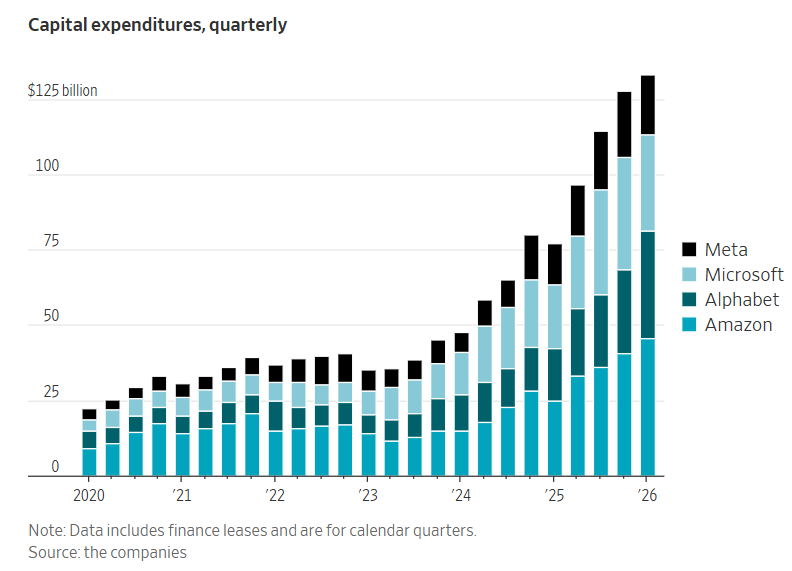

Do note that Alphabet expects $30B, or 37.5% of its proposed $80B raise, to go toward employee equity-award tax obligations not funding AI infrastructure.

Between stock trading by federal officials, insider trading in prediction markets, fixed sporting events, and suspicious moves in energy, integrity in markets feels lower today than at any point in the modern era.

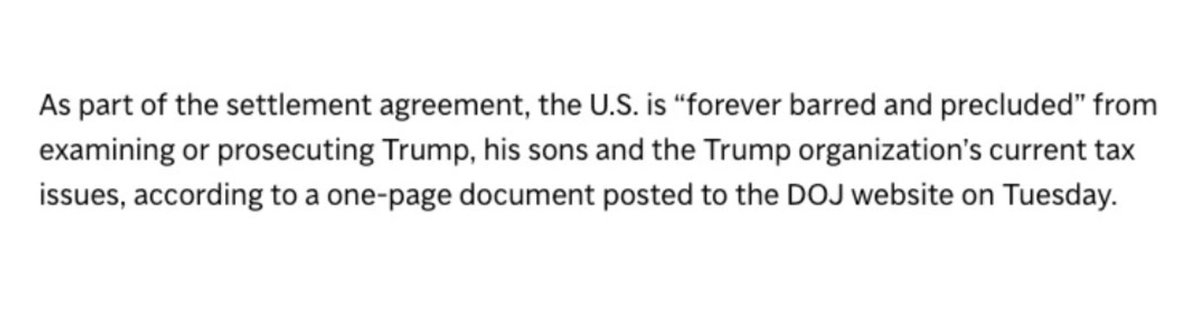

There are good reasons for this Jim. It is all Fugazi. How to make tens of $billions worth of $NVDA GPUs disappear from balance sheets in 8-12 byzantine stepspvs.

JPM: Another beneficiary of the AI cycle is European luxury stocks

The report argues that the AI supercycle has driven a surge in HBM and memory demand, sharply improving earnings expectations for Samsung Electronics and SK hynix. This, in turn, has supported equity-market strength, with the KOSPI up 91% year-to-date, bolstering consumer sentiment and high-end consumption.

While Korean households’ allocation to equities, bonds, and funds is only around 4%, lower than in the U.S. or Western Europe, the magnitude of the market rally means the wealth effect is still meaningful. JPM also estimates that the after-tax bonus pools at Samsung Electronics and SK hynix alone could reach roughly $25 billion in 2026 and more than $35 billion in 2027.

JPM expects this wealth effect to be particularly concentrated among younger male consumers. Given that roughly two-thirds of Samsung Electronics and SK hynix employees are male, the categories most likely to benefit first are luxury cars, watches, high-end ready-to-wear, and outerwear. Leather goods and jewelry, which are more female-oriented categories, could also benefit, but more through gifting demand than direct consumption.

$CSU.to

"Code is not the hard part. Selling software to a risk-averse institution, passing security/compliance reviews, integrating with legacy systems, training staff, and earning enough trust to become deeply embedded in workflows. That’s the hard part."

https://t.co/puoNmwmNB4

The FT piece on Chris Hohn is good. While MM funds are gobbling up more and more dollars for market neutral strategies playing quarters, you have a British guy with 6 analysts running $70 billion and kicking ass for 2 decades with 9 year holding periods and 15 stocks total.

Chris Hohn did a 90-minute sit-down with Nicolai Tangen and then dropped an investor letter the FT got hold of last week.

You’d think the guy who printed a record $18.9B last year would be doing victory laps. Instead he’s quietly rewiring his whole portfolio.

My favorite takes from both:

1.The most important thing in investing isn’t growth. It’s barriers to entry. Growth without a moat is the airline industry: 5% volume growth for 100 years and basically zero cumulative profit.

2.There are only about 200 companies on earth he considers high-quality and investable. His fund holds 15.

3.Average holding period: 8 years. Some positions 13. “You have to hold the company forever, because the stock market may be at very bad prices when you want to sell.”

4.His real test for a moat: can the company price above inflation? A 20% margin business that prices 1% above inflation grows profits 5% faster than revenue. Forever. Almost no companies can do this.

5. Industries he won’t touch: banks, autos, retail, insurance, tobacco, asset managers, fossil fuel utilities, airlines, wireless telecom, media, advertising. On banks: “sooner or later someone without a lot of intelligence comes to run them, and then it can be toxic.”

6.On AI generally: call centers go bankrupt. Indian outsourcing coders are next. But for everyone else, AI lowers costs and raises productivity. Companies with real moats become MORE valuable.

7. Here’s the punchline. The FT got hold of his investor letter. He cut his Microsoft stake from 10% of the fund to 1%. Roughly $8B sold. He’d held it since 2017 through a 400% rally. His reason: AI could disrupt Office and Azure faster than the market thinks.

8.He moved that capital into Alphabet. Doubled it from 3% to 5%. Now his largest tech position. The world’s best quality investor sold Microsoft and bought Google because he thinks Google’s moat is more durable in an AI world. Not the consensus trade.

9.The underlying thesis: “AI eats software.” If AI agents do the work humans used to pay per-seat SaaS licenses for, the whole SaaS model gets re-rated. Oracle, Adobe, Salesforce all ~40% off highs. Microsoft 25% off. Market is starting to agree.

10.When to sell? Not when something gets expensive. When conviction drops. Valuation is one variable, conviction is the other. What kills you isn’t being wrong, it’s permanent loss of capital.

11.He admits hardcore activism doesn’t work anymore. Too much of the shareholder base is passive index funds. And even when activism wins, you usually win in a bad business. “The business always wins.”

12.Counterintuitive take: there are more good companies in public markets than in private equity. The best businesses are too big for PE to buy. And when public companies sell something to PE, they’re selling the assets they want to get rid of.

13.On intuition: “thinking without thinking.” Pattern recognition from 20 years of reps. It’s how he sniffed out Wirecard while the German establishment was defending it. “Most investors trust authority too much.”

14.He basically stopped shorting. “You’re going to be eventually right but not be able to fund the losses.” The first guy to short Wirecard had to cover 19 years before it hit zero. Buffett told him he and Charlie studied shorting and concluded it was too hard.

15.He gives almost everything away. ~$500M a year. $10 prevents an unwanted pregnancy in Africa. $40 saves a child from severe malnutrition. $50 prevents permanent blindness.

16.Tangen asks: advice to young people? Hohn, who runs the world’s most profitable hedge fund: “Go on a spiritual path.” The guy who made $18.9B last year ends the interview saying only purpose and meaning matter.

The headline: the world’s best quality investor just sold his biggest tech compounder because he thinks AI is breaking the moat. Quietly, with conviction, on an 8-year horizon, while everyone else is still buying the AI winners of 2023.

Die einzigartige Kultur von Constellation Software ( $CSU) in einer Fußnote zusammengefasst:

Der neue Präsident Mark Miller verzichtet ab 2026 freiwillig auf #Gehalt und Bonus – genau wie der Gründer Mark Leonard.

Mark Miller besitzt rund 1,2 % des Unternehmens. Er möchte dessen Wert steigern.

Wo sonst findet man Manager mit so viel "Skin in the game"?

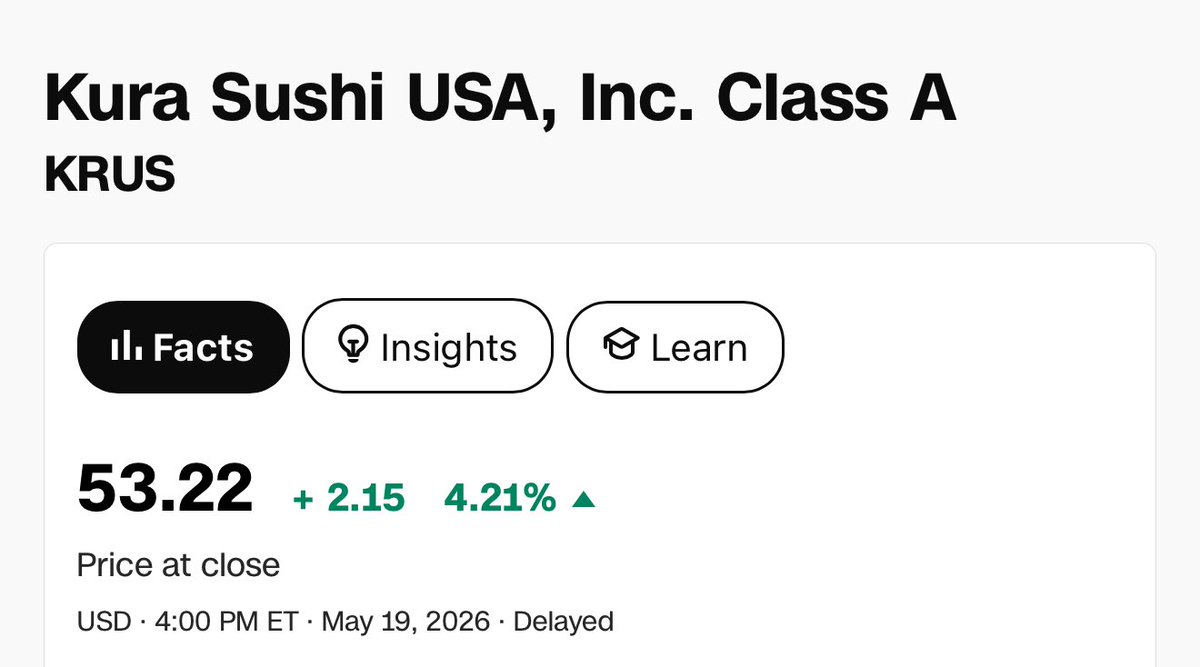

wait a second

Trump just bought $5m (1%) of a Sushi train restaurant chain because he got it mixed up with another AI company (FujiKura)

can’t make this up 😭

The amount of cognition that we are offloading to AI will lead to a massive crisis in education and corporate work

In the future, CEOs will feel uncomfortable promoting young folks because they never developed fundamental skills and just gave it all to AI instead

We are not preparing the next generation for what is coming

Yes, the United States has the most progressive tax system in the world. The top 1% pay 40% of taxes, the bottom 50% pay 3% of taxes. We can make it even more progressive by zeroing out taxes on the bottom half. It’s a small amount of the total tax revenue but very meaningful to people in this group.

NAILED IT: Jeff Bezos: “A nurse in Queens who makes $75K a year pays more than $12K a year in taxes. Does that really make sense?”

“So people talk about making the tax system more progressive. How about we start by having the nurse in Queens NOT pay taxes? At all!”

“Why is a nurse in Queens who makes $75K a year paying more than $1K a month in taxes?”

“That’s $1K a month that could help with rent or groceries or anything.”

“And by the way, do you know what that all adds up to? The bottom half of income earners in this country pay only 3% of the taxes. It’s only 3%.”

“We can find 3%. So we don’t have... it’s a small amount of money for the government. You know that. And the more I thought about it, to me, it’s kind of absurd that we’re doing this.”

“We shouldn’t be asking this nurse in Queens to send money to Washington — they should be sending her an apology. It really makes no sense.”

Exactly!

Gavin Baker on why the AI bubble talks might be overblown this time around

"I am optimistic that we may avoid a bubble this time. The reason we are going to avoid it is because we have fundamental shortages of watts and wafers."

The supply side is so constrained while demand continues to grow exponentially. This is nothing like the dark fiber of the dot com era where build out was happening with the expectation of demand on the other end.

The demand is already here. Today. It is happening now in AI.

Investors have never used this much leverage:

US margin debt surged +$83 billion in April, to a record $1.3 trillion.

Over the last 12 months, margin debt has risen +$453 billion, or +53%.

As a result, margin debt is up to a record 5.2% of US GDP.

This is ~3 percentage points above both the pre-2008 Financial Crisis level and well above the 2000 Dot-Com Bubble peak.

Market leverage is through the roof.

@moneyandmore72 Found the manager of the Blue whale growth fund take interesting on the underperformance of his quality competitors. He mentioned something along the lines of that they look at past quality/ performance rather than future. Some of them are also bad at selling.

@TokyoDeepValue Japan debt is 260% of GDP. Most of those companies have no plans in returning that cash. Some are subsidiaries that can't really decide on what to do with it.

There's a few decent ones.

Probably the best take I have heard on why there is so much fear around software exposure in private equity and credit because of AI

From David Sacks

"Historically we only had two good exits for software businesses. One was IPO. The other was M&A. Then these big private equity shops came along and gave us a third potential exit. You would sell to them and then they would raise the capital based on one third equity and two third debt. So it was debt financed buyouts.

It is something that has been around in the non technology part of the economy for a long time but was a relatively new entrant in the world of technology. And the reason for that is if you have debt financed a purchase, you need to have very stable cash flows.

Because if you miss and you cant pay your interest on the debt, you will lose all your equity because the debt holders will foreclose.

It was belief for a long time that software did have predictable cash flows, at least for the mature businesses."