The pullback in memory stocks, while healthy, seemed overblown in the context of multiples and a lack of any structural changes in the thesis.

However, it's hard to envision too much of a recovery this week beyond today's action given the impending $SPCX IPO.

We've raised a $500 million Series D to continue solving the next big challenge in space: movement beyond launch.

With over $1 billion in total capital raised, our team and our production are scaling aggressively to accelerate humanity’s future beyond Earth.

Read more: https://t.co/lDhjQyADHU

I’ve been holding this back for fear of calling the top but…

People pointing to the historical cyclical nature of the memory market, and shouting bubble, seem to be completely ignoring the once-in-a-century technological revolution that is AI.

Everything has changed.

"Memory is cyclical, everyone knows that, and the recent run up in memory names is an obvious bubble."

That's the easy, reflexive view. But I think the people who hold it are missing the simple scale of what AI is doing to memory demand.

The first clue that there might be more to the memory story came in January of this year when it came out that NVDA's next gen Rubin platform would require 16 TB of NAND per GPU, or 1152 TB per rack, and that required HBM bandwidth for the system would be 70% higher than what had been previously reported.

That was the first time it became obvious to outside observers that memory would need to scale exponentially to keep up with already-known GPU demand.

One under-appreciated fact is that while GPU compute has largely scaled with Moore's Law (doubling in compute ~every 2 years), memory density and speed hasn't. As GPU compute continues to scale, existing memory manufacturers must produce exponentially more chips.

These chips will also need to be faster than ever, which introduces an incredible technical challenge: how can memory manufacturers find the required speed improvements that have eluded them for decades?

When you combine this added technical complexity with an exponentially expanding demand for the product, memory starts to look less like the "commodity" everyone knows it to be, and much more like a high-margin proprietary chip.

This hasn't even touched on memory's role in inference (compute needed for inference is expanding exponentially as well, and is highly memory-dependent), long context, etc.

Agentic AI requires agents to pull massive amounts of data into their context, which increases the number of tokens per "turn" and also the amount of memory required to run them. True agentic systems will require both dramatically higher context, and also many more "turns" or iterations of each task (as they improve an output over and over until it reaches a target quality level). Longer context = more memory per workload, and more "turns" = more workload per output.

To put a specific number on that, Micron SVP Jeremy Werner said recently on The Circuit that agentic AI is causing context length to grow 30x a year.

Michael Dell recently framed the problem in extremely simple terms: H100 had 80GB of HBM; by 2028, accelerators could carry ~2TB. That is 25x more memory per accelerator. Over the same period, he expects roughly 25x more accelerators deployed.

That's 25 x 25 = 625x more accelerator memory demand by 2028.

Everyone knows memory stocks are cyclical, and they always look cheap right before the bubble bursts. But what if there are structural changes happening in the memory markets that could prove the consensus wrong?

Does anyone remember another traditionally cyclical company that has rerated to a growth story due to the demand from AI? Hint: It's now the most valuable company in the world.

Reminder: this is not a recommendation to buy or sell any securities. It's a framework for thinking about how the AI buildout may be changing the memory market.

Project Hail Mary was amaze amaze amaze. The cinematography, storytelling, staying truthful to the book, and Ryan Gosling were all top notch.

Time dilation and space never ceases to amaze.

https://t.co/QdztCdAacZ

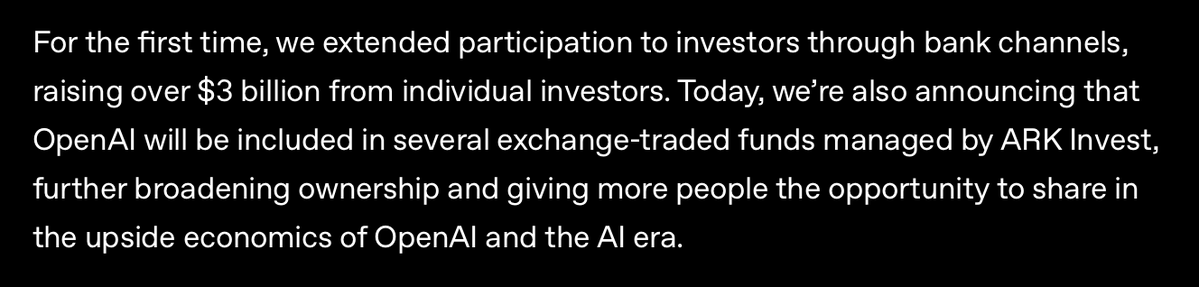

OpenAI just raised $122B at a $852B valuation. Buried in the announcement is something quite fascinating...

1. Participation of individual investors through presumably private banking products HNWI

2. Inclusion of OpenAI in ETFs managed by ARK Invest - guessing it's probably $ARKVX

$ARKVX is about to be the next $VCX

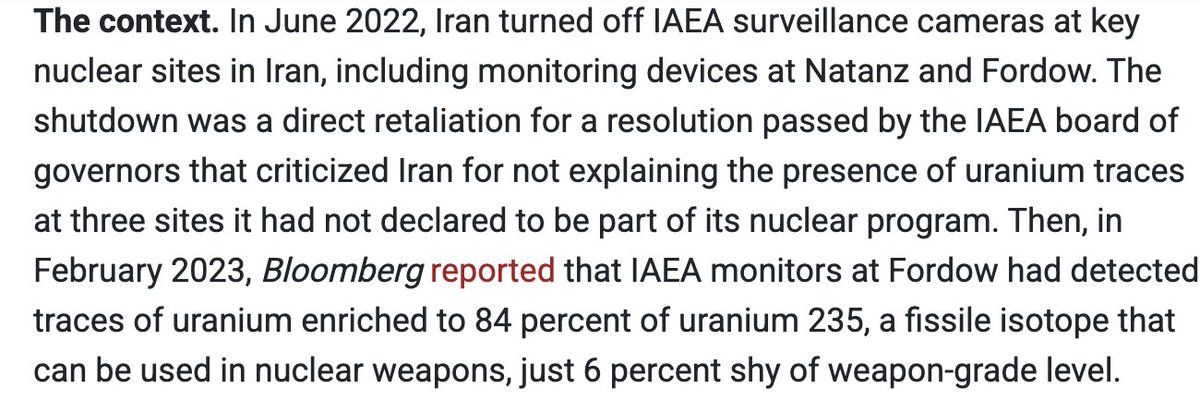

Some very scary reports about Iran that likely caused Israel to strike last year.

Most likely hypothesis: highly enriched uranium.

https://t.co/7e2ncPUpzE

"Highmark (payer) posts $175M net loss for 2025 amid insurance headwinds"

> The insurance division posted a $609 million operating loss in 2025 due to high claims and medical utilization.

> AHN (provider), a wholly owned subsidiary of Highmark Health, posted $90 million in operating income and an increase in EBITDA of $257 million compared to 2024.

Read: If a payvider can't stymie losses on their insurance side due to rampant increase in AI-based upcoding from the provider side, then it is going to be an absolute bloodbath for the insurance businesses that don't own providers.

Consumer premiums will only go in one direction if this continues.

https://t.co/oZu2ZPXRrY

Solutions like this will further break the backs of insurance companies, which whether you like it or not, relied on some level of inefficiency in care delivered vs coded to stay solvent.

Provider systems will bill more, insurers will push back/deny/delay claims more, and if the providers successfully collect will use the $$ to hire more admin staff and fund more capex projects to increase write-offs.

And in the end, premiums will increase and the cost of care for consumers will continue to climb… The vicious cycle continues.

Solutions like this will further break the backs of insurance companies, which whether you like it or not, relied on some level of inefficiency in care delivered vs coded to stay solvent.

Provider systems will bill more, insurers will push back/deny/delay claims more, and if the providers successfully collect will use the $$ to hire more admin staff and fund more capex projects to increase write-offs.

And in the end, premiums will increase and the cost of care for consumers will continue to climb… The vicious cycle continues.

Today we're introducing Coding Intelligence™, allowing physicians to focus on their patients while OpenEvidence seamlessly automates the coding process for accurate and accelerated reimbursement.

Modern medical billing is broken. There are tens of thousands of billing codes and endless ways to code the same visit. It is virtually impossible to navigate this complexity and get appropriately reimbursed without shifting focus away from patient care. We built Coding Intelligence™ to solve this.

@ThisWeeknAI@Jason Does AI solve the artificial restriction of supply of doctors thus resulting in high medical school costs (debt) and wages (patient costs)?

Spot on.

Policy levers can be a tremendous tailwind for new companies and should be leveraged far more to drive real change instead of shuffling the same 100 pennies around.

However I’m highly skeptical that TEFCA and others will actually reduce admin costs via layoffs/reduced hiring when offset against cost to comply/usage.

@yrechtman Preach. Was just saying the same thing the other day.

My personal vendettas:

- Health insurance tied to employer: not a true free market; ICHRA starts to address this but rip the entire bandaid off

- Medical societies: artificially restrict supply of doctors driving prices up

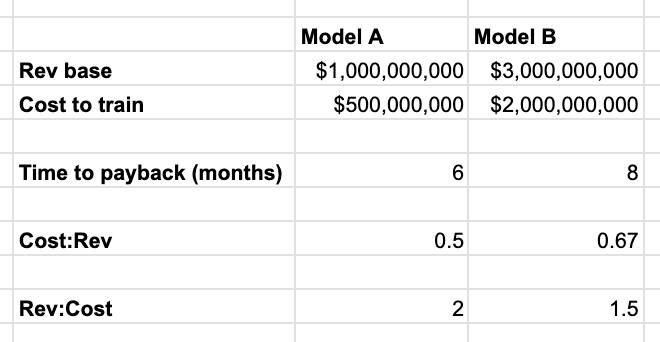

>"Said another way, if it takes you 6 months to pay back Model A’s training cost on a $1B revenue base, and Model B costs 4x more to train but you’re on a $3B revenue base… the payback period actually shrinks. The ratio is getting better, not worse."

Isn't the revenue to cost ratio and payback period getting worse, not better?