Agreed. If we are not at the top, we are very close. But who knows, this can go longer. One thing is for sure long term returns from here looks much bleaker from here.

My cash position is more than ever. 'Be greedy when everyone is fearful, be fearful when everyone is greedy'

I might be wrong on this, but in the future we might look back and think that there were evident topping signals...

1) Hyper-concentrated portfolios around one theme

2) Leveraged thematic ETFs everywhere

3) Sell side upgrading companies based on 13Fs

4) YTD screenshots daily

5) 13Fs moving stocks double digits

6) Stocks that are up 20% YTD categorized as "not moving"

7) People believing that under no circumstances can the AI trade falter

8) PTs based on "vibes"

9) Luxury car dealerships in Korea full

Probably very wrong on this and I do think AI is real and game-changing tech, but looks a lot like past tops

As two of the largest forces in equity markets -- growing index ownership and increasing amounts of capital controlled by extremely short-term-oriented, leveraged, volatility-intolerant investors -- converge, we have found occasional opportunities to acquire some of the most dominant long-term compounding franchises at attractive valuations.

For example, we acquired Alphabet $GOOG when the stock declined substantially on the release of ChatGPT in late 2022, Amazon $AMZN in the weeks following Liberation Day, and $META more recently on the market's response to the company's unexpectedly large cap ex guidance and expenditures.

In our 13F which we will file later today, we will disclose a new position in Microsoft, a company we have followed for many years now offered at a highly compelling valuation. While $PSUS will not be filing a 13F tomorrow, it has also recently made $MFST a core holding.

Microsoft operates two of the most valuable franchises in enterprise technology, which account for approximately 70% of the company's overall profits: M365 and Azure.

M365, the company's productivity suite, is the dominant operating platform for knowledge work, with over 450 million workers using Word, Excel, PowerPoint, Outlook, and Teams on a daily basis.

Azure is the world's second-largest hyperscaler cloud platform and, like AWS in our Amazon investment, is a direct beneficiary of the multi-decade migration of enterprise IT workloads to the cloud, which is now further accelerated by surging demand for AI inference workloads.

Both M365 and Azure are underpinned by Microsoft's unparalleled enterprise distribution and the security, compliance, and identity infrastructure it has built and refined over decades.

Beyond these core franchises, Microsoft also owns a portfolio of other leading businesses, including LinkedIn (the world's largest professional network with 1.3 billion members), its gaming platform (Xbox and Activision Blizzard), and search and news advertising (Bing and the Edge browser).

We began building our position in MSFT in February following a meaningful share price decline after the company reported its fiscal Q2 2026 results. We were able to establish our position at a valuation of 21 times forward earnings, broadly in line with the market multiple and well below Microsoft's trading average over the last few years.

Notably, MSFT's headline multiple does not reflect the value of Microsoft's approximately 27% economic interest in OpenAI, which would represent approximately $200 billion, or 7% of Microsoft's market capitalization, at OpenAI's most recent funding round valuation.

We believe Microsoft's recent share price decline has been principally driven by investor concerns around two key issues: i) the competitive positioning of M365 against increasingly capable AI lab offerings (notably Anthropic's Claude Cowork), and ii) the durability of Azure's growth, especially in light of Microsoft's evolving relationship with OpenAI.

In our view, investors underestimate the resilience of the M365 franchise given its deeply embedded role across enterprises and highly attractive price-value proposition. Unlike point software solutions, which may be vulnerable to disintermediation by better-performing AI alternatives, M365 is tightly integrated into the daily workflow of nearly every large enterprise and is supported by Microsoft's identity, security, compliance, and data governance infrastructure, which would be nearly impossible to replicate.

Attractive bundle economics further reinforce Microsoft's advantage, with monthly average revenue per user on the M365 suite at approximately $20, less than half of what customers would pay to purchase the underlying applications individually from different vendors.

Moreover, we are encouraged to see Microsoft prioritizing its R&D efforts and investment in Copilot, its own AI agent embedded across M365, with direct involvement from CEO Satya Nadella. We believe these efforts will translate into improved product velocity and greater customer adoption over time.

Alongside Copilot's rollout, the company has also begun shifting its pricing model from pure per-seat licensing to a hybrid model of seats plus metered consumption, which helps expand the company’s revenue opportunity as AI agents drive incremental usage that a seat-only structure would not capture. These initiatives should help sustain M365’s strong underlying growth momentum, which was already evident in the business unit’s 15% revenue growth (in constant currency) last quarter.

We believe concerns regarding Azure's growth trajectory are similarly misplaced, particularly in light of the franchise's exceptional recent performance. Azure revenue grew 39% in constant currency last quarter, with company guiding to modest acceleration through the second half of the year.

We view Microsoft's recent decision to restructure its OpenAI partnership not as a concession but as part of a deliberate pivot toward a more open, multi-model architecture that better serves enterprise customers, who increasingly seek optionality across model providers.

Microsoft recently disclosed that over 10,000 enterprise customers have used more than one model on Azure Foundry, the company’s modular AI model marketplace. This model-agnostic approach also strengthens Copilot, which can auto-route queries across multiple models to deliver the optimal output for a given task.

To support Azure's rapid growth amid persistent supply constraints, Microsoft has raised its calendar year 2026 capex budget to approximately $190 billion. Consistent with what we have observed at hyperscaler peers Amazon and Google, we view this spend as growth capex that should drive future revenue generation. This is particularly true for Microsoft, given that roughly two-thirds of its capex budget is allocated to server and networking equipment that correlates directly with near-term revenue.

Like our purchases of $GOOG, $AMZN, and $META, we believe that $MSFT offers analogous and compelling long-term value at today's valuation.

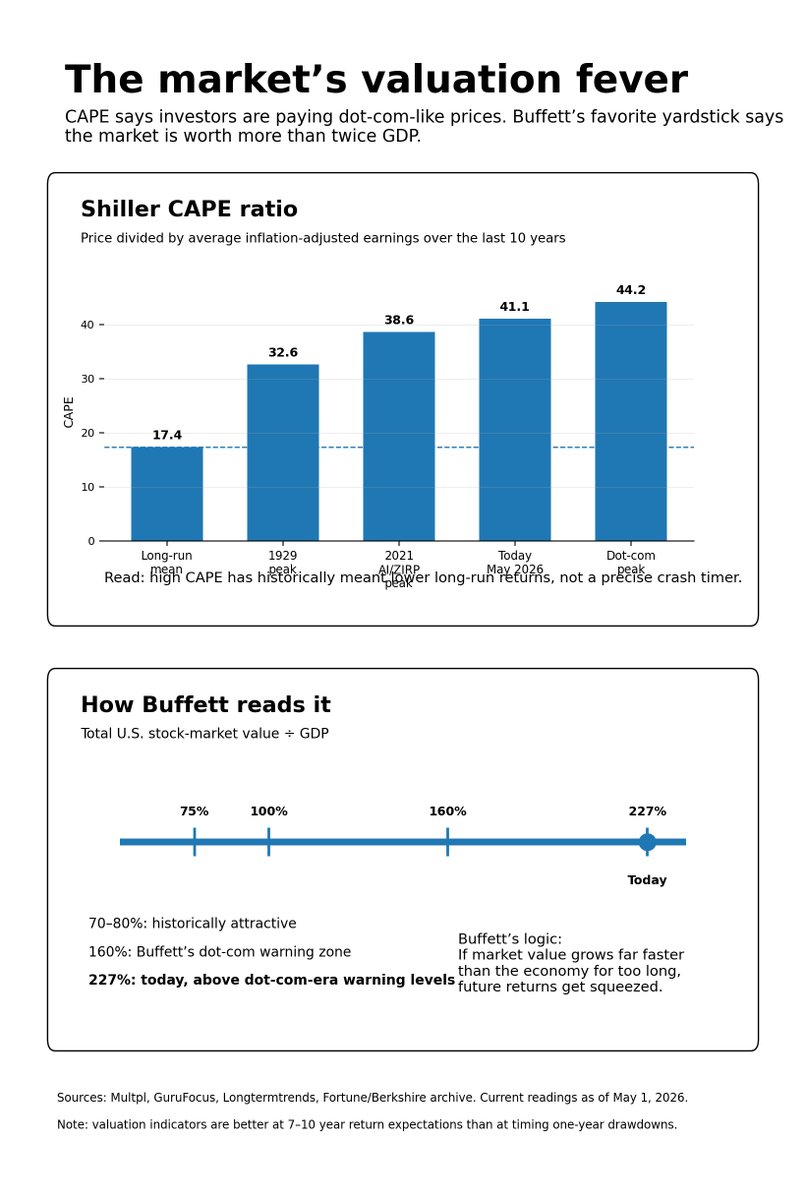

Let me explain exactly why Buffett is sitting on $373B in cash despite a market up 72% in 5 years, because the "he missed it" frame doesn't square with the math.

The Shiller PE just printed 41.06. The only time it's been meaningfully higher in 144 years of data was the 1999-2000 dot-com peak. Higher than 2007. Higher than 1929. After March 2000 the S&P drew down 49% over 30 months and didn't recover until 2007.

Warren's playbook when valuations stretch has been the same three times in a row.

1969: He shut down Buffett Partnership Ltd. and returned capital to investors, saying he couldn't find anything worth buying. The Nifty Fifty crashed 45% over the next 5 years while he sat in muni bonds.

1999: Berkshire's stock dropped 19.9% while the S&P gained 21%. Barron's ran "What's Wrong, Warren?" on the cover. Then the dot-com unwind hit and Berkshire crushed the index for 3 straight years.

2007: $44B in cash at the peak. Deployed during the 2008-2009 panic into $5B Goldman preferred at 10% with warrants, $3B GE preferred at 10% with warrants, and the 2011 BAC deal that turned a $5B preferred into roughly $30B in realized value. Three deals nobody else on Earth could write the check for.

Now run the math on the current pile. $373B in T-bills at 3.68% generates $13.7B per year in risk-free interest. Berkshire's average annual operating profit through the 2000s ran around $8B. The cash position alone is throwing off more income than the entire company used to produce.

The bull case for full equity exposure today is real. AI capex inflecting, nominal earnings growing, momentum compounding. Sounds attractive until you ask what game Warren is actually playing. His job is to be the buyer when somebody desperate needs liquidity at minus 40%. The only currencies that game requires are patience and capital that doesn't redeem.

Berkshire has both. And $13.7B per year while waiting.

The trade was never even close.

I’ve been thinking a lot about AI, chips, and all these other hot poplar industries and ai keep coming back to a pretty uncomfortable conclusion. Ten years from now, most of the companies people are excited about today will not work out as investments. Not because the technology isn’t great or the people arnt amazing, and not because demand won’t be massive. But because great technology and great returns are not the same thing.

We’ve seen this before in then1990s, everyone knew the internet would change the world, and they were right. What they got wrong was who would actually make money and more importantly who would earn high returns on capital because the future economics were unclear.

There’s a simple reason this keeps happening. The more important a technology is, the more capital flows into it, and the more capital flows into it, the harder it becomes to earn excess returns. Everyone builds, everyone expands, everyone competes, and the economics get spread thin over time. You end up with an incredible industry and very average investments.

I think AI is setting up the same way. There will absolutely be winners, and the obvious place to look today is the hyperscalers like $AMZN, $MSFT, and $GOOG, perhaps $META, because they have distribution, cash flow, and the ability to invest at a scale others can’t. Even then nothing is guaranteed, but at least the logic holds.

Where I struggle is when people assume every part wins at the same time. Chip designers, manufacturers, neo clouds, and AI applications are all raising capital and racing to grow. That sounds exciting on the surface, but it also means competition is increasing exactly where people expect the most profit. Usually capitalism doesn’t reward that evenly, again we’ve already seen this movie.

If you break it down, each layer has its own challenge. Semiconductors require massive capital and constant reinvestment just to stay relevant. Cloud platforms may win, but pricing pressure and competition will naturally compress returns over time. AI applications have no moat, with low switching costs, and many of these “neo” infrastructure players are dependent on what looks promising today but the economics are difficult to foresee 3-5 years out.

There’s a simple framework I keep coming back to. Value tends to concentrate in only a few places, the customer relationship, the lowest cost producer, or the bottleneck that acts like a toll bridge. Everything else ends up competing away its profits over time. The question is not who participates in AI, but who actually owns one of those positions.

This is where most investors get tripped up. Investing isn’t about how big something becomes, it’s about what return that business earns on the capital it reinvests. You can grow quickly for years and still be a poor investment if all that growth requires constant spending just to keep up. At that point, you don’t have a compounding machine, you have a treadmill (this is a quote from my book).

And treadmills are dangerous when expectations are high. Because the moment investors realize returns won’t match the story and more important the expected economics, the repricing isn’t gradual. It’s fast, and it’s brutal (ie $TTD), and it usually catches people off guard. That’s how you get 70% or 80% drawdowns in companies that still look like they’re “winning.”

If you own five or six companies across the same AI value chain, you’re implicitly betting they all earn high returns. History suggests that’s unlikely. You might be right on the theme and still wrong on the outcome. That’s a tough lesson, but it’s a real one we all should think about.

I could be wrong on who the winners are, but I’m very confident most won’t be. That’s not pessimism, it’s just my opinion that’s backed by pattern recognition. If it walks like a duck and quacks like a duck, it’s probably a duck. We’ve seen how this plays out when capital floods into something important and everyone tries to win at once.

🌹

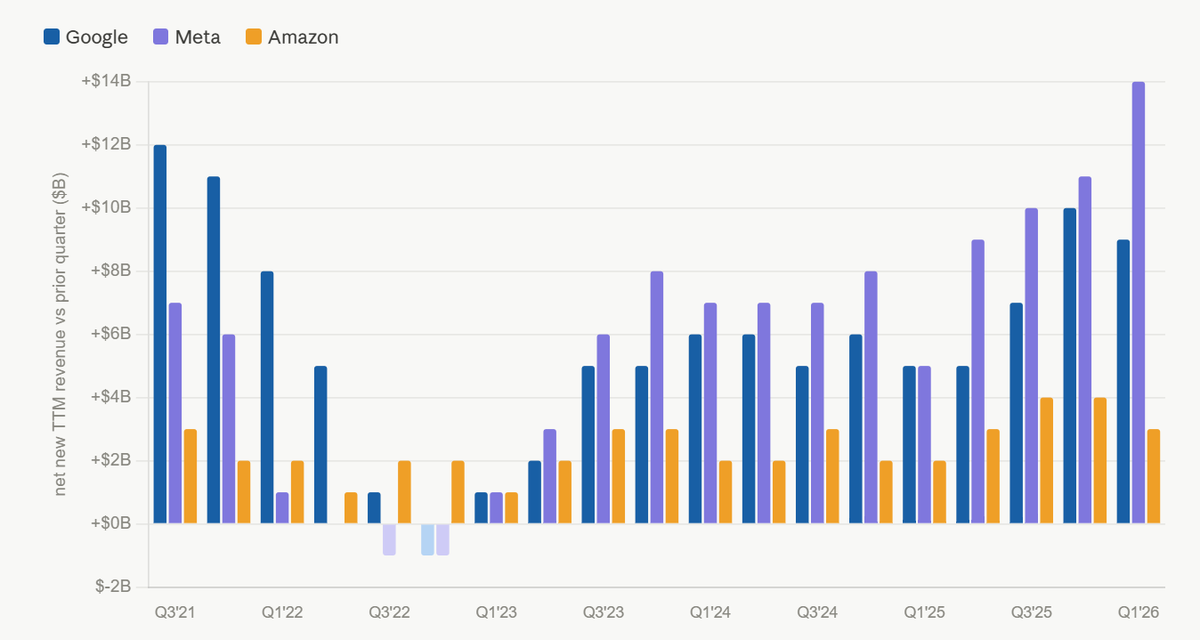

$META incremental net advertising revenue additions hit an all time high, by far, into a seasonally weak quarter (Q1).

They also increased ad revenue significantly more than $GOOG and $AMZN.

Incredible.

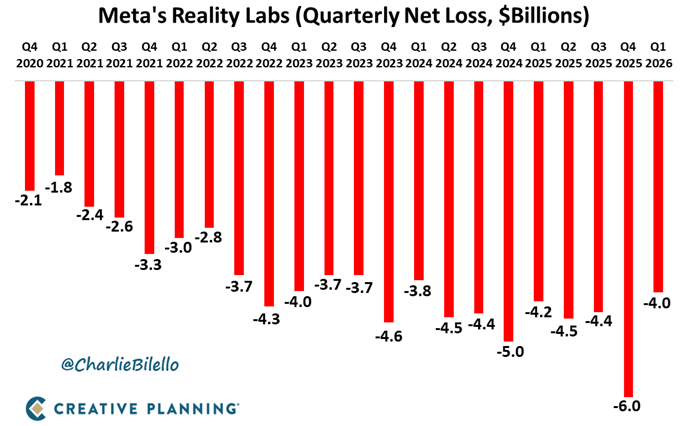

$meta is burning money because they can. $meta can produce more than 83 bil of FCF in a year if they want to. They are spending all of their money on Capex because they can, not because they need to. There is a difference!

Meta's Reality Labs unit lost another $4 billion in Q1, bringing its cumulative losses since 2020 up to $83 billion. We've never seen a public company light money on fire to this extent. $META

I remember at this time last year $googl $goog was priced as if it was going bankrupt!

Up 157% from last years lows.

I was tweeting everyday about $googl being cheap. Havent sold a single share till now.

I just did a 2 hour live stream with my Patreon going over $MSFT, $META, $AMZN and $GOOG earnings.

TLDW;

$META looks like the cheapest stock (lowest price, fastest growth).

$GOOG is selling for a premium, but deservedly so.

$AMZN is also undervalued.

$MSFT lagging in cloud.

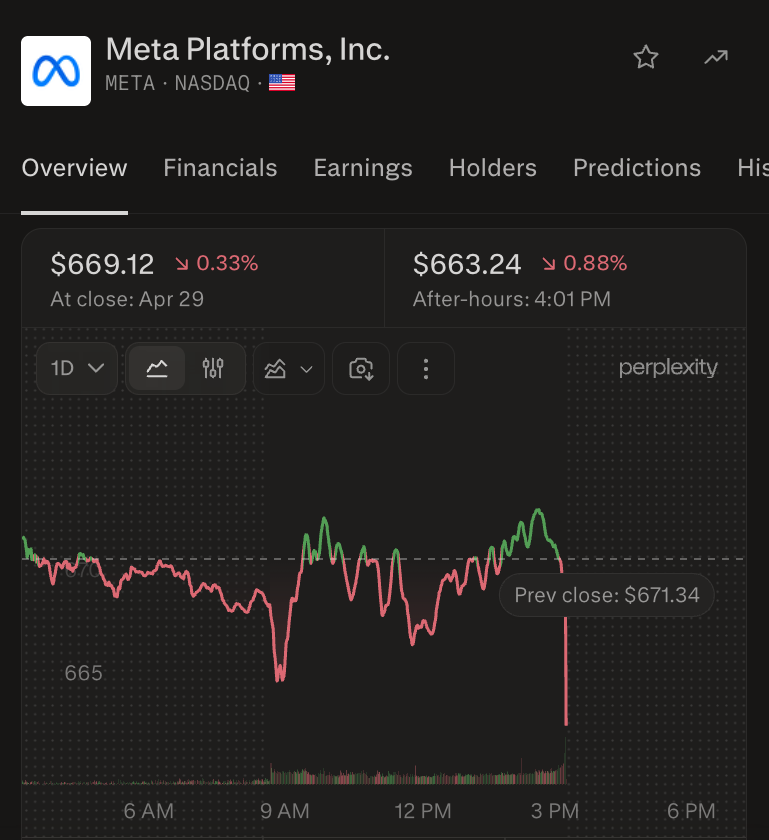

$META is down 6% because of the capex guide. Deja vu: We saw this when they reported Sep-25.

Capex is expected to grow this year by 94%, vs. the Street was expecting 76%.

My take: I continue to be surprised by investors negative capex reaction. We have enough datapoints from Meta that show these investments are paying off. Revenue in March grew at 33% yy, and they guided to 28% in June. That compares to March of 2025 up 16%.

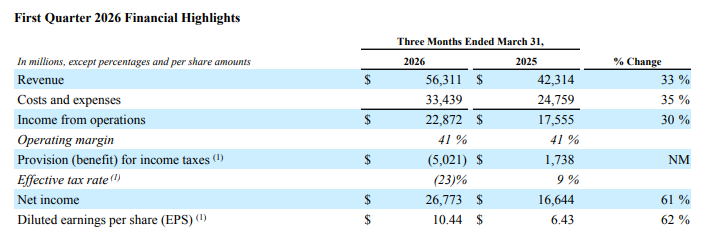

$META Platforms Q1'26 Earnings Highlights

🔹 Revenue: $56.31B (Est. $55.36B-$55.5B) 🟢; UP +33% YoY

🔹 EPS: $10.44 (Est. $6.67) 🟢; UP +62% YoY

🔹 OI: $22.87B (Est. $19.4B) 🟢; UP +30% YoY

🔹 FY26 CapEx: $125B-$145B (Prior: $115B-$135B; Consensus: ~$125B)

🔹 DAP: 3.56B; UP +4% YoY

Guide:

🔹 Q2 Revenue: $58B-$61B (Est. $59.5B) 🟡

🔹 FY26 Total Expenses: $162B-$169B; unchanged from prior outlook

🔹 FY26 Operating Income: Expected above 2025 operating income

🔹 FY26 Tax Rate: 13%-16% for remaining quarters

Q1 Segment:

🔹 Advertising Revenue: $55.02B (Est. $54.4B) 🟢; UP +33% YoY

🔹 Family of Apps Revenue: $55.91B; UP +33% YoY

🔹 Family of Apps Operating Income: $26.90B; UP +24% YoY

🔹 Reality Labs Revenue: $402M; DOWN -2% YoY

🔹 Reality Labs Operating Loss: ($4.03B) (Est. Loss ~$5.0B) 🟢

Other Metrics:

🔹 Ad Impressions: UP +19% YoY

🔹 Avg. Price per Ad: UP +12% YoY

🔹 Headcount: 77,986; UP +1% YoY

🔹 CapEx: $19.84B

🔹 Operating Cash Flow: $32.23B

🔹 Free Cash Flow: $12.39B

🔹 Dividend & Equivalents: $1.35B

🔹 Cash, Equivalents & Marketable Securities: $81.18B

Financials:

🔹 Costs & Expenses: $33.44B; UP +35% YoY

🔹 Operating Margin: 41%

🔹 Net Income: $26.77B; UP +61% YoY

🔹 Income Tax Benefit: $8.03B

🔹 EPS Impact From Tax Benefit: $3.13

🔹 Long-Term Debt: $58.75B

CEO Commentary:

🔸 “We had a milestone quarter with strong momentum across our apps and the release of our first model from Meta Superintelligence Labs.”

🔸 “We're on track to deliver personal superintelligence to billions of people.”

🔸 FY26 CapEx outlook increased to $125B-$145B, reflecting higher component pricing and additional data center costs to support future year capacity

🔸 Meta continues to monitor active legal and regulatory matters, including EU and U.S. headwinds that could significantly impact business and financial results

Q1 earnings are in: 2026 is off to a terrific start.

Our AI investments and full stack approach are lighting up every part of the business: Search queries are at an all-time high with AI continuing to drive usage. Google Cloud revenue grew 63%, Gemini models have incredible momentum, and it was our strongest quarter ever for consumer AI subs, driven by @GeminiApp.

Thanks to our partners + employees around the world. Much more to share on our earnings call in 20 minutes… and at Google I/O in 20 days!

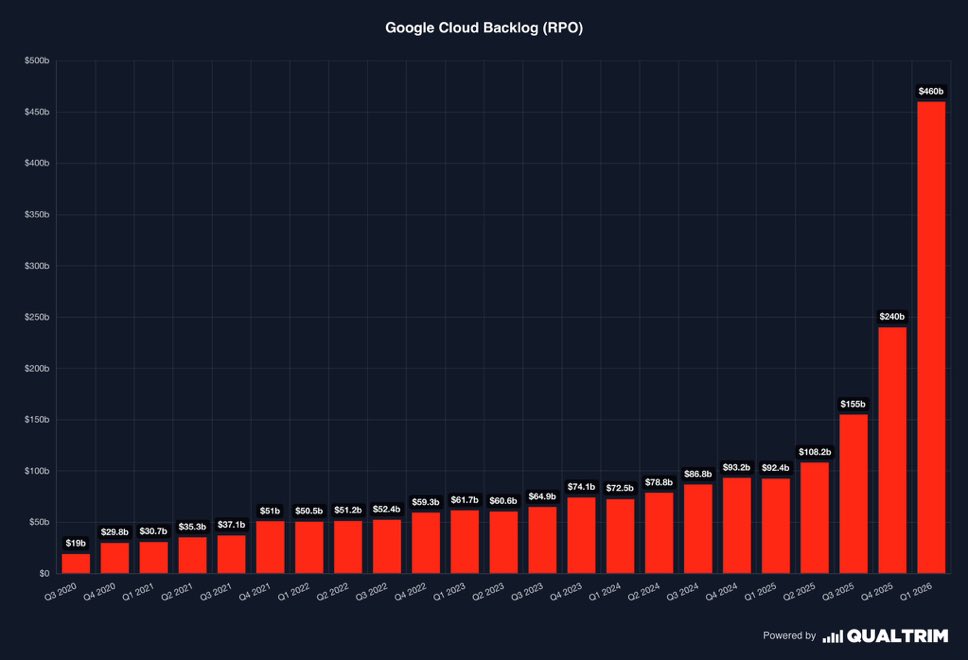

This is the craziest number in all of big tech earnings

$6.6 billion

That is how much GCP is making in one quarter.

They are now at a 33% (!) EBIT margin

y/y that is a whopping 57% incremental margin

Don't really understand how they have THAT much leverage

Insane earnings for $meta!

Stock is down, lol! PE is now closer to 24.

Market is scared of spending. They can reduce spending anytime and there wont be any impact on revenues.

$Meta posted 33% revenue growth

It easy to become blasé at that figure, but remember...

that is more than twice the 16% growth they put up in 1Q25, despite a larger revenue base.

I am a big fan of FIRE

Being smart with your money and building a portfolio to support you during a rainy day is a must today

Rainy days include job loss, health issues, family emergencies etc

Having options in life an the ability to control your time is invaluable

The alternative to FIRE is being chained to a desk till you are 65, and asking another adult to be able to take one week vacation (if you are kucky)

The alternative to FIRE is going through at least one or two job losses over a career, and going through the stress of not having enough to support your family

The alternative to FIRE is losing your job in your 50s, and never finding another job in your field due to age discrimination. Right hwen your kids are about to go to college. And then spending your 60s and 70s having to work a menial minimum wage job

Of course, it is all a balance, requiring trade-offs and calculation of opportunity costs

Seeing that most here on Twitter hate FIRE means it's actually a good idea to pursue

The plot twist is that many today confuse luxuries with needs.

Once you accumulate a decent size portfolio, you may be able to pursue something that truly gives meaning in your life

Having the option to live life how you want is invaluable

That could be traveling more, getting into an occupation you love that is not paid well, spending time with family, raising young kids, or arguing with random people on the internet