Does anyone else have this annoying seed planted in their mind too?

Whenever I see $MRVL drop, I get reminded of Jensen’s comment “The next $1T company”.

$GLW Corning: The AI Optical Infrastructure Springboard Strategy. Investment Thesis. New: 6/29/26.

Corning has repositioned a traditional materials manufacturer into a critical supplier at the physical layer of AI infrastructure — a transition that leverages decades of fiber optics and photonics expertise into a market where that expertise is now mission-critical rather than commoditized. High-density fiber and advanced photonics are the connectivity backbone that AI data centers require as networking bottlenecks become increasingly binding constraints on cluster performance, and Corning's manufacturing scale and materials science depth position it as one of the few suppliers capable of meeting that demand at the volumes hyperscalers require.

The NVIDIA and Meta partnerships are significant validation points. Both represent demanding customers whose technical requirements and qualification standards are rigorous, and their direct engagement with Corning signals that the company's optical infrastructure capabilities are viewed as strategically necessary rather than substitutable. That kind of direct hyperscaler relationship is difficult for competitors to displace once established, given the integration depth required in data center network architecture planning.

The Springboard strategy is the financial framework converting the AI infrastructure opportunity into demonstrated margin improvement. Operating margin expansion that has already materialized provides credibility to the more aggressive 2030 revenue growth targets — this is not a purely forward-looking narrative but one with a track record of execution behind it. That said, the distance between current results and the 2030 targets is substantial, and the growth trajectory assumes continued AI infrastructure capital spending at a pace that has historically been difficult to sustain without periodic digestion phases.

Capital intensity is the structural constraint on returns during the buildout phase. Scaling fiber and photonics manufacturing capacity to meet AI-driven demand requires sustained capital deployment, and the return on that investment depends on demand durability matching the capacity being built. Customer concentration compounds that risk — significant revenue exposure to a small number of hyperscaler relationships means that any shift in AI infrastructure capital spending plans at a major customer would disproportionately affect Corning's growth trajectory relative to a more diversified customer base.

The Solar business is a complicating factor that sits somewhat apart from the core AI optical infrastructure narrative. Scaling that segment successfully requires different operational capabilities and serves a different demand driver, and management attention split across a capital-intensive solar scale-up alongside the AI infrastructure buildout introduces execution complexity that pure-play AI infrastructure companies don't carry.

The valuation reflects multiple years of anticipated growth, which means the premium is justified only if execution stays on pace with the Springboard targets and AI infrastructure capital spending remains robust through the multi-year buildout period the thesis depends on. Corning's market position is genuinely dominant in its core optical infrastructure niche — the question is whether that dominance, expressed through a still-developing financial trajectory, supports a price that has already captured much of the anticipated upside.

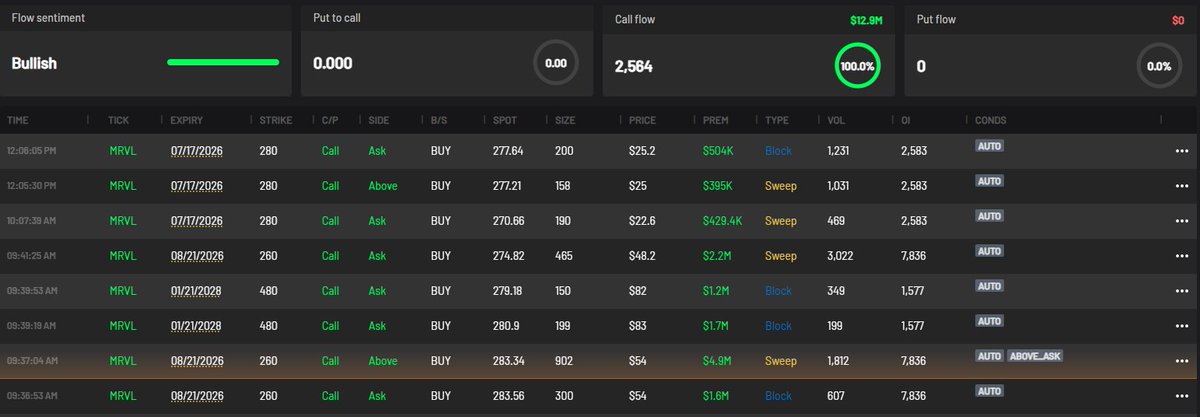

$MRVL call buyers are all over the tape 👀🔥

Flow sentiment: Bullish 🟢

Call flow: $12.9M

Put flow: $0

Put/Call: 0.00

100% of premium is hitting calls today.

Biggest focus is the 8/21 $260C, with multiple aggressive buys including a $4.9M sweep above ask and another $1.6M block 📈

Also seeing longer-dated positioning in the 1/21/28 $480C with $2.9M+ traded.

No put flow showing — buyers are clearly leaning upside on $MRVL 🚀

Server-grade DDR5 memory costs $27 to $37 per GB today, and prices have risen 300 to 400% since mid-2025. For AI workloads that are consuming memory faster than fabs can produce it, that is a significant infrastructure cost challenge.

Marvell Structera CXL devices address this through a purpose-built hardware block that compresses data at full memory bandwidth as it is written to DRAM and decompresses it on read, completely transparent to the host CPU. The result is that the host sees more memory than physically exists on the device, at ratios that can reach 2:1 or higher on real-world data types.

Director of Product Marketing Arifur Rahman details how the technology works and what it means for the economics of CXL memory pools: https://t.co/KlPv37vcY9

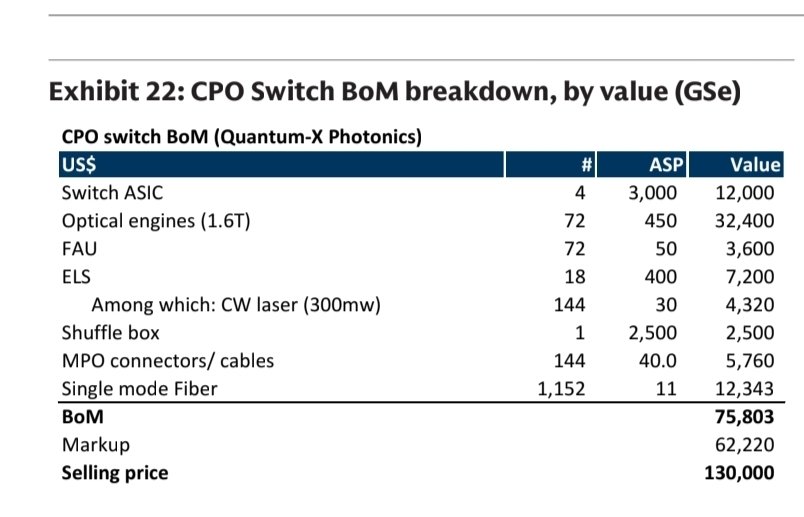

The photonics related stock sell off looks ridiculous.

NPO does require:

- Laser source

- FAU

- PIC/EIC all just like CPO!!!!

The main thing that changes from CPO is where PIC/EIC assembly is located - whether on ASIC substrate (CPO) or off-ASIC substrate (NPO).

And did you know NPO needs more DSP logic (which could be absorbed in ASIC) than CPO, as it needs more correction of disturbance caused by long connection? @austinsemis

So in going from CPO to NPO, you basically you are trading packaging complexity of CPO for packaging simplicity of NPO at higher energy expenditure. Laser, FAU, PIC/EIC all still needed.

What am I missing?

@iamfabian@jaygoldberg@vikramskr@zephyr_z9