$BB BlackBerry

The Path to $11.50

Our aggressive target is modeled on a sum-of-the-parts (SOTP) re-rating as the market realizes the IoT and Cybersecurity segments operate more efficiently as standalone units.

If the fast-growing IoT/Physical AI business is assigned a conservative 10x Enterprise Value-to-Revenue (EV/Rev)multiple—in line with pure-play embedded software and IoT infrastructure peers—the market cap expands significantly.

Combining this with a stabilized 3.5x EV/Rev multiple on the steady, recurring federal government cybersecurity stream yields an aggregate valuation of $11.50 per share, implying roughly 70% upside from current levels.

Key Catalyst: Watch the upcoming Q1 earnings release in late June. Continued expansion of the QNX royalty pipeline and net-positive cash flow generation will force a structu

$NBIS JUST IN: Famed Billionaire Ron Baron’s Fund Baron Capital Group initiated a position in Nebius in Q1

From Baron Capital:

“Nebius is a Big Idea with a remarkable origin story – the company was born from Yandex, popularly known as the “Google of Russia,” which founder Arkady Volozh built into a $30 billion business over 25 years with leading positions in online search, e-commerce, ride-hailing, music streaming, maps, and cloud services. After Russia’s invasion of Ukraine, Volozh divested all Russian assets in the largest corporate exit from Russia in history ($5.4 billion), reconstituting the company as Amsterdam based, Nebius. The company boasts a world-class 1,300-strong team of engineers with decades of experience building large-scale computing systems and a vision to build a leading AI cloud business from first principles – a purpose-built vertically-integrated hardware and software stack optimized for AI workloads.

Nebius’ long-term vision requires significant resources to build the physical infrastructure and acquire customers. In the interim, Nebius is strategically and very selectively signing bare-metal GPU deals (renting the data center with the GPUs installed but no software on top of the GPUs) with Microsoft (up to $19 billion) and Meta (up to $27 billion). While there is a range of outcomes on the long-term value of GPUs in a bare-metal model (with the main concern revolving around the rapid depreciation of old GPUs as new more efficient ones are introduced), the useful life of AI accelerators appears to be longer than previously anticipated, as the economic output of GPUs (as measured by token throughput) has been increasing over time as models have improved, meaning project returns get better with age. Dylan Patel of SemiAnalysis explained the dynamic on the Dwarkesh Podcast (March 2026)14: GPT-5.4 from OpenAI generates more tokens on H100s than GPT-4 did, despite being a far more capable model, because newer architectures (such as sparse mixture-of-experts) are more computationally efficient per token. The implication is that an H100 is worth more today than when it was purchased three years ago. For Nebius, this means the residual value of its GPU fleet after long-term contracts expire could be substantially higher than depreciation schedules assume. The rapid growth in AI-demand has also driven H100 one-year rental prices higher by approximately 40% from $1.70 per hour in October 2025 to $2.35 per hour by March 2026 (SemiAnalysis, March 2026),15 even as NVIDIA’s newer Blackwell GPUs entered the market. In our view, as long as incremental AI token demand exceeds the token supply enabled by the new chips produced in a given year, older GPUs retain – and can even gain – value (as long as token throughput increases over time as models improve – despite an increase in intelligence). More importantly, these deals function as a quasi-financing mechanism for the AI cloud buildout. Meta's deal in-particular provides access to investment grade borrowing costs with no equity dilution, while acting as a backstop customer if enterprise demand for the AI cloud doesn't materialize on schedule.”

At today's price, we are essentially buying a contracted bare metal business and a portfolio of valuable stakes at a fair price, and getting what could become a very big idea, as one of the world's next great AI cloud platforms with a world-class Founder/CEO and a team of engineers who have succeeded before at an attractive entry point.

We have conviction in Nebius' ability to build a large AI cloud business. They are leading the neocloud space in building a full suite of software offerings on their platform, much in line with what the big three hyperscalers have built for cloud workloads, i.e., multi-tenant compute, unified storage, inference-as-a-service, and security certifications, the kind of platform depth that took incumbents years to assemble.”

https://t.co/Hk6tSP47bM

$TE shows how heat, vacuum pressure and precision engineering turn glass, EVA and solar cells into a fully sealed solar module.

This lamination step protects the cells, improves durability and supports the bigger push to become a leader in American solar manufacturing.

S&P 500 earnings are now expected to increase by 24% this year. We've never seen earnings growth this high outside of post-recessionary rebounds. An unprecedented boom fueled by massive EPS gains in big tech.

Video: https://t.co/BE95GpQv5f

,” Moody’s Ratings said in a May 13 report. In terms of cross-border payments, stablecoins can settle for 0.1% to 0.5% of a transaction value, compared to an average remittance cost above 6%, Moody’s said.

$CRCL $V $MA $AXP

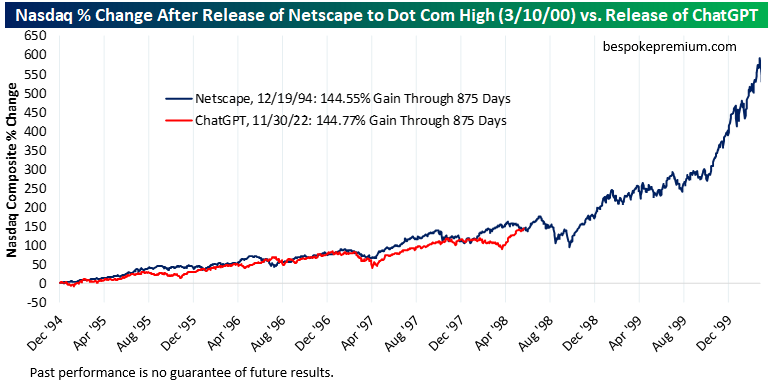

UPDATE:

Nasdaq at 875 trading days after the release of Netscape on 12/19/94: +144.55%.

Nasdaq at 875 trading days after the release of ChatGPT on 11/30/22: +144.77%.

Past performance is no guarantee of future results!

Analysts where a wee off on their target prices for $DELL heading into the quarterly results

Just prior to the results, 18 of the 27 analysts covering DELL rate the stock ‘Buy’ or higher, seven rate it ‘Hold,’ and two rate it ‘Sell,’

However, their average price target of $218.09 implied a 31% downside from the stock’s last close

Financial

Switching to Enterprise Value (EV)—adding debt and subtracting cash/Bitcoin—reveals a much wider valuation gap.

Hut 8's $HUT liquid Bitcoin vault acts as a massive cash offset, whereas IREN has taken on significant debt to fund its rapid near-term buildout.

The EV Per Gigawatt Comparison

Hut 8 (HUT)

Market Cap: ~$13.07 B

The EV Formula: Market Cap ($13.07B) + Debt ($405M) – Cash ($160M) – Bitcoin Treasury ($1.12B)

Enterprise Value (EV): ~$12.20 Billion

EV / GW (8.38 GW Pipeline): $1.45 Billion per GW

$IREN

Market Cap: ~$24.24 B

The EV Formula: Market Cap ($24.24B) + Debt ($6.84B) – Cash ($550M)

Enterprise Value (EV): ~$30.53 Billion

EV / GW (5.00 GW Pipeline): $6.10 Billion per GW

The Takeaway

On a pure asset basis, IREN is more than 4 times as expensive as Hut 8 per gigawatt ($6.10B vs. $1.45B).

IREN commands a near-term premium because its data centers are online and cash-flowing right now. However, looking at the entire balance sheet, Hut 8 gives you significantly more raw power pipeline per dollar spent, with far less debt leverage attached to the equity

Good luck out there.

The Strategic Bet: $KEEL is doing something incredibly unique: they are skipping the current chip generation entirely. They have designed 99% of their 2026/2027 data center shells around the intense, liquid-cooled power specifications of NVIDIA’s $NVDA next-generation Vera Rubin architecture (slated for late 2026/2027). By building specifically for the Rubin footprint today, they avoid the multi-million dollar retrofitting costs that current "Blackwell-era" data centers will face

$WULF $IREN $CORZ $HUT

This is where the math gets fascinating. Look at what you are paying for every gigawatt of potential power waiting in the wings:

$IREN has a 5 GW pipeline and trades at a $24.2 billion market cap.

$Hut 8 has a 8.4 GW pipeline—nearly double the physical pipeline capacity of IREN—yet trades at a $13.0 billion market cap

Mobile phone subscriptions in sub-Saharan Africa went from near zero to 85 per 100 people in two decades.

Landline phones never reached more than 2 percent of the region's population.

By adopting cellular technology, poor countries were able to leapfrog an important bottleneck in their economic development.

Back in January, on our Predictions show, my Most Contrarian Take for 2026 was that AI would create more white-collar jobs, rather than destroying them. This week Goldman Sachs’ CEO, Sam and even Dario seemed to agree. The consensus is shifting.

Ground zero for the SpaceX wealth story is in SoCal.

~4,000 SpaceX employees will become overnight millionaires in LA

They live in Westchester, Playa Vista, Playa del Rey, El Segundo, and the surrounding South Bay near SpaceX’s El Segundo campus and Hawthorne facilities.

The S&P 500 is up 26% over the last 12 months and forward-earnings estimates are up 28% in the same period.

No matter how loud the bubble crowd gets, the data confirms that the bull market is built on fundamentals.