Wow, the S&P Dow Jones Indices has just officially announced that they will NOT be changing their inclusion rules to make it easier for “MegaCap” companies (such as @SpaceX) to be fast-tracked into the S&P 500.

Their reasoning:

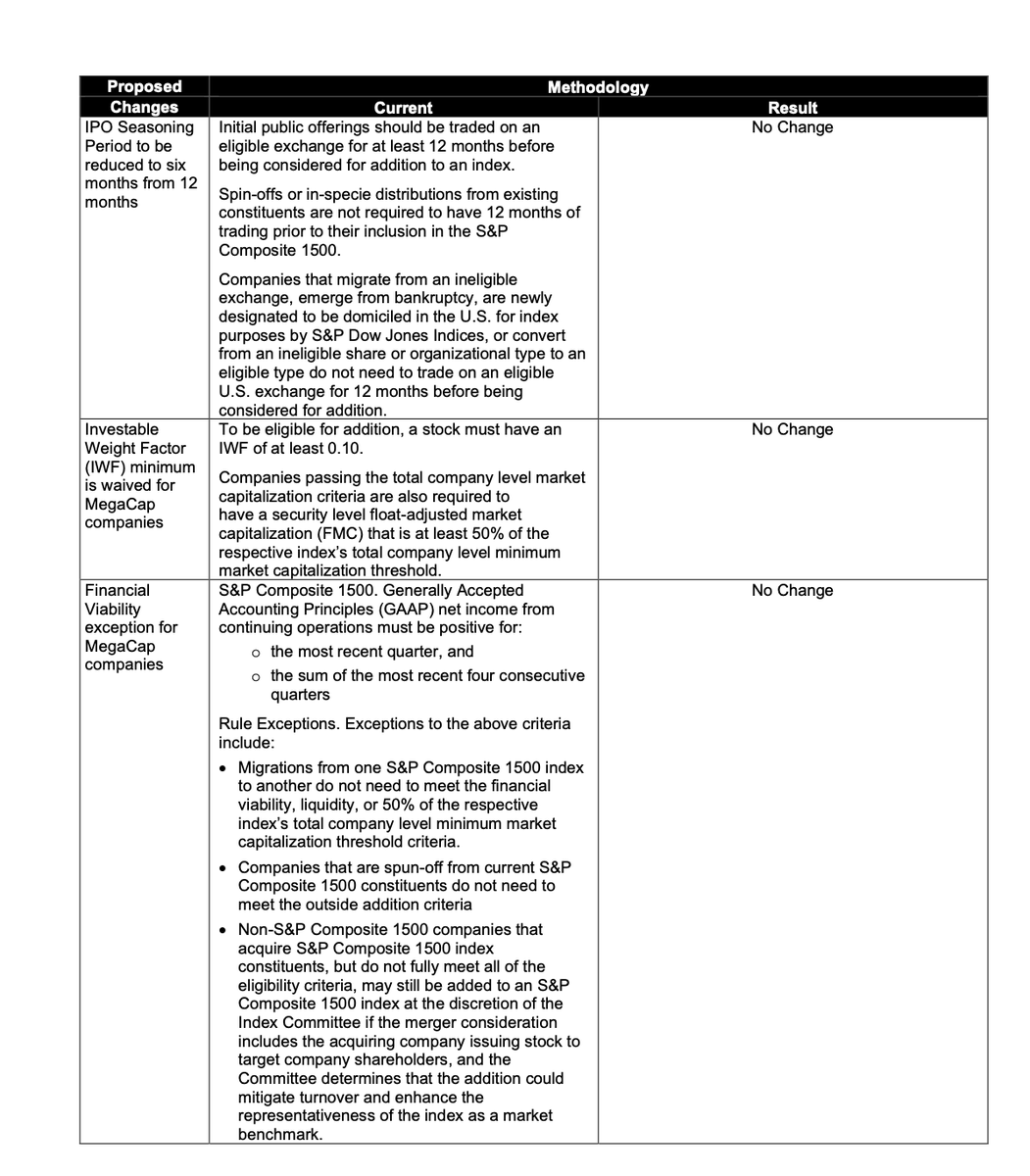

"S&P DJI determined that exceptions to the financial viability, seasoning, and IWF requirements should not be granted solely based on market capitalization. The decision not to adopt the proposed exceptions preserves core index principles by maintaining consistent application of these key requirements. Although there may be trade-offs between strict adherence to these eligibility requirements and broad representativeness, the current methodology provides substantial market coverage and sector balance. As a result, the indices can continue to meet their stated objectives while preserving their role as representative and investable benchmarks for the U.S. equity market.

No changes will be made to the eligibility criteria including financial viability screens, seasoning period, or minimum IWF, for the S&P 500, S&P MidCap 400, or S&P SmallCap 600 as a result of the S&P Dow Jones Indices consultation on the treatment of MegaCap companies. Accordingly, there will be no changes to existing methodology for this index family."

This means that the earliest @SpaceX could be eligible to be added to the S&P 500 would now be June 2027.

The requirements that will now remain in place are:

• No changes to S&P 500 eligibility rules for mega-cap companies.

• Mega-cap companies will still need to wait 12 months after their IPO before being considered for S&P 500 inclusion.

• S&P will not waive profitability requirements for mega-cap companies. The company must have positive GAAP net income in the most recent quarter, and the sum of the most recent four consecutive quarters.

• S&P will not waive minimum public float requirements for mega-cap companies. At least 10% of a company's shares must be publicly tradable ("free float").

The S&P rejected proposals that would have:

• Reduced the IPO seasoning period from 12 months to 6 months

• Waived profitability requirements

• Waived minimum public float requirements

google (and deepmind) would just win if they had a product leader with the balls to scorch earth the entire bureaucracy stack that is Google Product Management

Treasury’s CGT modelling appears heavily dependent on assuming Australian shares only deliver ~4.3%-4.4% capital growth p.a., which seems to come from measuring the ASX/200 and All Odds over the last 20 years, a period the Treasurer keeps repeatedly describing as evidence that shares were supposedly “undertaxed” or “undercompensated” - including in this interview with @BilliFitzSimons

But the only circumstance where inflation indexation actually benefits investors relative to the current 50% CGT discount is where inflation makes up more than 50% of total capital returns. That’s generally only true when capital growth itself is unusually low or it’s a market where a very high portion of the total return is paid in dividends (like Australian large caps). That’s not how most younger Australians invest today!

Most younger investors build globally diversified ETF portfolios with significant global share market exposure. Across Stockspot clients, around 50% of share market exposure is global. As one example, Stockspot’s most popular diversified portfolio (Topaz), delivered 7.3% annual capital growth over the 10 years to the end of April 2026, despite having around 22% in defensive assets like bonds and gold.

That massively changes the outcome under the proposed CGT system.

Using:

• $20k invested

• 10 year holding period

• 2.5% inflation

• 30% tax rate

At Treasury’s apparent 4.3% growth assumption:

> current 50% discount tax = $1,571

> proposed new tax = $3,141

But at a more realistic globally diversified 7.3% growth assumption:

> current 50% discount tax = $3,069

> proposed new tax = $6,138

i.e. the extra tax drag roughly doubles. You can use this CGT calculator to see this https://t.co/WFVQzYuMnt

That’s because the proposed inflation indexation plus 30% minimum tax model becomes increasingly punitive as long term capital growth rises. The higher the long term growth rate, the larger the portion of gains exceeding inflation, and the larger the compounding tax drag becomes over time. Which raises an important question... if the modelling omits global shares and other higher capital growth assets like crypto that younger Australians increasingly invest in, are the published examples materially understating the long term tax impact and presenting outcomes that aren’t representative of how people actually invest today?

Can't follow any Australian fintwit guys cause 95% of their tweets are about how homes cost $500 quintillion dollars and earning money has been outlawed

This is true.

Michael Burry: Mostly bearish

Robert Kiyisaki: Always bearish

Tom Lee: Always bullish

Cathie Wood: Leveraged bullish

Michael Saylor: Broke bitcoin

If you’re new to the markets, just know this.

too many people fell for their calls.

> web article about unis

> 90% of students using ai to cheat

> uni educators and staff frustrated

> call for revolution of education

> critics say school is cooked now

> phd lady writes article about it

> look inside

> "its not x—its y"

> "why it matters"