AI still can't make investment decisions but it is very good at finding specific ideas and lookalike companies - the kind of stuff that takes forever like going A-Z. If you can just make good decisions I think a lot of the hard work is over, esp as models get better.

Going A-Z through an exchange for ideas could not be a better LLM task - Synthesize a large data set where the cost of a few errors is meaningless.

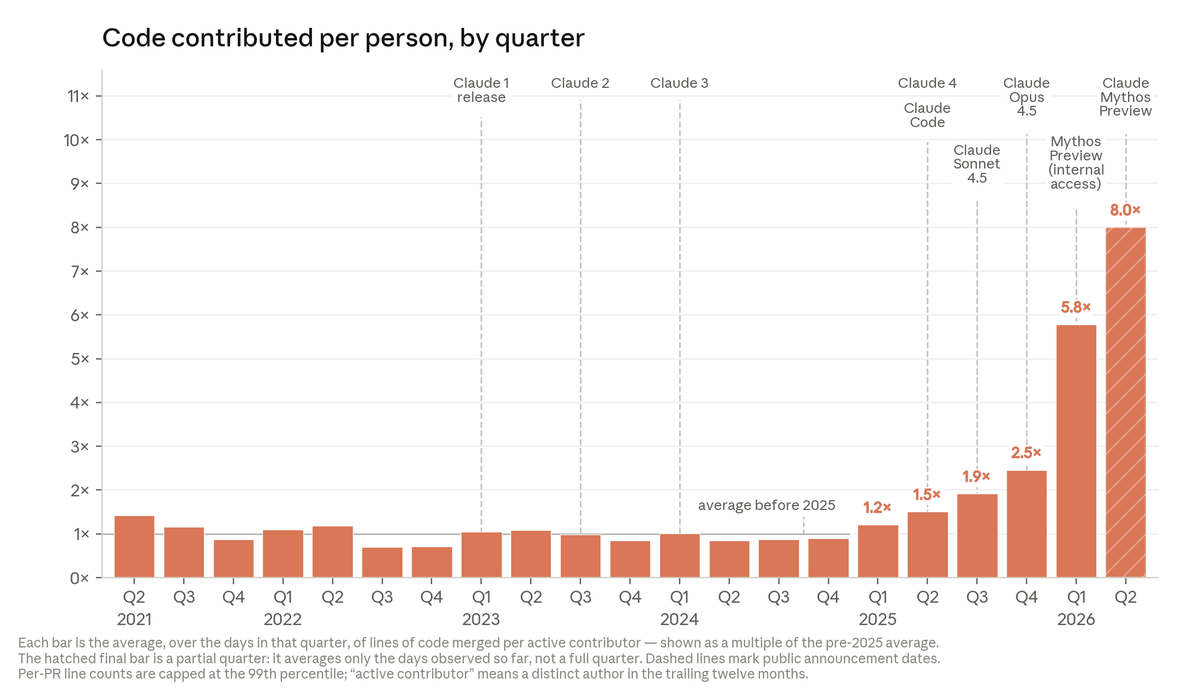

Can even load Claude code with up to date financial data for every stock.

Any one else working on this and getting good results?

$GPW was top of my list for anyone hunting under a $1b market cap. cheap PE, plenty of growth, untapped upside in data sales in a growing economy.

has a public stock exchange ever gone bankrupt?

(not as cheap as it was now)

wrote this one up a while back. a japanese company with a $531m market cap sitting on $520m of cash and $800m of marketable securities.

yes those numbers were right. and they returned cash to shareholders.

rerated a lot since

Li Lu on how to invest under $100k:

interesting one, in Korea there's a form of securities called preferred securities. basically non voting common stock that pay a slightly higher dividend. not much more, but no voting rights.

cheap way to own the same business

Goldman will never mention it because it's small potatoes but if true, this will likely have second order effects for Wafer reclaim services.

more wafers -> more reclaimed wafers

Bullish for RS Technologies $3445.T

BUT... sometimes japanese companies don't raise prices.

Goldman may have just made one of the more important "second-order AI" calls I've seen recently.

It´s not about GPU or CPU ... It's about wafers - specifically, 300mm wafers.

Goldman believes 300mm wafers have entered a multi-year growth cycle driven by AI. AI servers already account for more than 20% of wafer demand, while GPU/ASIC deployments, HBM scaling, CoWoS, silicon photonics, and the rise of agentic AI are increasing semiconductor content across entire systems - not just accelerators. At the same time, next-generation memory architectures such as CBA NAND, 400+ layer NAND, and eventually 3D DRAM could further increase wafer consumption per bit shipped. With supply growth slowing while demand continues to broaden, Goldman sees the setup becoming increasingly supportive for wafer pricing and profitability.

Goldman thinks the industry is moving away from the traditional "shrink more, use fewer wafers" model.

Instead, advanced packaging, stacking, bonding and AI system complexity are causing wafer consumption per unit to rise.

That's a subtle but potentially huge shift.

Potential beneficiaries:

(++) SUMCO (https://t.co/oAG6VEG9h8) – largest estimate increase in the report

(++) Shin-Etsu (https://t.co/l2RQM6lVdz) – stronger 300mm wafer pricing assumptions

(++) Resonac (https://t.co/vZ7iWq6ifB) – AI packaging materials outperforming expectations

(+) Mitsubishi Gas Chemical (https://t.co/0fCEqM6q0k) – BT substrates and AI server materials

(+) Mitsui Kinzoku (https://t.co/OT8gj11OYW) – copper foil increasingly tied to package substrates

Going to release this for free and maybe add a paid tier for Snaptrade broker integration later.

I HATE interactive brokers UI. Also no trackers get IBKR integration right WITH transaction history

Full portfolio tracker with transaction history feature for Interactive brokers through Flex queries which to my knowledge is the best way to extract IBKR data for performance summaries with other accounts.

Most other tools provide inaccurate data, snaptrade wont provide IBKR transaction data for historical data.

I use it by doing Flex query for interactive brokers and Snaptrade for Robinhood and anything else.

Feel free to give it a try and test it out: https://t.co/xaSHBNwxo3

Trying to get an AI news feed for holdings working properly then will be released

This is one of the best opportunities I’ve seen in quite some time...

I recently took this position after the US announcement of worldwide tariffs sent the Tokyo Stock Exchange into a frenzy. The nice thing about this company is the majority of sales are in Japan, China, Taiwan and other Asian companies with limited exports to US. Therefore, initial effects from tariffs should be limited besides total economic slowdown. On top of that, Semiconductors are excluded from tariffs, protecting the market even further.

The name of the company is RS Technologies $3445.

I bought this stock near the bottom of the dip in early April 2025 achieving an average price of 2209 per share, a great bargain. I still believe that there is upside of over 100% from here.

Quick Summary, what do they do?

RS Technologies Co., Ltd. is a Japanese semiconductor company that operates 3 main segments: reclaimed wafer manufacturing, prime wafer manufacturing and semiconductor related products.

Their main business is reclaimed wafers which semi manufacturers use to calibrate equipment and perform test runs. This is a recurring revenue product because the actual chips being made change every year or two, sometimes more. It is important to note this is a commodity product, however it is still vital to the semi manufacturing process. Additionally, RS is the largest player with 33% market share and may have the best distribution. More on this later.

The other main business is prime wafer manufacturing in China, under the listed company GRINM Semiconductor Materials Co., Ltd, 688432. They create the silicon wafers themselves which other companies etch then etch to create chips for Power semiconductors, electric vehicles, industrial equipment and much more. This market is forecast to grow at 9.3% per year globally. Again, while this is somewhat of a commodity product, supplier trust creates somewhat of a switching cost for semi manufacturers due to the complexity of the process. Let’s say I’ve been making chips with Supplier A’s wafers for the last 10 years, I wont take the risk of switching to Supplier B’s wafers and risk impure wafers dropping the yield of the factory.

Lastly, the semiconductor related products are made of many smaller divisions that both manufacture and distribute semiconductor related products.

I will break down the analysis into 2 parts: Why it is cheap (Valuation), and why the business is good enough.

Why it’s cheap (Valuation)

To get the obvious part out of the way, the company is very lowly valued compared to sum of the parts of Net Cash, Reclaimed wafer business, Shanghai listed subsidiaries.

Back in the 2024 investor presentation they did a good job of breaking it down visually:

Keep in mind that the market cap in the image is 80B yen and the market cap as of today is 56B yen, thus the value gap is even wider.

Let’s break this down a little further:

The biggest portion of the valuation is the stake in the Chinese Prime wafer manufacturing company GRINM Semiconductor Materials Co., Ltd, 688432 on the Shanghai stock exchange. RS Technologies owns a 45% stake of this business.

As of today the market cap of this business is 1.9 billion USD.

The value of RS’ stake is 863 million USD. Contrast this with RS Technologies market cap of 450 million USD.

Even if GRINM trades at a stretched 62x P/E, RS’s stake is still nearly double its entire market cap. You’re getting the rest of the business—reclaimed wafers, cash, distribution—for free or less than zero.

So what is the reason that investors do not like RS Technologies?

I believe that the 2 main reasons are China exposure and Shareholder return policy.

The company does have exposure to China, but I see this as an advantage as the China demand is responsible for a large part of global growth, even if the US were to reticent semi trade.

They pay a small dividend, but the main vehicle for shareholder returns is M&A. This process is lengthy, and of course, there is no guarantee you will make an above average return on capital from the Acquisition. Initially, I avoided the stock due to uncertainty around the M&A strategy. But after the sharp selloff, the discount became so large that even mediocre execution would still generate attractive returns.

Also, the M&A is Strategic, which I get into here:

Why the Business is good enough

I preface this section by saying you can write several articles this length about the many businesses that RS is involved with, all of which are very technical in nature. I don’t claim to be an expert nor understand every business. The next resource is the IR page has a pdf that explains every business in detail. That being said, you really only need to understand the reclaimed wafer, prime wafer and M&A track record to know all you need to know.

Firstly, the reclaimed wafer is a key part of the manufacturing process. Reclaimed wafers are wafers that have been previously used in manufacturing, then cleaned, polished, and restored for reuse. Reclaimed wafers are used for a variety of purposes, including particle monitors, diffusion/CVD/implant, equipment set-up/qualifications, demonstrations, etch rate sampling, and as furnace fillers.

Point being, I don’t see the technology being disrupted.

Second is prime wafer manufacturing. The silicon wafer is the core building block for any chip. Companies like SMIC and TSMC specialize in turning the wafer input into useable chips at the end of the process. So there is a small risk of disruption in this business but more important is the risk of being the low cost commodity producer.

The Prime wafer manufacturing market is projected to grow at 9.3% CAGR (2025-2034).

Third is the semiconductor related business which is a mosh of smaller business

Lastly, the most important idea about RS technologies is the ability for the direct sales force to cross sell existing customers. The

Shareholder Returns / Reinvestment

To Start, here is what the company says they will return for the next 3 years

It seems like a whopping 70 billion Yen will be invested into existing businesses over the next 3 years. Keep in mind the current market cap of 64 billion Yen.

If you believe in the future potential of the businesses that much why not buy back the depressed stock price when ROIC is only 13-14%??

Nonetheless, even if ROIC is low for the 70 billion Yen invested, because of the depressed valuation, investors can still make outsized returns.

The next pillar is the M&A. Many in the investment community regard most M&A as value destructive. On the contrary, I will explain why M&A in this instance may create shareholder value.

Since the creation of the reclaimed wafer business in 2010, RS has forged long standing customer relationships due to the nature of their repeat business. Then what they have done is bought other businesses and sold new products to the customer network. This can be a really effective strategy for companies to be worth more as a part of RS than outside of their network.

The idea is that the company is going to acquire other vital parts of the semiconductor / electronics supply chain, and then sell it using their direct sales network.

One example of this is their purchase of a hitachi distributor to sell Ultrasonic imaging systems. We also have an approximate indicator of the success of these investments because they segment report. Here are the latest numbers from this segment:

Of course the quality of each of these lines within the segment will vary, but overall I am confident in the distribution network being a competitive advantage.

Within this segment, there are also some moonshots that have the potential to 2-3x from the acquisition price as they target some huge markets like battery storage and automotive optical sensors.

TLDR

With a net cash, niche products, and a stake worth nearly double its own valuation, RS Technologies represents a deep value opportunity in a misunderstood part of the semiconductor world. If management executes even modestly, the upside could be significant.

It’s kind of crazy that the US markets will glamorize ASML, KLA, AMAT but there are Asian counterparts in equally important parts of the same semi supply chain that trade at fractions of the price or negative EV like RS.

If you find any flaws in my thesis please express your argument in the comments or dm me on X @firsthillcap.

As a reminder nothing in this article constitutes financial advice.

To learn more about the Semiconductor manufacturing process the Asainometry YouTube channel is the best resource. I learned about the ruthless supply chain expectations in this video:

Very nice rerate on RS Technologies, congrats to those who played it.

Still holding a full position, although the rally is likely driven by a general move up in AI adjacent stocks rather than fundamentals

Li Lu on how to invest under $100k:

It's interesting in Korea there's a form of a securities called preferred securities.

These are essentially non-voting common stock that pay a slightly higher dividend — not much more, but they carry no voting rights.

For interesting reasons, these shares sometimes trade at a 70% to 80% discount to their voting common stock equivalents.

And within this group of securities, there are several companies that possess truly enduring franchises. These companies have been growing earnings and revenue at a compounded rate for over three or four decades.

Their businesses are like fortresses with very long purchase cycles — powerful earning machines that still have significant room for expansion. Yet they are trading at prices that represent only a tiny fraction of what they would be worth in a private transaction if someone were to buy the entire company.

In fact, even today, there are situations where the voting common stock and the non-voting shares are virtually identical in economic terms. In some of these companies, the founding family controls the voting shares anyway, so there is virtually no real difference between the voting and non-voting shares.

And yet, the non-voting shares are trading at an 80% discount — I’m not talking about 20%, but eighty percent. They are effectively trading at twenty cents on the dollar, if you believe the common stock reflects the true value.

This kind of opportunity has existed across many different securities. So if you’re young and just starting your career, and if I were starting all over again, I would first study the great examples in history where the market went to extremes on a small segment of securities — creating tremendous margin of safety. Even if things go wrong, you can still come out okay and remain in the game.

Then, study what is available today. At any given time, there are always opportunities like this. It really comes down to fundamental human psychology. And as long as humans remain the same — which I suspect they will, even after billions of years — these opportunities will continue to appear.