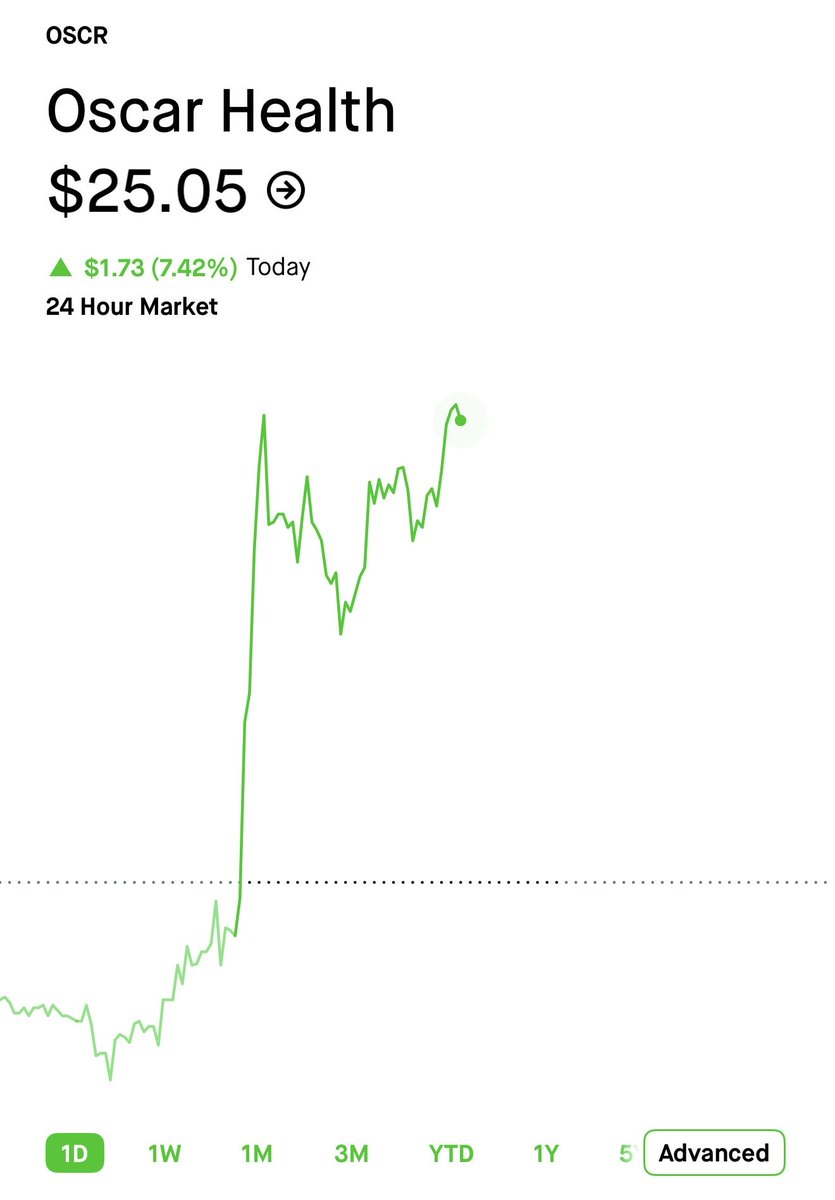

$OSCR

Currently trading at 0.458x P/S of 2026 guidance

250-450 million guide on profitability

PLUS new 130 million positive PPD

380-580 million earnings from operations

PLUS morbidity tracking better than expected

Lets assume just over the higher end, at 650 million

650/19000=3.42% Op Margins…

If 5% margins imply 1x P/S or higher…

Then 3.42% margins imply 0.68x P/S or higher… MINIMUM

That implies a 48.57% price increase to $41.57… MINIMUM

This doesn’t account for a premium given from Lucie, +Oscar, ICHRAx, or the potentially for even higher operating margins in 2026…

This also doesn’t account for 5% margins to likely happen in 2027…

This doesn’t account for competitors leaving the marketplace, which Oscar has overlap with and picks up those members…

This doesn’t account for the fact that ICHRA is becoming increasingly adopted…

This doesn’t account for the fact that we will likely trade higher than recently across the board due to increasingly favorability on insurers…

This also doesn’t account for the fact that $OSCR is one of, if not the, fastest growing health insurance company in the US.

I am Long $OSCR , at $10-13 this was the “mother of all buys”, and at $28, it’s a good DCA, but not “all-in”…

I do what I say. I have daily purchases currently, and will add heavier on dips.

Utilization across healthcare is rolling over - you want to own health insurance / value-based care stocks - particularly with high Medicare Advantage exposure.

$OSCR

WOW.

56% of brokers are now actively recommending or implementing ICHRA

94% of employers have explored alternative cost-containment strategies

Brokers reported an average estimated savings of 15.5%

89% of employees said their ICHRA coverage was better than their previous group plan

Something that seems to have not been spotted by FinX yet in the $OSCR bull case, 2 days ago Dr Oz at the CMS announced fees for carriers in the ACA market were reducing from 2.5% to 1.9% for Federal Marketplaces (FFE) and from 2.0% to 1.5% for State marketplaces (SBEs) for 2027?

Why does this matter you might say, it's tiny!

Here is why it does:

1) This is effectively a reversal back to 2025 pricing, CMS put the fees up for 2026 because they expected 30% reduction in market place size and needed to maintain income. So evidently, this bear case is now gone i.e. ACA shrinkage is minimal and we're hearing it indirectly from the horse's mouth

2) The fee is based on the gross premiums, that's before risk adjustment so disproportionally benefits Oscar who have a high risk adjustment of 20%. As an example a person paying $8.0k a year for coverage would appear on the revenue line for Oscar as $6.4k then incur a FFE CMS market place fee of $200 which is 3.125% and makes up that amount in the SG&A costs. This effect is now $152 so 2.375% falling into SG&A, this a 75 bps improvement on SG&A from the stroke of a pen or roughly one $ in twenty lower SG&A costs

3) "That's still immaterial" some will say, however a gold standard for ACA insurers is 5% margins, that means 15% more profit going from 5% margins to 5.75% margins and even more at the lower end when profits are only 2% or so of revenue

4) Oscar predominantly operate in the FFE markets, the SBEs are rates are down as well albeit marginally less, it will effectively have the same impact on the sub 10% of members Oscar hold in SBEs

Mark B said this in the latest earnings call

"taxes and fees are pretty much fixed for us based on the level of membership. It's 9%-10%. We're looking at the variable piece that we can manage versus that fixed piece, which we literally is sort of a tax for being in the game."

so that 9% to 10% range, just dropped to 8% to 9%

announcement in the link for the detail orientated folks

https://t.co/hCiye6w9uf

For the second year, Oscar is proud to sponsor SureCo’s 2026 The State of ICHRA report.

SureCo partnered with a third party to survey 1,500 finance leaders, employees, and benefits consultants at companies with 150-2,500 employees and pulled the clearest read we’ve seen on how fast the market is changing.

And the headline is simple: when budgets are predictable and people can choose coverage that fits, everyone wins. That’s why more companies are taking a hard look at defined contribution.

🔗 See the full report: https://t.co/1dufEGNnUh

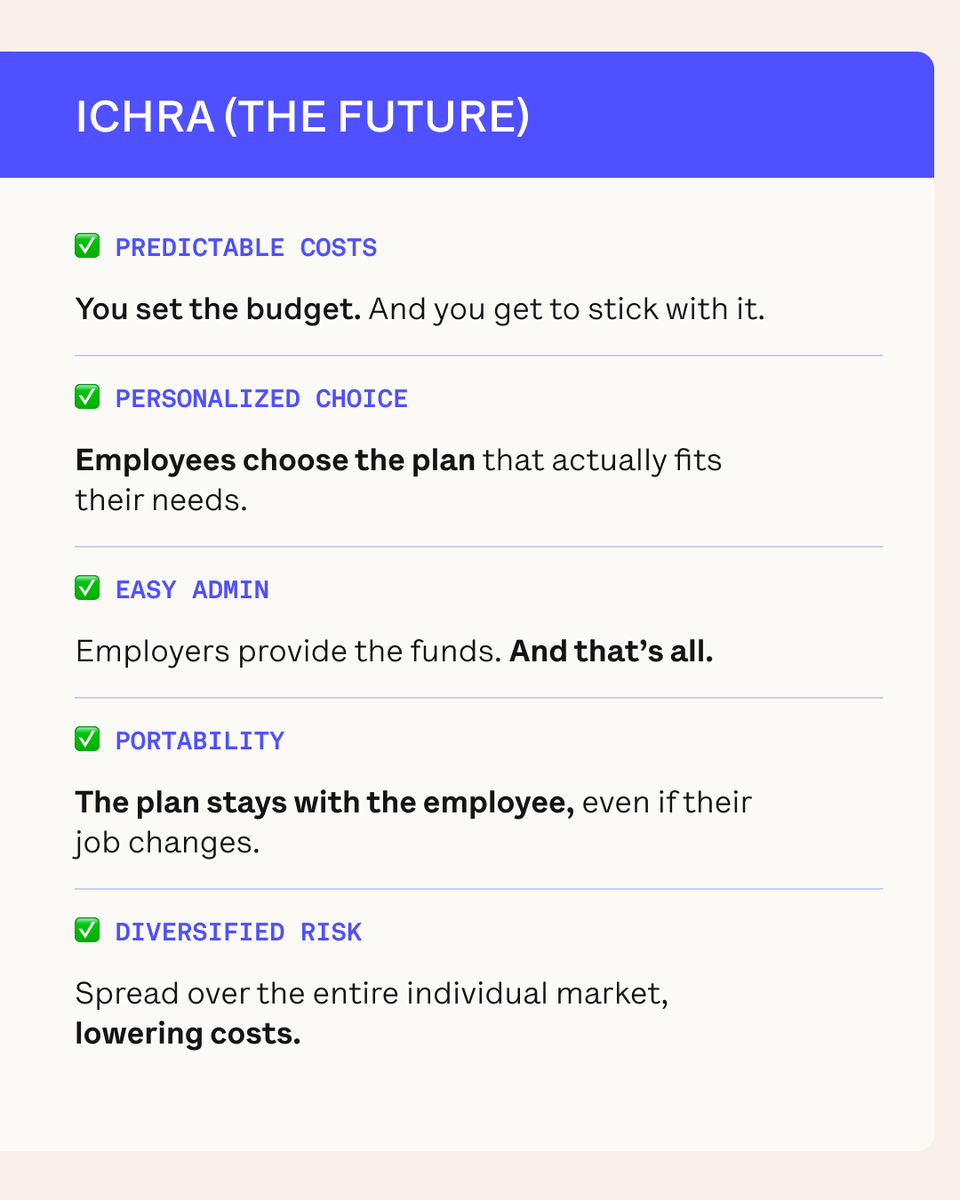

For decades, employer-sponsored group plans have been the default for American workers.

But the default isn’t always the best fit. Rising renewals, limited options, and burdensome admin put employers in the impossible position of choosing “one-size-fits-all” coverage for their employees.

Now, a new model is gaining momentum: ICHRA (Individual Coverage Health Reimbursement Arrangement.) Employers set a predictable monthly budget, and employees use that buying power to shop the individual marketplace for plans that match their doctors and health needs.

The data shift is promising: 60% of employees want to make the shift from group plans to ICHRA, and 94% of employers agree that switching was the right move.