I have interviewed 1,000 CEOs of the largest companies over the last 10 years.

Adam Foroughi is top 5 I have ever met. Easily.

AppLovin Market Cap: $160BN

Revenue: $5.48BN

EBITDA per Head: $10M

There is no company on the planet with numbers like AppLovin.

Episode coming 👇

Lead Edge has built one of the most unique LP bases in venture, with over 800 founders and executives who are actively engaged across the entire investment lifecycle. They represent 95% of the firm's total capital.

"All of these people invest in funds and never get asked for help.

The reason we did it is because the returns in tech flow to the top 10% of funds.

When I was starting Lead Edge, I asked "why is anybody going to take my money?"

Had I been the global head of HR at P&G and my partner had been the global head of HR at Microsoft, when I called Workday 80 times at Bessemer, Dave Duffield would've engaged with me because he would've known that I could've introduced him to those companies.

In a world that's super crowded and undifferentiated, and I think it's exponentially the case more today even than what it was 15 years ago, it differentiates us and we do what we say we're going to do."

2026 has been a generational year for us at Menlo already.

— Anthropic is the fastest growing company of all time adding $4.5B run rate in 42 days after the $380B round. We put ~$1B into it starting from the Series C

— Suno reaches 100M users and $300M ARR

— Lovable is the 5th most adopted and 2nd fastest growing AI vendor, going 0 to $200M in a yr

— OpenRouter grew 2.5x in 1.5 months. On track to 1 quadrillion token annual run rate.

— Higgsfield hits $200M run rate with creative tools and a $1B+ valuation.

— Wispr Flow continues to grow 40% MoM with a 70% 1 year retention and wins some massive enterprise contracts

— Clerk becomes #4 fastest growing vendor in the league of Google, Atlassian and Replit

— Inception launches the first and best reasoning diffusion model that is the fastest for its intelligence at 1000tokens/s

— Goodfire, Anthropic's first direct investment, hits $1B+ val and discovers novel biomarkers for Alzheimer's

Most VCs don't believe in this model of being picky, low volume investors. We do very few investments (up to 2/partner/yr) and we go early. 5 of these were partnerships since the Seed. It's been working for us so far (even though we've missed a lot too!)

It's an privilege to work with founders who run through walls and take on so much risk to bring new things into the world. And we're very lucky to play a small part in that! Still a lot of work to do.

@bryan_johnson Owner of farm to table Sicilian EVOO shop here (remedy to EVOO slop): https://t.co/QdNzl0VRBP

Owner of bean to bar chocolate manufacturer sourcing from elite cocoa farms: https://t.co/5Lmdrk3MU2

If you had to read one thing about "SaaS is dead": software is not dead, it’s just recalibrating the DCF and therefore the NPV. Stable retention rate will be the true litmus test.

AGI is now on the horizon and it will deeply transform many things, including the economy.

I'm currently looking to hire a Senior Economist, reporting directly to me, to lead a small team investigating post-AGI economics.

Job spec and application here: https://t.co/VAfwrMc8Tp

Man the sentiment on software as an investment here is pretty bombed out. Some various thoughts from having spent a couple decades working in software:

- This was the easiest market for a long time. Greenfield opportunity everywhere

- A few sub-problems flow from this. A) That didn’t exactly nurture what I would describe as “operational rigor.” B) I also wouldn’t describe many of these executive teams as killers C) People are used to operating in an inbound environment with weak competition. Very much not the case today

- Similarly, gross margins hid a bunch of lazy, bad habits

- And investors have never given a shit about real profit, so that is baked into how these companies operate.

- You would think 2022 would have washed a lot of these bad habits away. For some companies, like I would say Shopify is a great example, it absolutely did. For other companies it did for a little, but muscle memory is strong, and times got good again. Some didn’t even really try.

So you are going from an environment with a ton of tailwinds, minimal competition, low interest rates, investors who didn’t care about profit, and high gross margins to…

Incredibly intense competition, needing to sacrifice margins to compete in AI, knife fights everywhere as tailwinds vanish and operating surfaces converge, higher rate environment, investor concerns on terminal value due to AI disruption risk, and a bunch of other real, structural issues that would make this post way too long to read

And almost all these companies aren’t cheap even after this de-rating. And they’re not growing that fast anymore either. And AI native app layer companies are stealing their incremental customer LTV. And the management aren’t really killers because they haven’t had to be.

So do I think a lot of the bear cases are extreme? Yes. But is there a lot, a lot of truth here? Also yes.

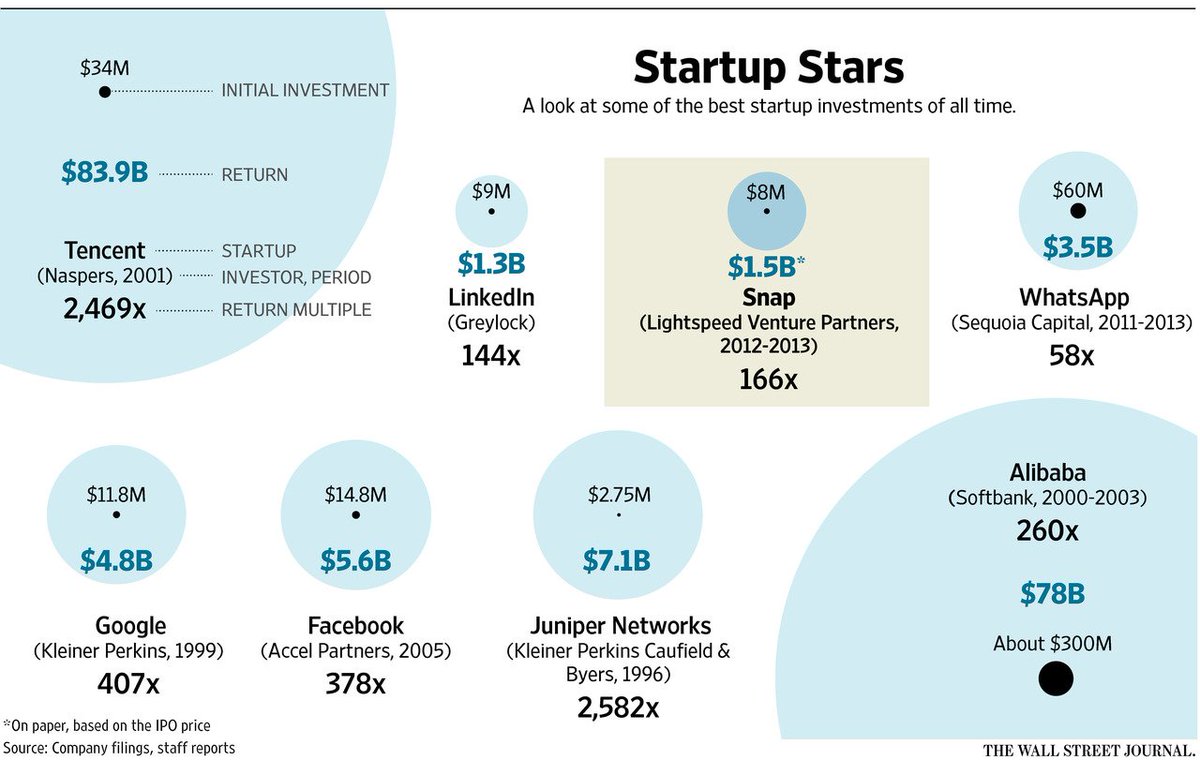

Juniper returned $7b+ to Kleiner's ~$500m fund ... I think it was 2500X but often ignored. Only player doing TCP/IP for the public internet in 1996 when every telco customer wanted ATM. If Juniper had not started the internet likely wasn't going to be TCP/IP. The CTO of @Cisco told me they would never do a router above OC12! https://t.co/IaysW5SsQF

"We have to make sure we're taking enough risk... and that usually comes in the form of evaluate the entrepreneur and the company on the magnitude of their strength [...] I think it's always a mistake to rule out somebody who's truly world class on a weakness."

a16z just announced their newest fund - $15 billion!

I had @bhorowitz on Uncapped to discuss how they run the firm, how he thinks about venture talent, a16z's overall investment approach, deploying capital at scale, media, and more.

He's easily one of the most impressive people I've gotten to have on the podcast. Hope you enjoy.