$TVK.TO Q2 FY2023 Review now published. Strong organic revenue growth driven by increased oil & gas activity in Western Canada. Better-than-expected fundamentals have led to a change in my intrinsic value estimate. Read my review below.

@airindia my wife and 12 month baby travelled to India on 27th September. Even after booking a bassinet seat, we did not get a bassinet for our baby. My wife literally had to stand or sit on the floor for a large part of the flight. Other passengers with babies had to do the same. To add to our ordeal, our bags with our baby’s medicines and milk supply never showed up at the destination. Just is entirely unacceptable standard of service. Do better!

$ZZZ.TO is up 25% since I published my report and initiated a position in April. I've exited my position today since I've got no more margin of safety when compared to my intrinsic value estimate.

Checking if there interest for a deep dive on $TOY.TO Spin Master. Good ROIC. Loads of cash to allocate. H2 2022 was bad. Valuation seems okay. No idea on management right now.

@marketplunger1 I would also like to add that I don't focus on finding multi baggers. That is an extremely tough job to do, and involves significant luck. I'll the take small mis-pricings as wins.

There have been times when I've done research and not even bought the stock. haha I'm driven by intrinsic value. However, the knowledge built through studying the stock stays with me for the longer term. It might come back down, a comparable company might become cheaper, a PR mistake might lead to the stock being battered. I'll still be looking out. You may also find some of reasoning here: https://t.co/k9WVS3HZw7

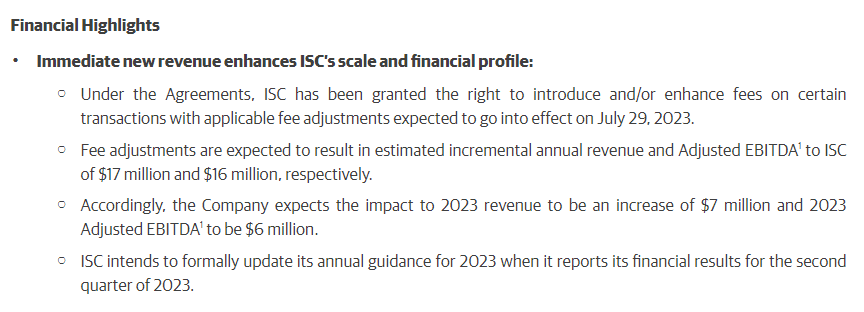

@NathanTee3@atelicinvest You are only considering the incremental ebitda. This agreement also ensures that the current registeries business monopoly remains in place for 30 years. The combined return on capital would make alot more sense.

I have been to several indigo stores in the past year and this is just observation: they are almost always empty (else than Eaton Centre). The prices are higher for everything. They have alot of inventory of stuff they should not be selling (candles and pillows). Just my view though.

@NamelessAnalyst I get where you are coming from but I don’t fully agree. The risk and return on retail real estate assets might be very different from say mattress retailer’s business itself. Yes they use the asset, but in reality they pay the rent for the use.

Leases are no longer classified as an operating expense but instead accounted for as depreciation of right-of-use assets and interest on leases. If you are comparing long-term financials you might see improvement in EBITDA margins, but it is not an apples-to-apples comparison.