Top Tweets for #GarwareHiTech

#GarwareHitech

DGTR has recommended for imposition of Anti-dumping duty (ADD) on imports of TPU based surface/paint protection film exported from China.

#Garware being a manufacturer of TPU will get benefit from this move wrt cheap Chinese dumping.

Disc - no reco.

#garwarehitech

Garware hitech will be the biggest beneficiary.

Also India -US trade deal around the corner

Leveling the playing field! 🇮🇳 A massive positive impact ahead for Garware Hi-Tech Films as anti-dumping duties get recommended for Chinese #TPU #PPF.

#GarwareHiTech #PaintProtectionFilm #AntiDumping #IndianAutomotive #MakeInIndia

#GarwareHiTech: D2C Strategy Could Be a Structural Margin Game Changer 🚀

Garware Hi-Tech's management made one thing very clear in the earnings call:

Direct-to-Consumer (D2C) is not merely a new sales channel but it is a major margin expansion lever that can transform the business over the coming years.

The biggest advantage of D2C lies in economics. By selling directly to customers instead of through distributors and dealers, Garware captures the entire channel margin.

Management indicated that D2C margins can be 30-40% higher than distributor led sales, depending on negotiations and product categories.

Even when compared with the company's existing B2B/B2C business, D2C channels are expected to generate 25-30% higher margins. This margin uplift is already visible and is not just a future aspiration.

The benefits are especially pronounced in high value categories such as Paint Protection Films (PPF) and architectural/sun control films, which are being sold through Garware Home Solutions and dedicated application studios.

Garware Home Solutions, which focuses on smaller ticket home installations, has been specifically highlighted by management as a high margin business and an important pillar of its D2C strategy.

Despite being in the early stages, D2C is already gaining meaningful traction. Currently, 10-15% of total company revenues come from D2C channels, including domestic and global application studios.

The domestic PPF business is even more advanced with around 40% of Indian PPF revenues already generated through D2C channels, demonstrating customer acceptance and strong execution.

Management plans an aggressive scale up of this model. Garware Home Solutions studios are expected to increase from just 6 today to nearly 50 by the end of FY27. At the same time, application studios in the US and Middle East are expected to contribute meaningfully to growth.

This transition is strategically important because D2C not only improves margins but also strengthens brand power, customer relationships and pricing ability.

The company is also investing heavily in digital marketing, generating over 8 crore Meta impressions and witnessing a significant rise in website traffic. Such investments help Garware build a premium consumer brand rather than remaining only an industrial film manufacturer.

Another important driver is the ongoing shift toward high value products such as architectural films, PDLC switchable films, TPU-based products and graphic solutions- all categories where direct selling can significantly improve realizations.

Operational efficiencies provide another layer of benefit. Digital ordering, online payments and direct customer engagement reduce transaction costs and improve operating leverage.

The upcoming TPU backward integration plant, expected to commence in October 2026, could become another major catalyst. Lower raw material costs combined with D2C distribution can create a powerful double engine for margin expansion, especially in the fast growing PPF segment.

Management acknowledged that marketing expenses and studio expansion costs may rise in the near term. However, these investments are already budgeted and the company believes D2C will still deliver a net margin advantage of 25-40%.

This D2C push aligns directly with management's FY27 guidance of 2500 crore revenue with a 25% ± 2% EBITDA margin band. Importantly, management explicitly linked future margin expansion to two key drivers: TPU backward integration and D2C scaling.

Architectural films, growing at 25-30% annually, along with D2C initiatives, have been identified as some of the company's fastest-growing and highest-margin opportunities.

At a strategic level, Garware appears to be evolving from a B2B heavy manufacturer into a premium consumer facing brand, much like it successfully created the PPF market in India.

#GarwareHitech

Growth Drivers & Positive Momentum:

1. Shift to High Margin Specialty Films: These now make up 87% of total revenue- a strategic move from commoditized films to higher value products.

2. US Tariff Relief & Export Recovery: US tariffs on imported films were reduced from 50% to 10% in Feb 2025 easing pressures and supporting exports (US is 50% of business).

3. D2C Network & OEM Wins: Expanding direct to consumer presence (300+ locations) and onboarding automotive OEMs.

4. MENA & Global Expansion:

New Dubai subsidiary (FZCO) targeting $20-22M sales as a growth market.

5. Capacity additions (e.g., TPU line with ₹118 Cr capex) and Chips to Film Integration.

Garware Hi-Tech Films: Specialty films (87% of revenue) fuel growth and margin expansion. Strong balance sheet, export recovery, OEM wins, and capacity additions support the outlook. ACCUMULATE. CMP ₹6,307 | TP ₹6,800. 📈 #Stocks #GarwareHiTech #Investing

#GarwareHiTech Films is becoming a materials science company not a film company. Most investors still put Garware in the same bucket as packaging film manufacturers.

But today around 87% of revenue comes from value added specialty products such as Sun Control Films (SCF), Paint Protection Films (PPF), and other high margin solutions. The business model has become far closer to a specialty materials company than a commodity film manufacturer.

This distinction matters because specialty material companies globally often command much higher valuation multiples than packaging companies.

The TPU backward integration story may be bigger than investors realize

Most investors know a TPU line is coming. What many don't appreciate is that TPU is the heart of PPF.

Currently TPU is one of the most critical and expensive inputs. Garware's 118 crore TPU project is expected to be commissioned around October 2026.

If execution is successful, benefits could include better gross margins, reduced dependence on external suppliers, faster product development, better quality control and stronger competitive moat

Several investor discussions have highlighted that management expects TPU integration to support future margin expansion.

The real moat is the application ecosystem. Investors usually focus on manufacturing capacity.

But Garware is quietly building:

- Global Application Studios

- Garware Home Solutions

- Large installer networks

- Direct-to-consumer channels

The company now has hundreds of application studios and is expanding internationally. A competitor can buy machinery but building a trained installer network across multiple countries is much harder.

Exports are the hidden engine. Many still see Garware as an Indian company. In reality, exports contribute roughly three fourths of sales and the company has presence in more than 90 countries. If management executes well in the US, Middle East and global architectural film markets, the addressable market becomes far larger than India's market alone.

PPF could become larger than what investors currently model. Today most discussions revolve around Sun Control Films. However, PPF is one of the fastest growing and highest value categories globally.

Garware is India's only professional grade PPF manufacturer, expanding capacity aggressively, onboarding automotive OEMs and investing heavily in TPU integration. If PPF continues compounding at a high rate, it could become the biggest earnings driver over the next several years.

Many investors still value Garware as a film manufacturing company. However a potentially more accurate description could be a global specialty materials company with dominant positions in Sun Control Films, Paint Protection Films, proprietary coating technologies, installer networks and upcoming TPU backward integration. If the market fully shifts from the first narrative to the second, the valuation framework itself could change substantially.

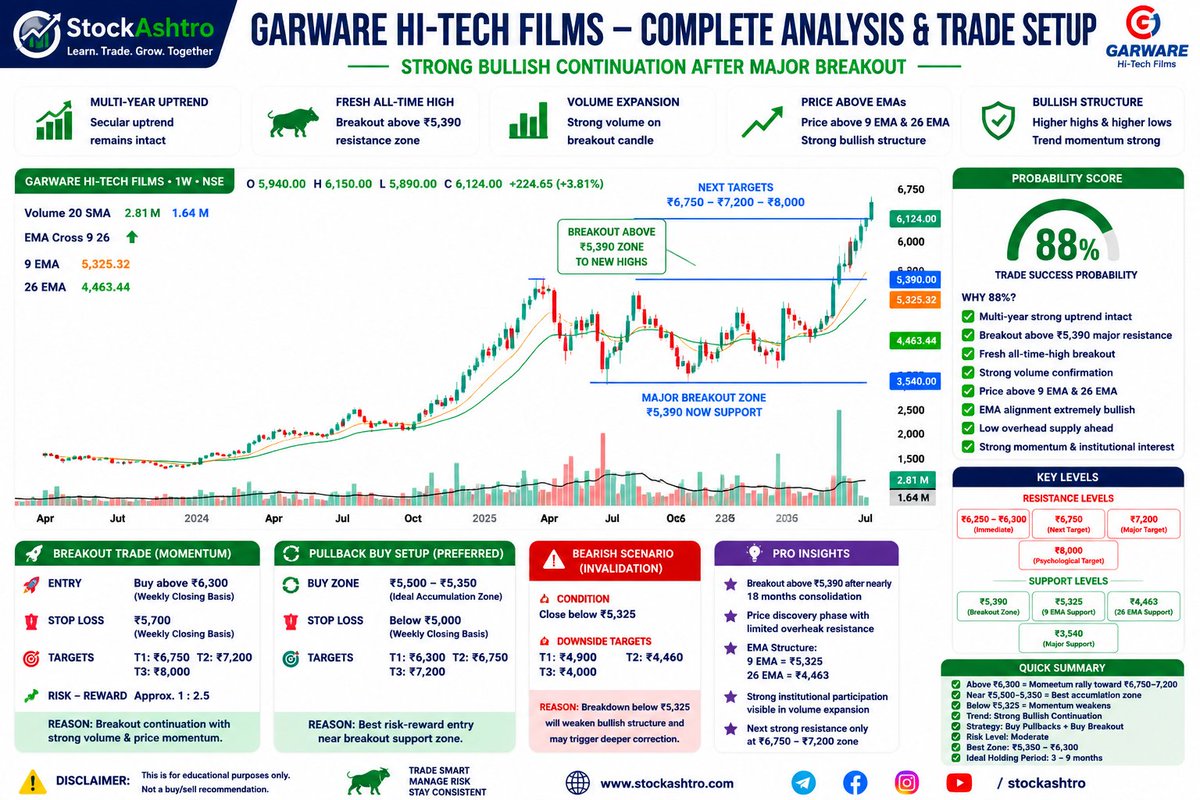

🚀 GARWARE HI-TECH FILMS hits a fresh All-Time High! 📈🔥

✅ Multi-year uptrend intact

✅ Breakout above ₹5,390 major resistances

✅ Momentum firmly with the bulls

Follow @StockAshtro for daily breakout stocks

#GarwareHiTech #BreakoutStocks #SwingTrading #StockMarketIndia

Garware Hi-Tech Films Q4FY26 concall looks incredibly strong

Zero Debt, 2,500 Cr revenue visibility 📈

• Launching high-margin TPU & PDLC films 🚀

• 4 new Indian Automotive OEMs onboarded for PPFCapacity utilization hitting 85% . #GarwareHiTech #StocksToWatch #StockMarketIndia

Garware Hi-Tech Films , understanding the value chain advantage and understanding the product economics , capability mapping and qualitative depth analysis and also attaching the first half of the call notes , second is also available on the feed folks

#Garwarehitech

#Garware

Stock is firing 🔥

An Indian co competing in the world with better quality and better pricing and still innovating on new products and winning market share.

Last two qtrs resilient nos reported by Garware Hi tech

Disc - Study the business. No reco.

#Garwarehitech

Again superb nos 🔥 reported by co and guidance for FY27 is good

Market rewards when co deliver resilient performance in difficult times like Tariff.

Stock touched new high 🔥

Disc - no reco to buy or sell.

#GarwareHiTech Films is often dismissed as "just another film company." A closer look at the business suggests something very different.

The company is India's only fully backward integrated specialty film manufacturer with leadership positions in Solar Control Films (SCF) and Paint Protection Films (PPF). Despite operating in a segment many consider commoditized, Garware delivered its highest ever EBITDA margin of 26.2% in Q4 FY26 and 23.6% for the full year.

What makes this performance more impressive is that FY26 was impacted by elevated US tariffs for most of the year. Even with this headwind, Garware reported record quarterly revenue of ₹597 crore and record profitability in Q4, indicating that demand and pricing power remain strong.

The balance sheet is another major strength. The company operates with virtually no debt, maintains over ₹770 crore of liquidity, and has funded more than ₹500 crore of recent expansion entirely through internal accruals. Its working capital cycle is exceptionally efficient, with collections averaging just seven days compared with industry norms of 60-90 days.

The biggest long term opportunity lies in Paint Protection Films. India currently has PPF penetration of only around 1.5%, compared with 13-15% in markets such as the US and China. With annual passenger vehicle sales expected to increase significantly over the coming years, even a modest increase in penetration could create a multi thousand crore market opportunity.

Garware was the first company to launch a professional grade PPF product in India, effectively creating the category.

The company is also steadily diversifying geographically. While the US remains an important market, its contribution has reduced as newer regions gain scale. The Middle East and North Africa region has already doubled its contribution over the last few years, and management has ambitious targets for further expansion.

A key strategic project is the upcoming TPU manufacturing facility. TPU represents the majority of the raw material cost in PPF and is currently imported. Once operational, Garware is expected to become the world's only fully backward integrated PPF manufacturer. This not only improves supply security but also has the potential to enhance margins while opening opportunities in medical grade and architectural applications.

Another underappreciated growth engine is architectural films. The segment is growing rapidly, supported by increasing focus on energy efficiency and green buildings. Garware enjoys certifications and approvals that position it well for institutional and infrastructure projects. Management has outlined ambitious plans to scale this business substantially over the coming years.

Looking ahead, the company has guided for revenue of at least ₹2,500 crore in FY27 while maintaining EBITDA margins around 25% ±2%. Multiple growth drivers including SCF expansion, PPF adoption, TPU backward integration, architectural films and international expansion are working simultaneously.

Garware today looks less like a commodity film manufacturer and more like a specialty materials company with strong margins, a fortress balance sheet, significant cash generation and multiple long duration growth opportunities.

#GarwareHiTech is the world’s #1 chip-to-film integrator.

Full vertical integration gives a significant cost advantage over peers who buy chips from the open market.

This integration insulates them somewhat from raw material volatility and ensures consistent quality feedstock for the next stage.

The PET chips are melted and extruded into thin films, then stretched in a bi axial orientation process (machine direction plus transverse direction) to create strong, thin, high performance BOPET film.

Differentiation:

Multiple proprietary production lines.

Advanced nano dispersion technology for superior optical and functional properties.

This base film becomes the foundation for all higher value specialty products.

Advantage: Proprietary process technology creates a moat which is harder for competitors to replicate quickly.

Key Products:

1. Sun Control Films (SCF)

Window films for buildings and vehicles (heat rejection, UV protection, privacy).

2. Paint Protection Film (PPF)

Protective layers for automotive paint.

Thermal lamination films, etc.

Capacity Expansion: From 4,200 LSF/year (likely Lakh Square Feet) currently to 5,400 by FY28.

Margin Profile: 22-40% significantly higher than the base film business because of the specialized coatings and intellectual property involved.

Role: This is where the real value creation happens turning a commodity like base film into high performance, branded specialty products.

Strong relationships with 4 large auto OEMs.

Exports to 90+ countries.

Dominant position in the US market (largest geography).

Serves institutional buyers and large distributors.

Advantage: Stable, high volume business with predictable demand.

D2C/Retail:

Garware Application Studios

Network:

250+ Garware Application Studios (GAS) in India.

11 international studios.

6 Home Solutions centres.

Positioning: Highest margin channel and the fastest growing part of the business.

Model: Company controlled application studios ensure proper installation (critical for performance films), build brand and capture retail margins directly.

The company has built a rare end to end integrated model (from chip to applied film) which is uncommon in the industry.

This allows them to capture margins at every layer instead of losing value to suppliers or distributors.

The strategy is shifting from a "film manufacturer" to a high margin specialty materials plus branded application business.

Risks remain around raw material volatility, but the integration and proprietary technology plus expanding D2C presence creates a strong competitive position.

#GarwareHiTech Q4FY26 concall actually pointing towards one of the most important long term developments. It signals a transition from being primarily a manufacturer selling through distributors to becoming a consumer facing branded solutions company.

Traditionally Garware's business model was largely B2B. The company manufactured films and sold them through distributors, dealers and installers. While this model scales well, a significant portion of the value chain economics remains with intermediaries. Now management is deliberately moving closer to the end customer.

The Garware Application Studio network is central to this strategy. With more than 250 studios already operational and a target of crossing 300 shortly, Garware is creating a nationwide branded installation ecosystem. Instead of customers simply asking for any film, they increasingly ask for Garware products specifically. This strengthens brand recall and pricing power.

The international rollout is equally important. Opening Global Application Studios in markets such as the UAE and the U.S. demonstrates that management wants to replicate the Indian model globally. If successful, this could gradually reduce dependence on private label sales and increase the proportion of branded revenue.

The most interesting development is Garware Home Solutions (GHS).

Historically, investors viewed Garware largely as an automotive film company. GHS expands the opportunity into residential and commercial buildings. Every modern office, mall, hospital, hotel, airport, residential tower and glass façade becomes a potential customer.

This is where management's statement that "everywhere there is glass, a film can be put on that glass" becomes significant.

The addressable market expands from vehicle owners to:

- Homeowners

- Builders and developers

- Architects

- Interior designers

- Commercial real estate owners

- Hotels

- Corporate offices

- Healthcare facilities

- Educational institutions

This creates a much larger and more diversified growth opportunity.

The margin implications could be even more important than the revenue implications.

Management repeatedly stated that D2C margins are approximately 25-40% higher than traditional distributor led margins.

This means that if a product generating ₹100 through distribution generates ₹10 of profit, the same product sold through a D2C channel could potentially generate substantially more profit because Garware captures a larger portion of the value chain. As D2C penetration rises, profit growth can outpace revenue growth.

Another noteworthy aspect is that D2C penetration is still very low globally. Current D2C contribution is only about 10-15% of PPF revenue worldwide. This means the journey is still at an early stage. India has already reached around 40% penetration in some areas, demonstrating that the model works. The global opportunity remains largely untapped. The digital metrics also indicate that management is investing in brand creation rather than merely manufacturing capacity.

Website traffic has increased from only a few thousand monthly visitors to nearly 1.8 lakh monthly visitors. Annual website visits of approximately 18 lakh and more than 8 crore impressions across Meta platforms suggest that Garware is actively building consumer awareness, which is uncommon for many industrial manufacturing companies.

The FY28 target of crossing approximately ₹200 crore from Garware Home Solutions and related new products is particularly important. On the surface, ₹200 crore may appear small relative to total revenue exceeding ₹2,100 crore. However, if these revenues carry materially higher margins and stronger brand ownership, they can have a disproportionate impact on profitability and valuation.

Markets often assign higher valuation multiples to companies that:

- Own consumer brands.

- Control customer relationships.

- Possess pricing power.

- Generate superior margins.

- Have scalable distribution networks.

.

#GarwareHiTech is the only Indian manufacturer of premium PPF and

one of very few globally integrated players in this segment.

Many products of Garware Hi-Tech Films Limited are specifically designed to help reduce heat, control solar radiation and improve temperature management.

Their window films and solar control films are widely used in cars, homes, offices and commercial buildings to reduce heat entering through glass surfaces.

These films help block infrared radiation, reduce glare and filter harmful UV rays.

In automobiles, the films can significantly reduce cabin heating under direct sunlight making interiors more comfortable while also improving air conditioning efficiency. This is one reason premium heat control films are seeing growing demand in India’s hot climate conditions.

In buildings and commercial spaces, these films help lower indoor temperatures and reduce cooling costs. They are increasingly used in energy efficient and green building applications where reducing heat load and electricity consumption is important.

Their Paint Protection Films (PPF) however serve a different purpose. PPF is mainly designed to protect vehicle paint from scratches, stone chips, and surface damage rather than heat reduction.

As temperatures rise and awareness about energy efficiency increases, demand for heat-control and solar protection films is expected to grow structurally, which can become a long term tailwind for Garware Hi-Tech Films.

#GarwareHiTech

Stock is doing Well

Not Holding as of now

Garware Hi-Tech Films brought detailing professionals together at the Detailing Studio Meet in Hyderabad to explore advanced protection solutions, industry insights, and stronger business connections.

Discover the future of automotive protection with Garware PPF.

#Garwarehitech

Last Seen Hashtags on Sotwe

aloha

Seen from Korea

silivritravesti

Seen from Turkey

touchdownkissfanmeet

Seen from United States

arcanine

Seen from United States

stripperfetish

Seen from Pakistan

petrification

Seen from Japan

ngintip

Seen from Indonesia

tiktokviral

Seen from Mexico

ديوت_بدويٌّْ

Seen from Saudi Arabia

MostViews

Seen from Egypt

Most Popular Users

Elon Musk

@elonmusk

240.3M followers

Barack Obama

@barackobama

119.3M followers

Donald J. Trump

@realdonaldtrump

111.6M followers

Cristiano Ronaldo

@cristiano

109.6M followers

Narendra Modi

@narendramodi

106.9M followers

Rihanna

@rihanna

97.4M followers

NASA

@nasa

92.1M followers

Justin Bieber

@justinbieber

90.7M followers

KATY PERRY

@katyperry

87.2M followers

Taylor Swift

@taylorswift13

81M followers

Lady Gaga

@ladygaga

72.6M followers

Kim Kardashian

@kimkardashian

69.6M followers

Virat Kohli

@imvkohli

69.1M followers

YouTube

@youtube

68.6M followers

Bill Gates

@billgates

63.6M followers

The Ellen Show

@theellenshow

62.5M followers

CNN

@cnn

61.9M followers

Neymar Jr

@neymarjr

61.8M followers

X

@x

60.9M followers

Selena Gomez

@selenagomez

60.3M followers