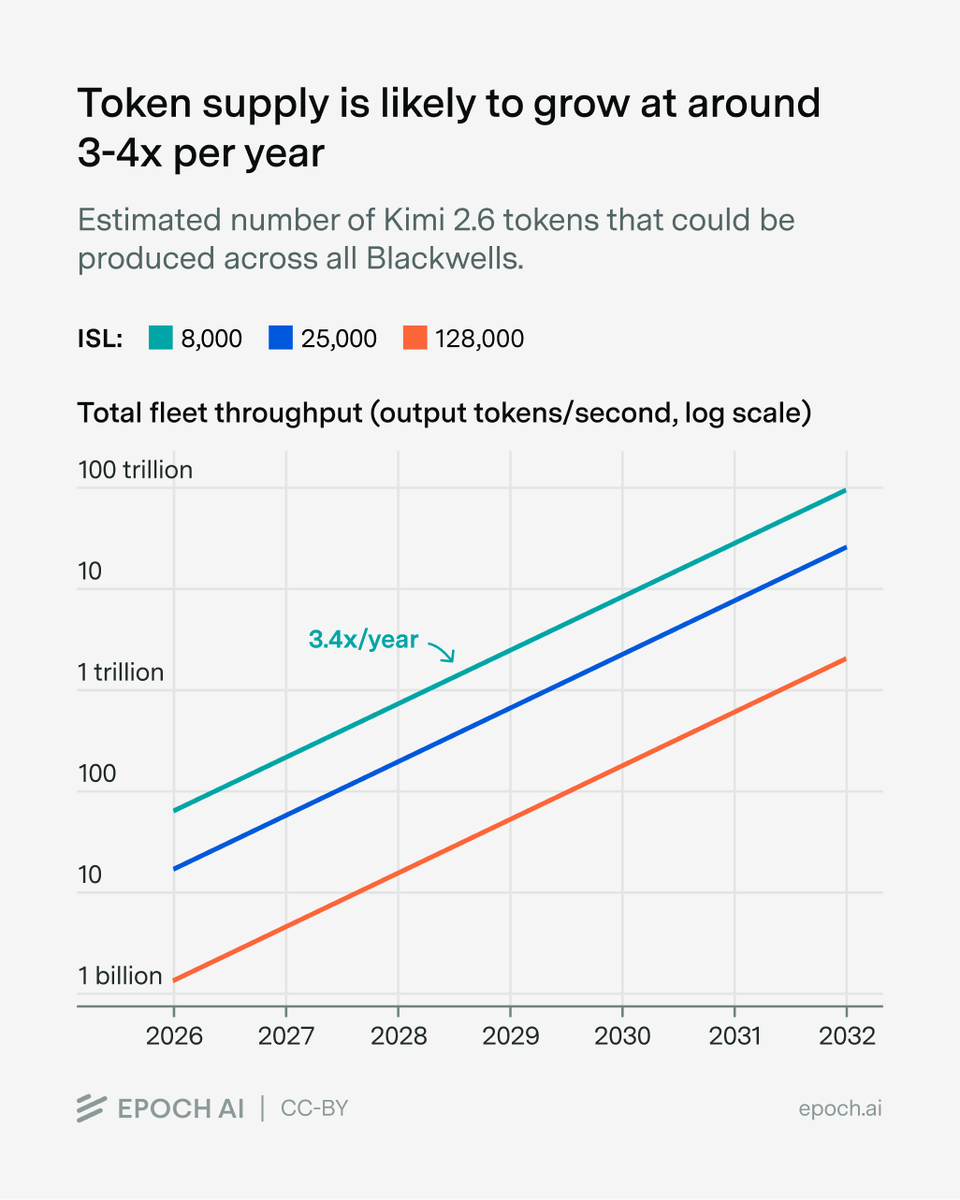

Are we nearing a compute crunch?

In our latest Gradient Update, @luke__emberson and @Jsevillamol estimate how many tokens all the Blackwell chips on Earth could serve, and compare this to total token demand. Direct comparisons are difficult, but it appears demand is growing much faster than supply.

A couple of weeks ago, @Bloomberg reported that TSMC won't buy ASML's newest chipmaking machine until at least 2029.

ASML's High-NA EUV is the most advanced lithography tool ever built.

When the world's #1 foundry passes, that's a strong signal.

Today's @exponentialview analysis w @hannahjpetrovic

https://t.co/7KKs9g0JMa

Over the past week, I have been in China meeting AI and robotics teams, including Zhipu and MiniMax (the two publicly listed foundation model companies), as well as Kimi, Alibaba, Xiaomi, Bytedance, and others.

Demand is booming. Zhipu, for example, is serving 5.5 trillion tokens per day. Developers are rushing to the platform, joining at about ten a minute. Keeping up with inference loads is a struggle in China, as it is in the US. Teams universally acknowledged compute constraints, particularly the shortage of Nvidia chips. But that isn’t stopping innovation under those constraints.

Researchers and developers are free to use whichever model they want. Anthropic’s Claude was the preferred choice for technical teams, but it was clear that “dog-fooding” is commonplace.

I'll write something in more depth in the next couple of weeks. For now, here’s a short video from one of the many demos we saw at Unitree:

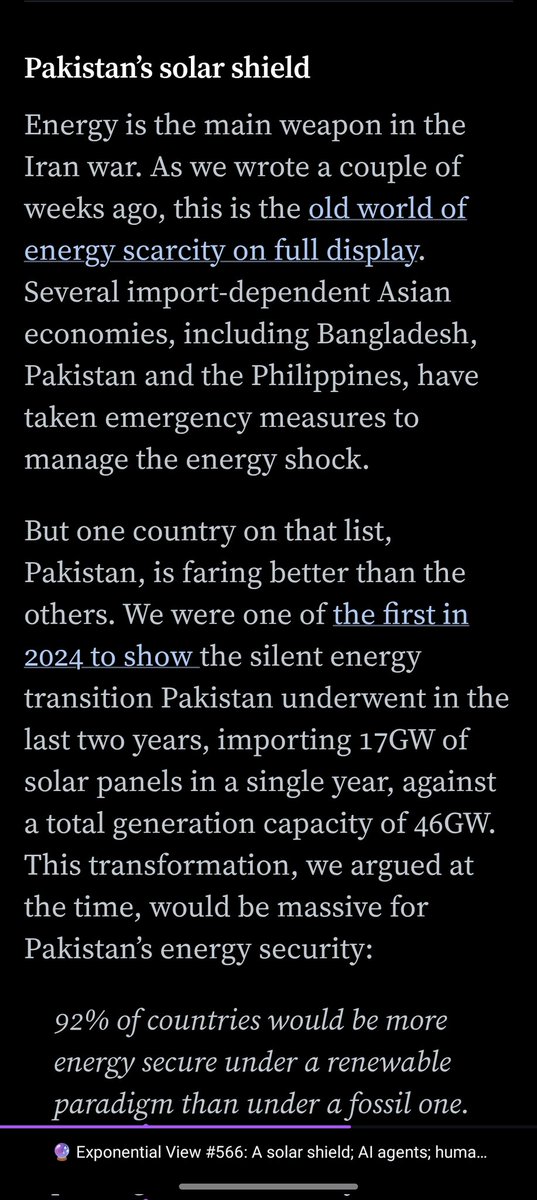

Pakistan's people installed solar panels in record numbers because their government couldn't be trusted to keep the electricity on...

As a result, Pakistan hasn't been as badly hit by the Iran war as other similar countries, argues @ExponentialView

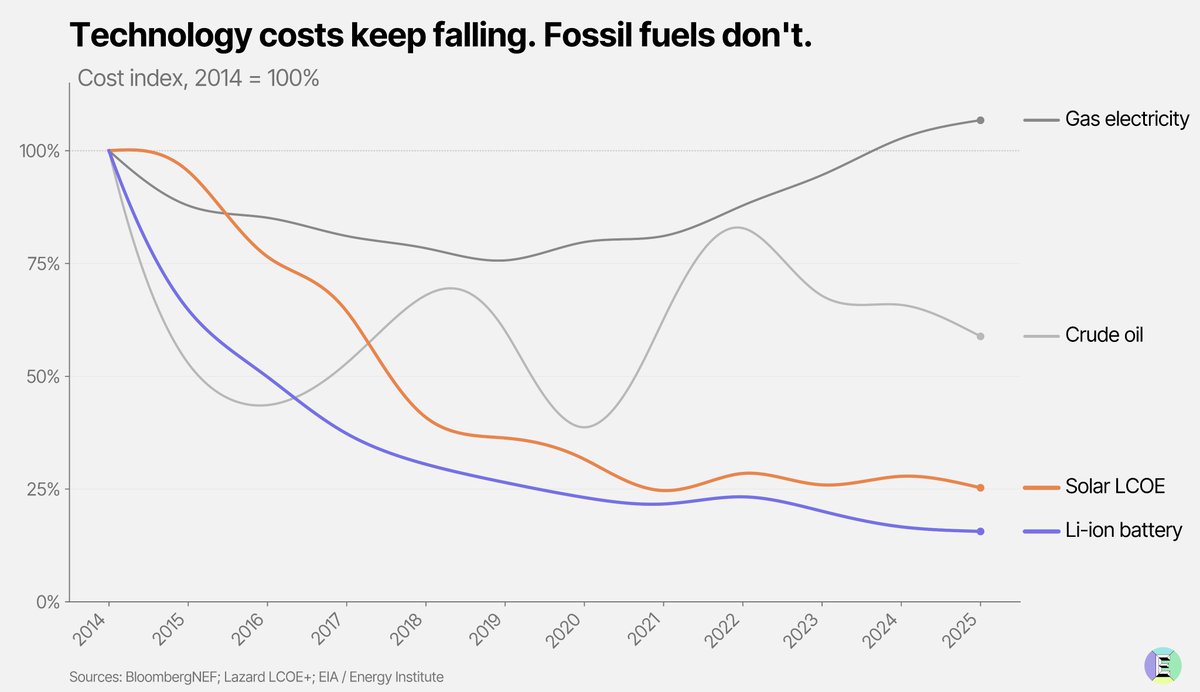

Chinese renewable energy is far more ambitious than just EVs or grid electrification.

This interactive chart from @ExponentialView by @azeem is a great way to see it: as solar gets cheap enough, it does not just take share in power generation. It starts to make entire incumbent systems vulnerable. Readers can play with the assumptions on the original site and see how quickly the timing changes.

A few examples of what ultra-cheap solar can start to unlock:

Grid power is the most obvious one. Global electricity generation reached about 30,900 TWh in 2024, and solar still provided only 6.9% of it, which shows how early we still are.

Aviation fuel is another. Global airlines’ fuel spend was projected at about $291 billion in 2024 and $248 billion in 2025, so this is already a roughly $250 billion to $300 billion annual market at current fuel prices.

Industrial heat may be even more important. Industry accounts for nearly 40% of global final energy demand, and much of that energy is used in heat-intensive processes. That implies an enormous incumbent fossil energy market, plausibly well above $1 trillion a year on a rough back-of-the-envelope basis.

Green hydrogen is especially interesting because it first displaces existing fossil hydrogen demand in refining and ammonia, and then could move into much larger industrial systems like steel. It is already being piloted at scale, and there are strong reasons to think it will ramp seriously over the next decade.

And then there are areas like desalination and carbon capture, where the value is harder to summarize as a single market number but could be enormous in social and economic terms.

Link to the chart in the comments. It is worth playing with the assumptions yourself to see when different cost thresholds start to make these incumbent systems vulnerable.

Solar does not care about the Strait of Hormuz.

Oil flows through chokepoints. Solar follows a learning curve.

Great piece @azeem

https://t.co/QqddYuyh9a

We are living through the solar supercycle, the self-reinforcing loop in which every cost reduction of solar opens a new market and every new market funds the next cost reduction which opens the next market.

https://t.co/9NF5DMnd9r