running the numbers on a consistent 30% CAGR is pretty mind blowing

@307Fool Changing *fairly* convicted to *very* convicted

Ran some of the basic numbers and guidance projections. Even conservatively it felt super undervalued. Right now it probably still is, I just haven’t run / looked at the numbers in a while

@307Fool Nice! I’ll be checking out HIMS as well!

Only been a shareholder since February but felt fairly convicted during the feb march timeframe and made it my second largest position 🕺🏼🫣🤷🏼♂️

Another great $LMND quarter!

I’m a happy longer term shareholder.

At $56/Share and a $4.35B market cap, I believe I can purchase shares at less than half their 2026 fair value.

After the Q4 2026 report, I got a conservative number of around $115

Haven’t done the math yet but after another 32% YoY growth (7.76% QoQ)…. with EBITDA losses narrowing and profitability about to inflect…. I’d have NPV/share a bit higher

Customer Life Time Value (LTV) to Customer Acquisition Cost (CAC) is still 3:1 despite a ramp in OpEx.

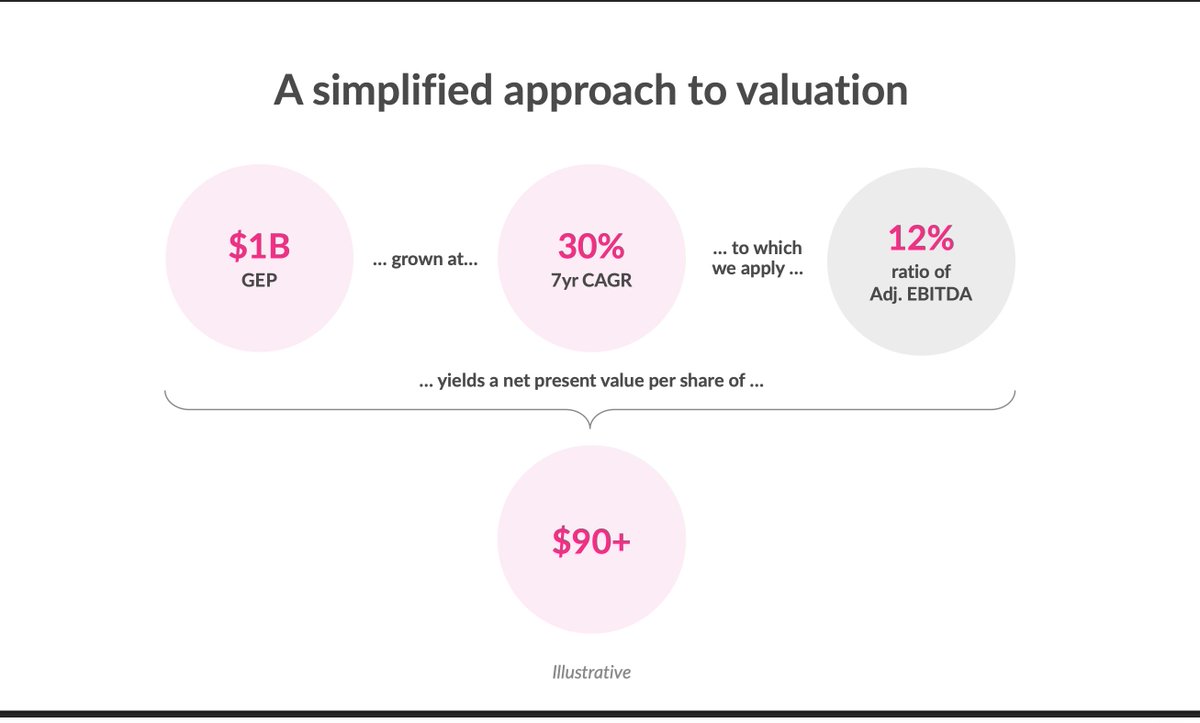

At the November 2024 $LMND Investor Day, CFO Tim Bixby conceptualized an NPV per share of $90+

Using Tim's same mental model, based on 2026 estimates, we get an NPV of $115+

Buying shares in the $60s today is significantly less than the 2024 fair value per share and dramatically less than the 2026 fair value per share ✅

Napkin Math:

FY25 GEP guidance is around $1.047B, and @PaperBagInvest estimates FY26 GEP to be around $1.380B (subscribe to his Patreon for full access to the model)

So, take $1.38B grown at 31% and apply a 12% ratio of Ajd. EBITDA and we get......

GEP year 7 ≈ 1.38B×(1.31)^7 ≈ $9.2B

Apply 12% Adj. EBITDA Margin, 9.18B×12% ≈ $1.10B

Tim’s original $90+ implied something around a 15x multiple on EBITDA, please correct me if you think otherwise.

Market cap 7 years out = 1.10B×15 = $16.5B

Discount 7 years at 10% (might be too low of a rate)

NPV ≈ $8.5B or $115–120/share

Reminders:

EBITDA is expected to flip positive this year.

CAGR has been accelerating and management hints at growth in the low 30s not up to and stopping at 30%. This could mean anywhere between 31-33% IMO.

At investor day, management said that if total earned premium doubles from $1B to $2B, cash flow - adjusted FCF - will 20x from $15M to $285M. That is EXTREME operating leverage.

In fall 2022 LMND’s loss ratios were 94%. In fall 2024 they were 62%, while the trailing twelve months (“TTM”) loss ratio was 67%.

Cash flow break even was originally guided for 2025. LMND achieved it a year ahead of schedule in 2024. FY 2024 was cashflow positive as a whole.

IRR with synthetic agent funding is 112%

Over the past few years, $LMND kept up with their guidance and even out performed their guidance despite a generational inflation bout that rocked the insurance industry.