Correction:

the alsic for rubin thesis is wrong for $cpsh. semianalysis already did the work

rubin and rubin ultra at 1800w to 2300w are not getting alsic lids. the thermal stack disclosed by nvidia at ces 2026 and detailed by semianalysis is:

copper base lid with electroplated gold (to resist indium tim2 corrosion)

stiffener added for warpage control

microchannel lid (mcl) etched into the copper itself

liquid metal indium tim2

gold plated copper cold plate

no aluminum silicon carbide anywhere in the spec

the two taiwan winners are:

jentech precision (tpe: 3653) sole supplier of tsmc cowos lids and stiffeners. 100% share in ai chip lids. mcl asp is 7 to 10x the blackwell lid. if all nvda chips migrate, jentech revenue could grow 50%+

asia vital components (avc, tpe: 3017) partnered with nvidia on the microchannel cold plate for rubin ultra

amd mi450x at 2500w follows the same roadmap. nvidia, amd, aws, google are all converging on copper mcl, not alsic

alsic is a real material with real defense and space and power electronics uses, but it is not the rubin packaging material. the entire ai bull case people are putting on $cpsh is built on a thesis the original substack author rated low probability and that semianalysis never even mentioned

if you want the rubin thermal trade, the names are 3653 tt and 3017 tt, not $cpsh

Serenity was early, again.

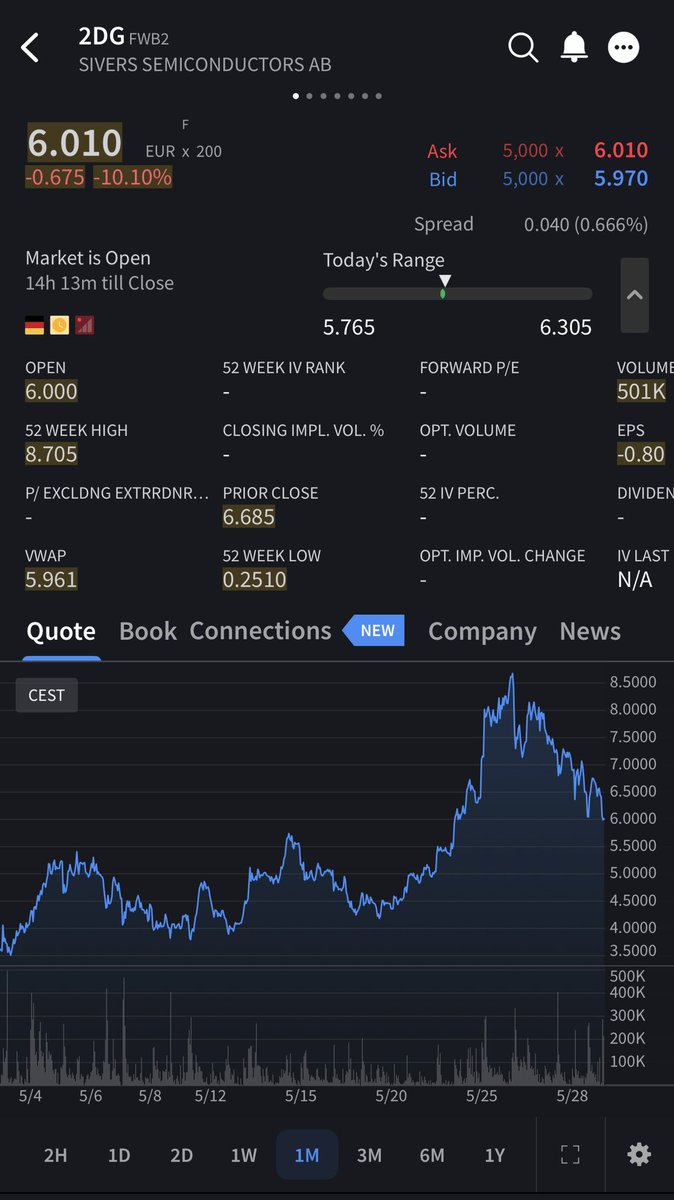

$cpsh ran from $7 to $10.82 intraday then $11.72 aftermarket. volume 17.5m vs 900k avg (19x normal). new 52w high

confirmed in $nasa tema space etf as of may 22: the ETF owns 1.82m shares, 0.76% of NAV, about 10% of cpsh float held by the etf

balance sheet: $12.5m liquid, zero debt, 18m shares outstanding (10% held by $nasa ETF)

concentration risk: top 3 customers = 64% of fy25 rev

segment potential:

- power electronics (the actual core, 60-70% of rev): hvdc, ev and hev inverters, wind, sic and gan modules. the $15.5m semi order lives here. q1 10q flagged this customer taking less than 50% of contracted qty.

- space (real but small): flight heritage on gps iii sats, mars 2020 rover, iss, methanesat. est $3-8 million today. golden dome and sda is the upside lever.

- defense (mixed real plus r&d): navy destroyer hybridtech armor with congress funding secured, ceo says modest scale. tungsten 40mm warhead phase ii sttr ($1.15m, 2 year r&d). uh 60 armor is sbir research. about 5% of rev from sbir per cfo

- ai and gpu thermal: current ai supply chain goat @aleabitoreddit posted a thesis on this ticker:

1) alsic could be spec’d as microchannel lid for 2300w plus chips. $cpsh would be one of few western suppliers. denka, sumitomo, byd are the incumbent risk.

2) laid out the materials science case for AlSiC in rubin/mi450x packaging at 1800 to 3000W TDPs.

3) mentioned as rubin's to scale up to 2300-2500W in 2027-2028, that same material may be used ai due to heat warpage.

my research on official filings and $cpsh management transcripts show zero company mention of nvidia, rubin, or gpu in any earnings call. but would trust serenity over myself sincr im not even close to an ai scientist

also watch:

- DOE nuclear (radiation shielding, snf transport)

- electric rail and subway mmc baseplates

- 5g and satcom hermetic packaging

- new commercial tungsten injection molding line (first order shipped apr 2026)

Narrative is lasers will be a chokepoint within optics which is anticipated as a major chokepoint. They will get more pricing power if that holds true. But honestly this is over my head I am right there with you, I guess the market sees the potential clearer than me. I sold in the $700s

$SIVE Q1 2026 earnings release observations:

22% revenue miss looks ugly on the surface, yet nothing here breaks the actual bull case. The thesis for 2027 inflection just got stronger imo.

1) Pipeline exploded +77% to $799M YTD (most important takeaway)

2) Jabil 1.6T win validates the laser tech for AI datacenters (most important takeaway)

3) Lidar ramp holds for Q4 2026

The setup for a probable 2027 inflection is there. However, shareholders have to survive the liquidity issues before that, they will run out of cash in 3-4 quarters or less.

Q1 results:

- Cash down to 26.6M SEK

- Q1 burn 49.2M (3x last year)

- 125M raise closed April, but that’s <1yr runway

Management says FX headwinds and US defense budget plus shutdown delays pushing revenue from Q1/Q2 into H2 2026:

- Revenue 61.9M SEK, −22% YoY (miss vs 74M consensus).

- Defense budget delays + FX pushed sales into H2.

Both segments shrank:

- Wireless −16%

- Photonics −32%

@arv9293 Felt kind of that way, very binary story. 2027 or cashflow or bust story. They sell lasers to aaoi lite cohr so I guess if optics tam grows they will grow.

$ASTI - Ascent Solar

A toaster sized satellite making 150W. That’s power normally seen on craft 10x bigger. $asti’s flexible solar “blankets” make it possible. They’re on NOVI’s Pathfinder, targeted to launch spring 2026 on Falcon 9. If the constellation scales, $asti gets to power all of it (that’s the lotto ticket).

Why asti’s flexible solar panel is different:

The core idea is a solar panel you can roll up like a yoga mat. It’s a game changer because:

1) Weight. This is the big one. Far lighter per watt than rigid silicon, which is everything in SPACE and on DRONES where every gram costs money to lift.

2) Flexibility. It rolls tightly for launch, so it takes up little stowed volume, then unrolls in orbit.

3) Durability. No glass to shatter. If struck by debris in space, it fragments less, which matters for orbital safety.

- company is about 20 people in Colorado

- debt free, $16M cash, basically considered pre revenue and burning cash.

- runway about 2 years based on $2M/qtr burn

CIGS = how much of the sunlight hitting a solar cell gets converted into electricity.

- asti CIGS (flexible panels) = 15.7%

- Mainstream CIGS (rigid silicon) = 20-22%

Asti’s 15.7% cigs must be respected. In space the metric that matters is power per kilogram, not power per square foot. Same with drones.

Upcoming catalysts:

- NOVI Pathfinder launch on Falcon 9, spring 2026.

- NOVI constellation scale up. The real prize.

- potential Defiant and NASA deals.

Is photonics done? Rotation to SaaS and memory starting to happen.

SaaS companies $snow $dell and $mdb reported amazing earnings.

Memory trading at low forward earnings multiples.

Could this be end of the run (in the near term) for $aaoi $lite $cohr?

@grok@grok with the stock price at $170-180 this time versus $80-100 during the last $500M atm should it in theory be closer to half the days it took for the prior atm?

Is that $600M atm almost done yet for $aaoi?

Last time it took them 35 calendar days (25 trading days) to raise $500 million at the market when the stock price was around $90-100 dollars

The share price was somewhere between $170-190 during this the current ATM, my estimate is it should be done either this week or first week of June at the latest.

I think the best way to tell is to see if this stock can hit $190. If it does hit $190 again, then I think that the atm is done.

@aleabitoreddit Bought another $1M at $171.

That ATM should end this week or first week of June based on how quick they went through the last $500M. It was finished in 35 calendar days (25 trading days) when stock was $80-100 per share